Getrawbox Getrawbox

Getrawbox Getrawbox

Related Articles

Table of Contents

- what does refinancing a student loan mean: the basics explained

- how does refinancing a student loan work?

- Why people choose to refinance: key benefits

- Lower interest rates

- Reduced monthly payment

- Consolidating multiple loans

- Customizable repayment terms

- Potential downsides: what you might lose

- Loss of federal benefits

- Credit score requirements

- Variable interest rates

- Eligibility checklist: Are you a good candidate?

- Credit health

- Stable income

- Loan balance

- Identify your loan servicer

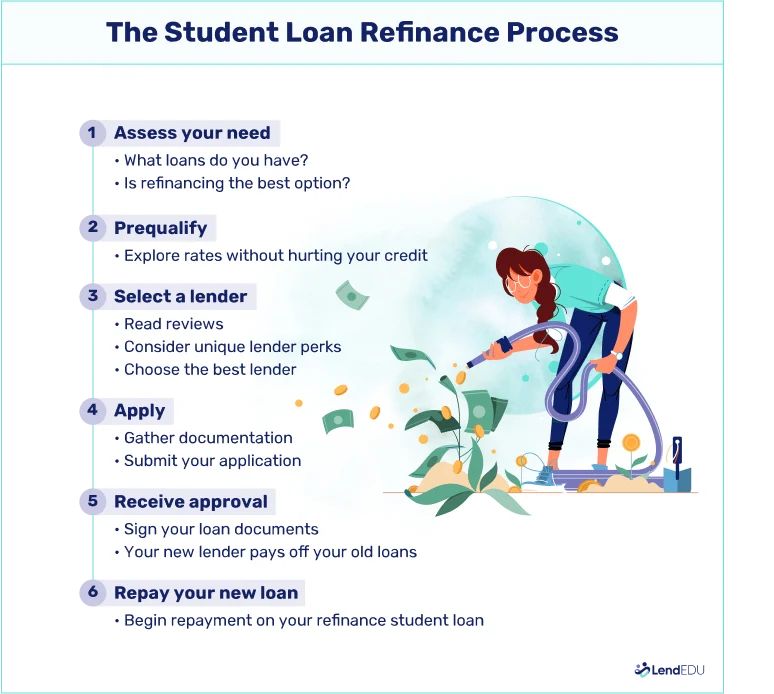

- Step‑by‑step guide to refinancing your student loans

- 1. Gather all loan details

- 2. Check your credit score

- 3. Shop around

- 4. Get pre‑qualified offers

- 5. Submit a full application

- 6. Review the final offer

- 7. Close the old loans

- 8. Set up automatic payments

- Refinancing vs. consolidation: which is right for you?

- Refinancing

- Consolidation

- When refinancing makes the most sense

- Common myths about refinancing student loans

- Myth 1: Refinancing will erase my debt instantly

- Myif 2: Only recent graduates can refinance

- Myth 3: All private lenders are the same

- Tips for maximizing your refinance outcome

- Final thoughts on what does refinancing a student loan mean

Student loans can feel like a permanent weight on your shoulders, especially when the interest keeps ticking up and the monthly payment doesn’t budge. You might have heard friends talk about “refinancing” their debt and wonder if that’s a magic fix or just another buzzword. In reality, understanding what does refinancing a student loan mean is the first step toward taking control of your financial future.

Whether you’re fresh out of college, a few years into your career, or even nearing retirement, the decision to refinance can reshape your cash flow, shorten the loan term, or simply give you peace of mind. But it’s not a one‑size‑fits‑all solution. The process involves swapping out your existing loan(s) for a new one—often with a different interest rate, repayment schedule, or lender.

In this article we’ll break down the concept, explore the pros and cons, walk you through the eligibility checklist, and hand you a practical roadmap so you can decide if refinancing aligns with your goals. Let’s dive in.

what does refinancing a student loan mean: the basics explained

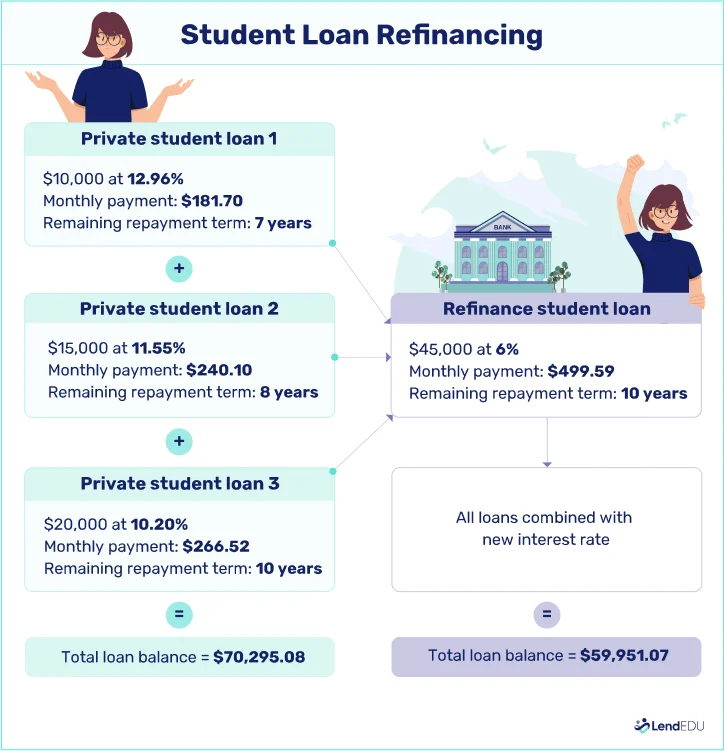

At its core, what does refinancing a student loan mean is simple: you replace one or more existing student loans with a new loan from a private lender. The new loan typically offers a lower interest rate, a different repayment term, or both. By doing so, you effectively “reset” your debt under new conditions that (hopefully) better suit your financial situation.

Unlike federal loan consolidation, which keeps the loan federal and preserves benefits like income‑driven repayment plans, refinancing usually involves moving your debt into the private sector. That shift can unlock lower rates, but it also means you may lose certain borrower protections.

how does refinancing a student loan work?

- Shop for lenders: Compare rates, fees, and customer reviews from banks, credit unions, and online lenders.

- Submit an application: Provide personal information, credit score, income verification, and details about your current loans.

- Get approved and receive an offer: If approved, the lender will propose a new interest rate, term length, and monthly payment.

- Close the old loans: The new lender pays off your existing balances, and you begin paying the new loan according to the agreed schedule.

If you’re curious about the step‑by‑step mechanics, check out our guide How Do I Refinance My Student Loans? A Complete Step‑by‑Step Guide for a deeper dive.

Why people choose to refinance: key benefits

Understanding what does refinancing a student loan mean in practice helps you see why many borrowers opt for it. Below are the most common advantages.

Lower interest rates

One of the biggest draws is a reduced interest rate. Even a half‑percent drop can translate into thousands of dollars saved over the life of the loan. For borrowers with strong credit scores and stable incomes, private lenders often offer rates that undercut the average federal rates.

Reduced monthly payment

By extending the loan term, you can lower the amount you owe each month. This can be a lifesaver if you’re juggling other debts, starting a family, or facing an unexpected expense. Just remember that a longer term may increase total interest paid, so weigh the trade‑off carefully.

Consolidating multiple loans

If you have several federal and private loans with varying rates and due dates, refinancing can bundle them into a single payment. This simplifies budgeting and reduces the chance of missing a due date.

Customizable repayment terms

Refinancing lets you choose the term that best fits your financial goals—whether you want to pay off the debt fast (shorter term, higher monthly payment) or stretch it out for affordability (longer term, lower payment).

Potential downsides: what you might lose

While it’s tempting to focus only on the upside, knowing what does refinancing a student loan mean also means recognizing the risks.

Loss of federal benefits

When you refinance federal loans into a private loan, you forfeit access to:

- Income‑Driven Repayment (IDR) plans

- Public Service Loan Forgiveness (PSLF)

- Deferment and forbearance options specific to federal loans

- Potential loan discharge in cases of total and permanent disability

If you think you might qualify for these programs, weigh the value of those protections against any rate savings.

Credit score requirements

Private lenders typically require a good to excellent credit score (often 680+). If your score is lower, you may not qualify for the best rates, or you might need a co‑signer, which adds complexity.

Variable interest rates

Some lenders offer variable‑rate loans that start low but can rise over time. While the initial payment may be attractive, future increases could erode the savings you hoped to achieve.

Eligibility checklist: Are you a good candidate?

Before you answer “yes” to what does refinancing a student loan mean for you, run through this quick self‑assessment.

Credit health

Check your credit report for errors and aim for a score of at least 680. If you’re below that, consider paying down existing debt or waiting until your credit improves.

Stable income

Lenders want to see reliable income to ensure you can meet the new payment. Typically, a debt‑to‑income (DTI) ratio under 40 % is preferred.

Loan balance

Most lenders have a minimum refinance amount (often $5,000–$10,000). If you have a small balance, consolidating may not be worth the effort.

Identify your loan servicer

Knowing who currently holds your loans is essential. It helps you gather accurate payoff amounts and understand any prepayment penalties. Our article who are my student loans through – Identify Your Loan Servicer Today walks you through the process.

Step‑by‑step guide to refinancing your student loans

Now that you grasp what does refinancing a student loan mean and have checked eligibility, follow this roadmap to get the best deal.

1. Gather all loan details

List each loan’s balance, interest rate, servicer, and monthly payment. This snapshot lets you compare the total cost of staying versus refinancing.

2. Check your credit score

Obtain a free credit report from AnnualCreditReport.com. If your score is solid, you’re in a good position to negotiate lower rates.

3. Shop around

Use comparison tools or visit lender websites directly. Look for:

- Interest rate (APR)

- Origination fees (some lenders charge 0‑1 % of the loan amount)

- Repayment term options

- Customer service ratings

4. Get pre‑qualified offers

Most lenders allow you to see a rate quote without a hard credit pull. This helps you gauge your options without impacting your score.

5. Submit a full application

When you choose a lender, complete the application with documentation: proof of income, identification, and your existing loan statements.

6. Review the final offer

Confirm the interest rate, term length, monthly payment, and any fees. Make sure the total cost over the life of the loan is lower than your current situation.

7. Close the old loans

The new lender will pay off your existing balances directly. Keep copies of the payoff statements for your records.

8. Set up automatic payments

Most lenders offer a discount (often 0.25 %–0.5 %) if you enroll in auto‑debit. This also helps you avoid missed payments.

If you need a more detailed walkthrough, our article How to Refinance a Private Student Loan: A Step‑by‑Step Guide provides screenshots and insider tips.

Refinancing vs. consolidation: which is right for you?

Both options aim to simplify repayment, but they serve different needs.

Refinancing

Best for borrowers with strong credit who want lower rates or customized terms. You trade federal benefits for potential savings.

Consolidation

Ideal for those who want to keep federal loan protections while merging multiple loans into one. It doesn’t lower the interest rate but can streamline payments and offer income‑driven plans.

If you’re wondering whether you can combine private loans, see our guide Can I Consolidate My Private Student Loans? A Complete Guide for the specifics.

When refinancing makes the most sense

Answering the question what does refinancing a student loan mean is only half the battle; you also need to know when it’s truly advantageous. Consider refinancing if:

- You have a credit score of 680+ and can qualify for a rate at least 0.5–1 % lower than your current average.

- You’re earning a stable income that comfortably covers the new monthly payment.

- You’re not relying on federal benefits like PSLF or IDR plans.

- You want to reduce the number of monthly due dates and simplify budgeting.

Common myths about refinancing student loans

Myth 1: Refinancing will erase my debt instantly

Refinancing replaces one debt with another; you still owe the same principal (plus any interest accrued). The benefit is a more favorable rate or term, not a magic eraser.

Myif 2: Only recent graduates can refinance

Anyone with a qualified credit profile can refinance, even borrowers with decades of repayment history. In fact, a longer credit track record can help you secure better rates.

Myth 3: All private lenders are the same

Interest rates, fees, and customer service vary widely. Some lenders specialize in student loan refinancing and offer tools like payment holidays or flexible repayment options.

Tips for maximizing your refinance outcome

- Lock in a fixed rate if you plan to keep the loan for many years; it protects you from future rate hikes.

- Pay attention to fees; a low rate with a high origination fee can nullify savings.

- Consider a co‑signer only if you trust the relationship, as they become equally responsible for repayment.

- Re‑evaluate annually; if your credit improves or market rates drop, you might refinance again for even better terms.

Final thoughts on what does refinancing a student loan mean

In essence, what does refinancing a student loan mean is swapping your existing loan(s) for a new one that ideally offers a lower interest rate, a more convenient repayment schedule, or both. It’s a strategic financial move that can free up cash flow, shorten the time you spend in debt, and reduce the overall cost of borrowing—provided you’re comfortable giving up federal protections.

The decision hinges on your credit health, income stability, and long‑term goals. Take the time to compare lenders, crunch the numbers, and consider whether you’ll need federal benefits down the road. With a clear understanding of the process and the right preparation, refinancing can be a powerful tool in your debt‑management toolkit.

Ready to explore your options? Start by checking your credit, gathering loan details, and visiting reputable lenders. Remember, the choice to refinance is personal, but armed with knowledge, you’ll be able to make a decision that aligns with your financial future.