Getrawbox Getrawbox

Getrawbox Getrawbox

Related Articles

Table of Contents

- Is Rocket Mortgage Good for Home Loans? A Straight‑Up Look

- Pros When You Ask: Is Rocket Mortgage Good for Home Loans?

- Cons to Keep in Mind: Is Rocket Mortgage Good for Home Loans?

- Eligibility and Application Process: Is Rocket Mortgage Good for Home Loans?

- Interest Rates and Fees: Is Rocket Mortgage Good for Home Loans?

- Customer Experience and Technology: Is Rocket Mortgage Good for Home Loans?

- Comparing Rocket Mortgage to Traditional Lenders

- Tips for Getting the Most Out of Rocket Mortgage

When it comes to financing a house, the name Rocket Mortgage pops up more often than a handful of traditional banks. Its sleek app, rapid approvals, and heavy marketing spend make many first‑time buyers wonder: is rocket mortgage good for home loans or is it just hype?

In this article we’ll peel back the layers of the brand, compare its offering with the old‑school lenders, and give you a realistic sense of what to expect. Whether you’re a tech‑savvy millennial hunting for a starter home or a seasoned homeowner looking to refinance, the insights below will help you decide if this digital‑first lender fits your needs.

We’ll also sprinkle in practical tips—like how to line up a pre‑approval for a VA loan or refinance other debts—so you can see the bigger picture of your borrowing strategy.

Is Rocket Mortgage Good for Home Loans? A Straight‑Up Look

Answering the question “is rocket mortgage good for home loans” isn’t a simple yes or no. The platform excels in some areas and falls short in others. Below we break down the major factors that matter most to borrowers.

Pros When You Ask: Is Rocket Mortgage Good for Home Loans?

- Speedy Application: The entire mortgage process can be started from a smartphone and often moves from application to approval in a matter of days.

- Transparent Pricing: Rocket Mortgage displays rate options up front, allowing you to compare APRs without hidden fees.

- Digital Convenience: All documents are uploaded electronically, and you can track progress in real time via the dashboard.

- Wide Product Suite: Conventional, FHA, VA, and jumbo loans are available, giving you flexibility regardless of your credit profile.

Cons to Keep in Mind: Is Rocket Mortgage Good for Home Loans?

- Higher Interest Margins: Compared with a local credit union, Rocket Mortgage’s rates can be a fraction of a percent higher, especially for borrowers with stellar credit.

- Limited Human Interaction: If you prefer face‑to‑face meetings, the digital‑first model may feel impersonal.

- Origination Fees: While the platform advertises “no hidden fees,” the standard 1%‑to‑2% origination charge can add up on larger loan amounts.

- Strict Automated Underwriting: Certain edge‑case financial situations (like self‑employment income spikes) may get flagged for manual review, slowing the process.

Eligibility and Application Process: Is Rocket Mortgage Good for Home Loans?

Getting started with Rocket Mortgage is as simple as downloading the app, creating an account, and entering basic personal information. The platform then runs a soft credit pull to give you an instant pre‑approval estimate.

If you’re curious about how this compares to a more traditional route, check out our guide on getting preapproved for a VA home loan. Both processes aim for speed, but the VA-specific guide highlights the extra documentation that government‑backed loans require—a nuance that Rocket Mortgage handles automatically if you select the VA option.

Key eligibility factors include:

- Credit score of 620 or higher (though better rates start at 680+).

- Debt‑to‑income ratio (DTI) generally below 45%.

- Proof of steady income—pay stubs, tax returns, or 1099s for freelancers.

- Down payment ranging from 3% (for conventional) to 0% (for VA or USDA).

Once you’ve uploaded the required documents, a loan officer will review the file. Most borrowers receive a final decision within 48‑72 hours, assuming no red flags.

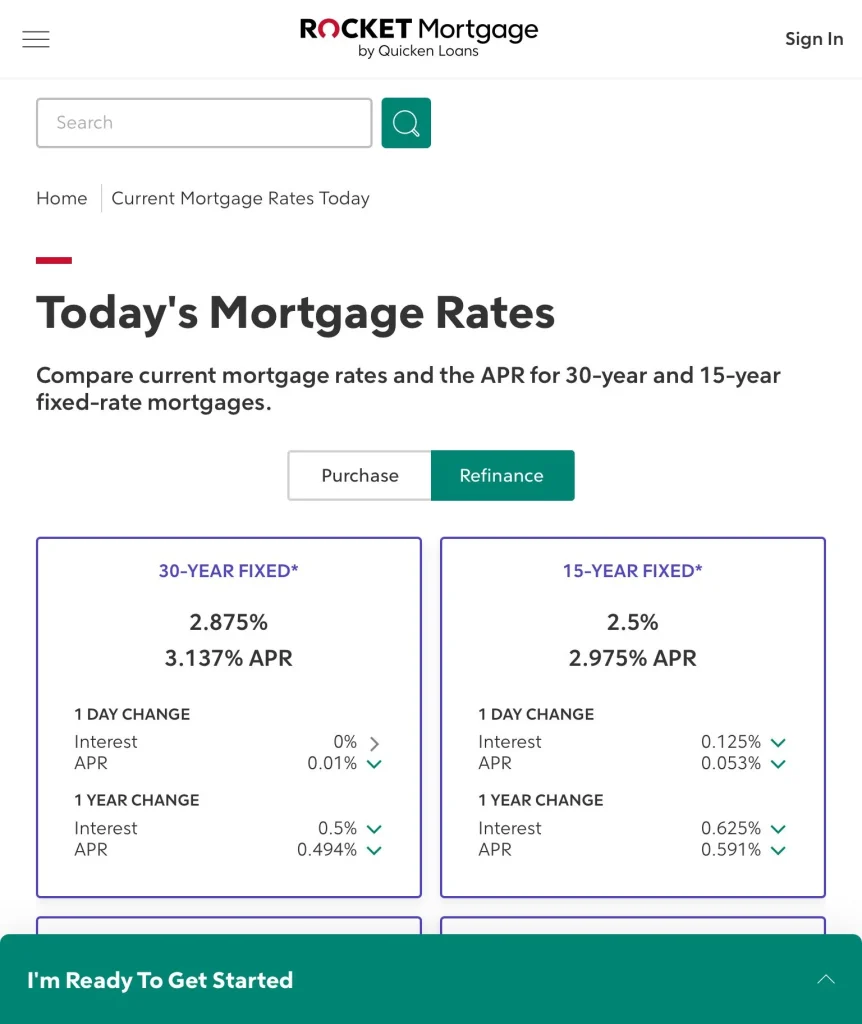

Interest Rates and Fees: Is Rocket Mortgage Good for Home Loans?

Interest rates are the heart of the “is rocket mortgage good for home loans” debate. Rocket Mortgage offers competitive rates that often sit within 0.10%‑0.25% of the national average. However, the platform’s convenience comes with a price tag—its origination fee typically ranges from 0.5% to 1.5% of the loan amount, and there may be an appraisal fee, credit report fee, and a small processing charge.

To put this in perspective, let’s say you’re borrowing $300,000 at a 4.125% rate with a 1% origination fee. That fee alone adds $3,000 to your closing costs. If you were to secure the same loan through a credit union offering a 3.95% rate with a 0.5% fee, you could save both on interest over the life of the loan and on upfront costs.

One way to offset higher rates is to refinance later. If you find a better deal, you can explore options like refinancing private student loans as an analogy—just as borrowers look for lower rates on education debt, they can do the same with mortgages.

Customer Experience and Technology: Is Rocket Mortgage Good for Home Loans?

The user interface is where Rocket Mortgage truly shines. The dashboard offers a clear timeline, real‑time updates, and an “Ask an Expert” chat that connects you with a licensed loan officer. For tech‑oriented borrowers, this level of transparency feels empowering.

That said, the reliance on algorithms can be a double‑edged sword. Some users report that the system occasionally misclassifies a legitimate document, prompting a manual review that stalls the process. When this happens, you’ll need to call the support line, which can be frustrating if you were expecting an entirely self‑service experience.

Overall, if you value speed and digital convenience, the answer to “is rocket mortgage good for home loans” leans toward yes. If you need a highly personalized touch—say, negotiating special terms for a unique property—traditional lenders might still have the edge.

Comparing Rocket Mortgage to Traditional Lenders

Below is a quick side‑by‑side comparison that helps answer the core question of whether Rocket Mortgage is a good choice for home loans:

| Feature | Rocket Mortgage | Traditional Bank / Credit Union |

|---|---|---|

| Application Speed | 24‑72 hrs (digital) | 1‑4 weeks (in‑person) |

| Rate Competitiveness | 0.10‑0.25 % above avg. | Often at or below avg. |

| Origination Fees | 0.5‑1.5 % | 0.25‑1 % |

| Customer Interaction | App & chat‑based | Branch & personal officer |

| Loan Types | Conventional, FHA, VA, Jumbo | Similar, plus some niche products |

From the table, the biggest trade‑off is speed versus marginally lower cost. If you’re buying in a hot market where a quick close can win a bidding war, the speed advantage may outweigh the extra fee—making Rocket Mortgage a good fit for home loans in that scenario.

Tips for Getting the Most Out of Rocket Mortgage

- Shop Rates Early: Use Rocket’s rate‑lock tool within the first 48 hours of pre‑approval to lock in a favorable rate.

- Boost Your Credit Score: Even a 20‑point increase can shave 0.10% off the APR, translating to thousands in savings over 30 years.

- Bundle Services: Some lenders offer discounts if you also open a checking account—check if Rocket has any current promotions.

- Plan for Refinancing: If you anticipate moving or your credit improving, consider a future refinance to lower your rate.

Remember, the decision “is rocket mortgage good for home loans” also hinges on your personal financial goals. A fast, digital experience might be worth a slightly higher rate if you need to close quickly. Conversely, if you have the luxury of time, a lower‑cost lender could save you more in the long run.

In any case, treat Rocket Mortgage as one tool among many. Run the numbers, compare the APR, factor in closing costs, and think about the level of human interaction you prefer. By doing a side‑by‑side comparison and keeping an eye on your credit health, you’ll be well‑positioned to make an informed decision.

Whether you ultimately choose Rocket Mortgage or a traditional bank, the most important thing is to secure a loan that aligns with your budget and future plans. Happy house hunting, and may your mortgage journey be smooth and financially sound!