Getrawbox Getrawbox

Getrawbox Getrawbox

Related Articles

Table of Contents

- How to Refinance Student Loans Without a Degree: A Step‑by‑Step Guide

- Eligibility Criteria to Refinance Student Loans Without a Degree

- Top Lenders That Allow Non‑Degree Borrowers

- How to Apply: The Practical Steps

- Tips to Secure the Best Rate When You Refinance Student Loans Without a Degree

- Potential Pitfalls and How to Avoid Them

- Real‑World Example: How Jane Turned a 7 % Federal Loan into a 3.9 % Private Rate

- Alternative Strategies If You Can’t Secure a Traditional Refinance

- What to Expect After You Refinance Student Loans Without a Degree

Carrying a student loan can feel like a permanent weight, especially when you didn’t finish a degree program. The good news? You don’t have to stay stuck with the original terms just because your education path didn’t follow the traditional route. Refinancing student loans without a degree is not only possible, it’s becoming a mainstream option for many borrowers who want to lower their monthly payment, snag a better interest rate, or simply regain control over their finances.

In this article we’ll walk through the entire process, from figuring out whether you qualify to picking the right lender and locking in the best rate. We’ll also toss in some practical tips, common pitfalls to avoid, and a few real‑world examples so you can see how the strategy works in practice. By the time you finish reading, you’ll have a clear, actionable roadmap to refinance student loans without a degree and start saving money right away.

Whether you’re a former college student who left school early, a career‑changer who pursued certifications instead of a four‑year degree, or simply someone who took a break from formal education, the steps outlined below will help you navigate the refinancing landscape with confidence.

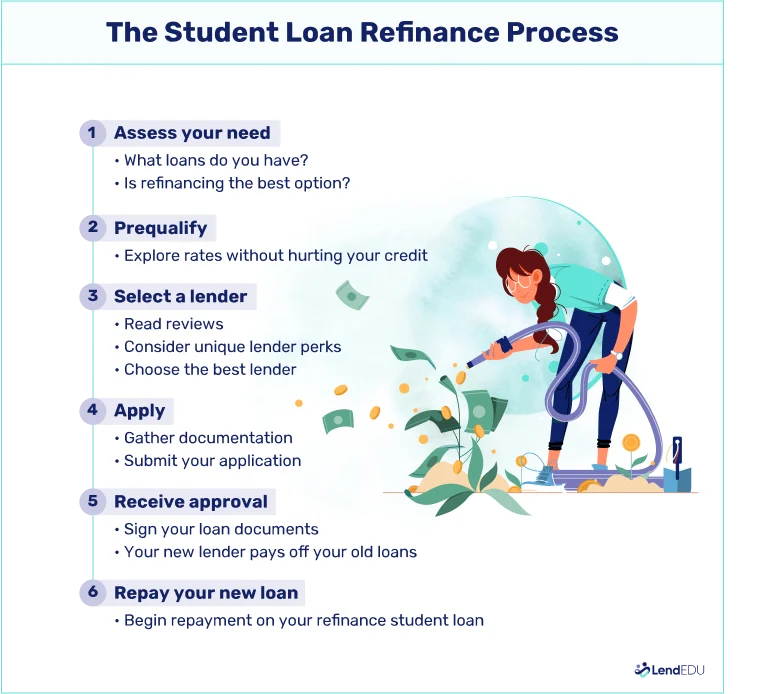

How to Refinance Student Loans Without a Degree: A Step‑by‑Step Guide

Refinancing is essentially swapping out your existing student loan(s) for a new loan that has a different interest rate, term, or repayment structure. The key difference for borrowers without a degree is that many traditional lenders still use degree completion as a proxy for creditworthiness. However, a growing number of private lenders are shifting their focus toward other metrics—like credit score, employment stability, and debt‑to‑income ratio—making it feasible to refinance student loans without a degree.

Eligibility Criteria to Refinance Student Loans Without a Degree

- Credit Score: Most lenders require a minimum FICO score of 660–700 for the most competitive rates. If you’re below that range, you might still qualify but at a higher interest rate.

- Income and Employment History: Steady employment for at least two years and a reliable income stream show lenders you can manage the new monthly payment.

- Debt‑to‑Income (DTI) Ratio: Aim for a DTI below 36 %. This ratio is calculated by dividing your total monthly debt payments by your gross monthly income.

- Loan Type and Balance: Most lenders accept federal and private student loans, but some have minimum balance requirements (often $5,000–$10,000).

- Co‑Signer Option: If your credit profile is thin, adding a credit‑worthy co‑signer can open doors to better rates.

Even without a degree, strong performance in these areas can make you an attractive candidate. Lenders are increasingly using automated underwriting tools that weigh these factors more heavily than educational credentials.

Top Lenders That Allow Non‑Degree Borrowers

Below is a quick snapshot of lenders known for being more flexible about degree status. Remember to compare APR, fees, and repayment options before committing.

- Earnest: Offers rates as low as 2.49 % for borrowers with a 720+ credit score, regardless of degree completion.

- SoFi: Known for “no‑fee” refinancing and a streamlined online application; they focus on income and credit health.

- CommonBond: Provides a “Social Impact Loan” with a portion of the proceeds going to education charities, and they do not require a degree.

- LendKey: Partners with community banks and credit unions, often offering competitive rates for borrowers with solid employment histories.

- Credible (Marketplace): Aggregates offers from multiple lenders, making it easy to see which institutions are willing to refinance without a degree.

How to Apply: The Practical Steps

- Gather Your Current Loan Details: Note the total balance, interest rate, and remaining term for each loan you want to refinance.

- Check Your Credit Report: Ensure there are no errors that could drag down your score. For a deeper dive, read our guide on impact of student loans on your credit report.

- Calculate Your DTI Ratio: Use a simple spreadsheet or an online calculator to see where you stand.

- Shop Around: Use a marketplace like Credible or go directly to lenders that explicitly state they accept borrowers without a degree.

- Submit an Application: Most applications are completed online and take under 15 minutes. You’ll need proof of income (pay stubs or tax returns) and identification.

- Review the Offer: Pay attention to APR, any origination fees, and whether the loan is fixed or variable.

- Close the Deal: Sign the loan agreement, and the new lender will pay off your existing loans directly.

Tips to Secure the Best Rate When You Refinance Student Loans Without a Degree

- Boost Your Credit Score First: Pay down revolving credit, keep credit utilization below 30 %, and avoid opening new accounts a few months before applying.

- Consider a Shorter Term: While this raises your monthly payment, it can shave years off your loan and save thousands in interest.

- Lock in a Fixed Rate: Variable rates can be tempting when they’re low, but a fixed rate protects you from future hikes.

- Leverage a Co‑Signer: A credit‑worthy co‑signer can dramatically improve the rate you’re offered.

- Bundle with Other Debt Consolidation: If you have high‑interest credit‑card debt, some lenders let you combine it with student loans for a single, lower‑rate payment.

- Watch for Hidden Fees: Origination fees, pre‑payment penalties, and late‑payment fees can erode your savings.

One often‑overlooked strategy is to use a 401(k) loan to pay off high‑interest student debt, then refinance the remaining balance with a private lender. This can be especially useful if your 401(k) loan interest rate is lower than what you’d receive on a traditional refinance.

Potential Pitfalls and How to Avoid Them

Refinancing can be a financial win, but it’s not without risks. Here are the most common pitfalls and practical ways to sidestep them:

- Loss of Federal Benefits: When you refinance federal loans into a private loan, you lose access to income‑driven repayment plans, deferment, forbearance, and loan forgiveness programs. Make sure the interest‑rate savings outweigh the loss of these protections.

- Higher Total Interest Cost: Extending the loan term can lower your monthly payment but may increase the total interest you pay over the life of the loan.

- Rate Lock Expiration: Some lenders offer a rate lock for a limited window (usually 30–60 days). If you miss the deadline, you could end up with a higher rate.

- Hidden Fees: Origination or processing fees can add up. Always ask for a “no‑fee” refinance option if possible.

- Credit Score Dip: Applying to multiple lenders can generate several hard inquiries, briefly lowering your credit score. Use rate‑shopping tools that count as a single inquiry within a 45‑day window.

Real‑World Example: How Jane Turned a 7 % Federal Loan into a 3.9 % Private Rate

Jane left college after two years and took out $25,000 in federal student loans at a 7 % interest rate. After three years of full‑time employment, she had a credit score of 730 and a DTI of 28 %.

She used a credit‑union marketplace to compare offers and found a private lender willing to refinance her loans at 3.9 % fixed for a 10‑year term. The monthly payment dropped from $260 to $250, but more importantly, she saved roughly $4,500 in interest over the life of the loan.

Jane’s story underscores how solid credit and steady income can outweigh the lack of a completed degree when it comes to refinancing.

Alternative Strategies If You Can’t Secure a Traditional Refinance

- Income‑Driven Repayment (IDR) for Federal Loans: While not a refinance, IDR plans can lower payments based on income and family size.

- Public Service Loan Forgiveness (PSLF): If you work for a qualifying employer, making 120 qualifying payments can wipe out the remaining balance.

- Peer‑to‑Peer Lending Platforms: Some platforms match borrowers with individual investors who may be more flexible about degree status.

- Debt Snowball or Avalanche Method: Focus on paying off the highest‑interest loans first while maintaining minimum payments on the rest.

If you decide to use a credit card to cover part of your student loan, make sure you understand the risks. Our article on paying student loans with a credit card walks through the pros and cons of that approach.

What to Expect After You Refinance Student Loans Without a Degree

Once your refinance is complete, you’ll notice a few immediate changes:

- New Monthly Statement: Your lender will send you a new payment schedule and online portal access.

- Impact on Credit Score: Initially, the hard inquiry may dip your score a few points, but as you make on‑time payments, the score typically improves.

- Potential Savings: Lower interest rates translate to reduced total interest paid, freeing up cash for other financial goals like emergency savings or retirement.

It’s also wise to set up automatic payments. Many lenders offer a rate reduction of 0.25 % for borrowers who enroll in autopay, which can add up to extra savings over the loan’s life.

Finally, keep an eye on your credit report for at least a year to confirm that the old loan accounts are reported as “closed” and the new loan reflects correctly. Any discrepancies should be disputed with the credit bureaus.

Refinancing student loans without a degree is a powerful tool, but it works best when paired with a broader financial plan. Consider how the new payment fits into your budget, retirement contributions, and other debt obligations. With the right strategy, you can turn a seemingly stagnant debt into a stepping stone toward financial freedom.

Ready to start? Begin by checking your credit score, gathering your loan details, and exploring the lenders listed above. The journey may require a bit of research, but the payoff—lower payments, less interest, and greater financial flexibility—is well worth the effort.