Getrawbox Getrawbox

Getrawbox Getrawbox

Related Articles

Table of Contents

- is student loan interest monthly or yearly: The Core Difference

- How is student loan interest calculated if is student loan interest monthly or yearly?

- Why the Timing of Interest Matters for Borrowers

- Tips if is student loan interest monthly or yearly confuses you

- Federal vs. Private Loans: Different Rules for Interest Accrual

- Impact on Repayment Strategies

- How to Reduce Interest if is student loan interest monthly or yearly feels overwhelming

- Common Misconceptions About Interest Frequency

- Tools and Resources to Track Your Interest Accrual

When you take out a student loan, one of the first questions that pops up is is student loan interest monthly or yearly. The answer isn’t always straightforward, because it depends on the type of loan, the lender’s policies, and even the specific terms you sign up for. Understanding the timing of interest accrual can help you budget better, avoid surprise balances, and even save money in the long run.

In this article we’ll break down the mechanics behind loan interest, compare the monthly versus yearly approaches, and give you practical tips on how to keep your payments under control. Whether you’re a fresh graduate just starting to repay or someone who’s been navigating student debt for years, having a clear picture of how interest works is essential for smart financial planning.

We’ll also sprinkle in some handy resources—like where to check your loan balance and how to refinance—so you’ll leave with a toolbox of strategies rather than just theory. Let’s dive in and answer that lingering question: is student loan interest monthly or yearly?

is student loan interest monthly or yearly: The Core Difference

The short answer is that most federal student loans in the United States calculate interest on a daily basis, which is effectively monthly when it gets added to your balance. Private lenders, on the other hand, often use a yearly interest rate that is compounded either monthly or quarterly. This distinction matters because it determines how quickly your balance can grow, especially if you’re only making the minimum payment.

How is student loan interest calculated if is student loan interest monthly or yearly?

Interest calculation follows a simple formula: Outstanding principal × Interest rate ÷ Number of periods. For monthly accrual, the annual percentage rate (APR) is divided by 12. For daily accrual, it’s divided by 365, and the resulting daily interest is added to the loan each day. At the end of each month, the accumulated daily interest is posted to your balance, which is why many borrowers think of it as “monthly interest.”

Private loans that state a yearly rate usually apply that rate to the balance once per year, but they may still add the interest to the principal on a monthly schedule. The key is to read the loan agreement: if it says “interest compounds monthly,” you’ll see your balance rise each month even if you’re not making payments.

Why the Timing of Interest Matters for Borrowers

Knowing whether is student loan interest monthly or yearly can influence several aspects of your financial life:

- Payment Planning: Monthly accrual means interest builds up faster if you miss a payment, while yearly accrual gives a bit more breathing room.

- Interest Savings: Paying early can reduce the amount of interest that compounds, especially under a daily or monthly model.

- Refinancing Decisions: Understanding the original interest schedule helps you compare offers from new lenders.

For example, if you have a $30,000 loan at a 5% APR and you pay only the minimum each month, the daily accrual method will add about $4.11 in interest each day. Over a year, that’s roughly $1,500 in interest—more than the simple yearly calculation would suggest if you didn’t make any payments.

Tips if is student loan interest monthly or yearly confuses you

- Check Your Loan Statement: Look for terms like “interest accrues daily” or “interest compounds monthly.” This will clarify the schedule.

- Use Online Calculators: Many financial sites let you plug in loan amount, rate, and accrual frequency to see projected balances.

- Set Up Automatic Payments: Most lenders waive a small portion of the interest (often 0.25%) if you enroll in autopay, effectively lowering the effective rate.

- Consider Refinancing: If your private loan uses a yearly compounding method that feels too harsh, refinancing to a loan with daily accrual could save you money.

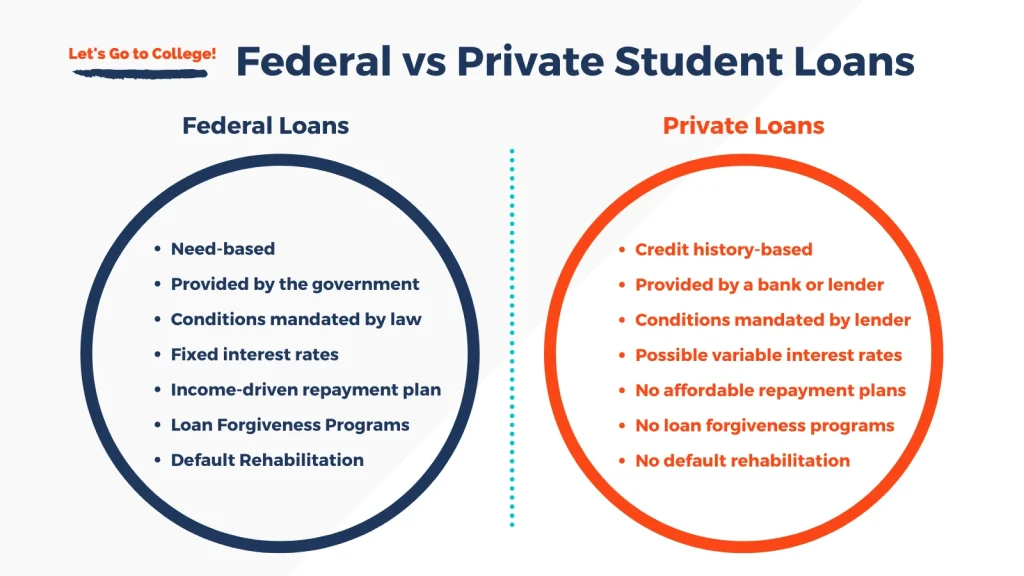

Federal vs. Private Loans: Different Rules for Interest Accrual

Federal student loans, including Direct Subsidized, Direct Unsubsidized, and PLUS loans, typically accrue interest daily. While you’re in school at least half‑time, interest on subsidized loans is covered by the government, but unsubsidized loans keep accruing daily interest that’s added to the balance once you graduate or drop below half‑time status.

Private student loans, issued by banks or credit unions, can vary widely. Some may advertise a “fixed yearly rate,” yet apply it monthly. Others might offer a “variable yearly rate” that changes annually based on the prime rate. This variability makes it crucial to read the fine print and ask the lender directly how interest is applied.

If you’re still unsure about the specifics of your own loans, the article where can i see my student loans? A Complete Guide walks you through how to locate your loan documents and decipher the interest terms.

Impact on Repayment Strategies

Knowing whether interest is monthly or yearly shapes how you approach repayment:

- Pay More Than Minimum: With daily accrual, every extra dollar you pay reduces the principal on which future interest is calculated, leading to exponential savings.

- Target High‑Interest Loans First: If you have a mix of federal and private loans, prioritize the ones that accrue interest more frequently (usually private loans with monthly compounding).

- Utilize Income‑Driven Repayment (IDR) Plans: Federal loans offer IDR options that cap your monthly payment, but interest may still accrue daily, potentially increasing your balance over time.

One practical approach is the “snowball” method: start by paying off the loan with the highest interest frequency—often the one where is student loan interest monthly or yearly leans toward monthly accrual—while maintaining minimum payments on the rest.

How to Reduce Interest if is student loan interest monthly or yearly feels overwhelming

Here are three actionable steps:

- Make Bi‑weekly Payments: Splitting your monthly payment into two halves means you make an extra half‑payment each year, reducing principal faster.

- Apply Windfalls Directly to Principal: Tax refunds, bonuses, or side‑gig earnings can be tossed onto the loan balance, shaving off future interest.

- Refinance to a Lower Rate: If you have a private loan where interest compounds monthly, refinancing to a lower APR can dramatically cut the amount of interest you pay over the life of the loan. See the guide Refinance Student Loans Without a Degree – Your Complete Guide for more details.

Common Misconceptions About Interest Frequency

Many borrowers mistakenly believe that a “5% yearly interest” means they’ll only pay $1,500 in interest over ten years. In reality, because of compounding—whether monthly, daily, or yearly—the actual amount can be higher. The more frequently interest compounds, the more you pay over time.

Another myth is that paying off a loan early doesn’t matter if the interest is yearly. Even with yearly compounding, each payment reduces the principal before the next compounding period, thus lowering the interest charged for the upcoming year.

Tools and Resources to Track Your Interest Accrual

Keeping tabs on whether is student loan interest monthly or yearly can feel like a full‑time job, but a few digital tools can simplify the process:

- Loan Servicer Portals: Most federal and private lenders provide online dashboards where you can see accrued interest in real time.

- Budgeting Apps: Apps like Mint or YNAB let you set up custom categories for student loan interest, giving you a visual of how much accrues each month.

- Spreadsheet Trackers: A simple Excel sheet with columns for principal, interest rate, accrual frequency, and payment date can be a powerful way to model different scenarios.

If you’re looking for a step‑by‑step walkthrough on checking your loan details, the guide Business Loans for New Small Businesses – A Complete Guide also touches on reviewing loan statements, which is a skill that translates well to student loans.

Ultimately, the key to mastering your debt lies in understanding the mechanics behind interest. Whether your loan accrues interest monthly, daily, or yearly, the principles remain the same: the sooner you reduce the principal, the less interest you’ll pay overall.

So, next time you sit down to budget, ask yourself: is student loan interest monthly or yearly for each of my loans? Then apply the strategies above to keep that interest from sneaking up on you. With a clear grasp of how interest works and a proactive repayment plan, you’ll be well on your way to financial freedom.