Getrawbox Getrawbox

Getrawbox Getrawbox

Related Articles

Running a small business is a constant juggling act. One month you might be celebrating a surge in sales, the next you’re scrambling for cash to cover inventory, payroll, or an unexpected repair. Traditional term loans can feel like a blunt instrument—big, fixed payments that don’t flex with the rhythm of your business. That’s where a small business line of credit loans can make a real difference.

Think of a line of credit as a financial safety net that you can tap into whenever you need it, and only pay interest on the amount you actually use. It’s a revolving source of capital that grows and shrinks with your borrowing activity, offering the kind of flexibility many entrepreneurs crave. In this article we’ll break down everything you need to know about small business line of credit loans, from how they work to the nitty‑gritty of qualifying, and we’ll sprinkle in practical tips to keep your credit line healthy.

Whether you’re a seasoned owner looking to upgrade equipment, a startup needing runway, or a seasonal operator smoothing out cash‑flow peaks, understanding the mechanics of a line of credit can empower you to make smarter financial decisions without the stress of a one‑size‑fits‑all loan.

small business line of credit loans: What They Are and Why They Matter

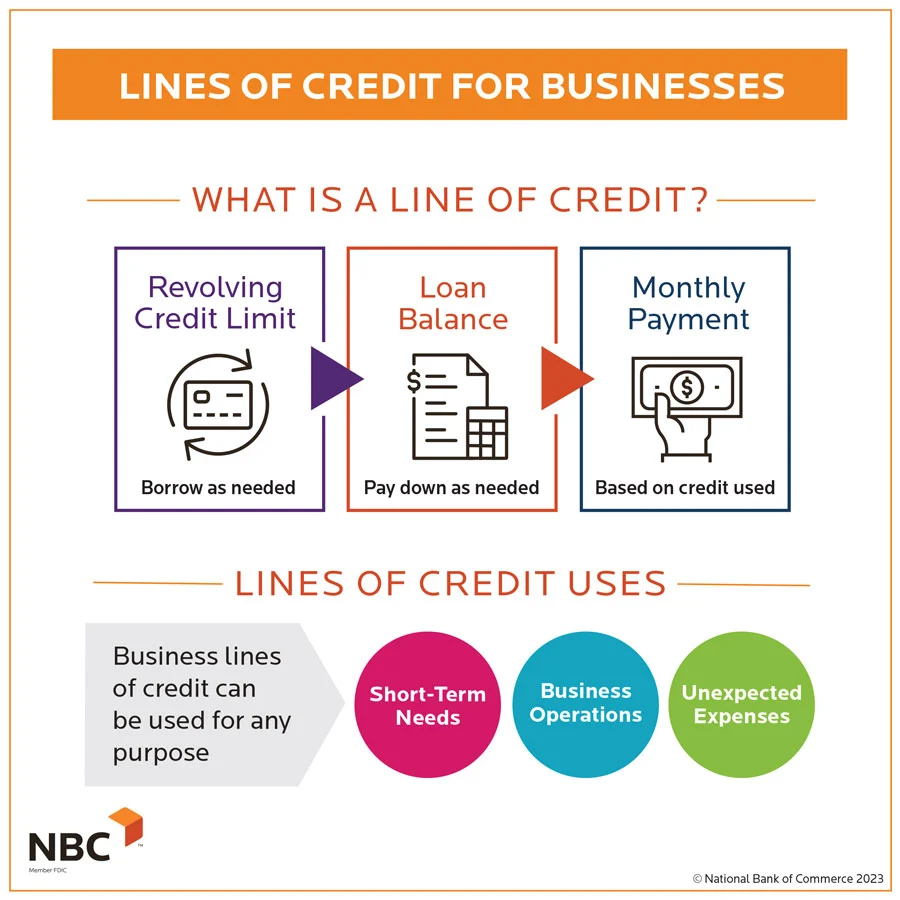

A small business line of credit loans is essentially a pre‑approved amount of money that a lender makes available to you on a revolving basis. Unlike a term loan, where you receive a lump sum and repay it in fixed installments, a line of credit lets you borrow, repay, and borrow again up to the approved limit. This revolving nature mimics a credit card, but typically with lower interest rates and higher borrowing limits tailored for business needs.

Why do they matter? Because cash flow is the lifeblood of any enterprise. A line of credit can cover short‑term gaps—like waiting for customer payments—without forcing you to take on high‑interest credit cards or scramble for emergency loans. It also provides a strategic tool for seizing growth opportunities, such as bulk inventory discounts or quick marketing pushes, while keeping your day‑to‑day operations smooth.

How small business line of credit loans Work

Understanding the workflow helps you decide if this financing option fits your business model:

- Application & Approval: You submit financial statements, tax returns, and often a personal credit check. Lenders evaluate revenue stability, credit score, and sometimes the industry.

- Credit Limit Set: Once approved, the lender assigns a maximum amount you can draw—commonly ranging from $10,000 to $500,000 for most small businesses.

- Draw Funds as Needed: You can access the money via online portals, checks, or a linked debit card. You only pay interest on the amount you actually use, not the full limit.

- Repayment Structure: Most lines require a minimum monthly payment, often a percentage of the outstanding balance plus interest. As you repay, your available credit replenishes.

- Renewal & Review: After a set term—usually 12 or 24 months—the lender may review your financials and either extend, adjust, or close the line.

Benefits of a Revolving Credit Facility

Here are the top reasons many entrepreneurs prefer a small business line of credit loans over traditional loans:

- Flexibility: Borrow only what you need, when you need it.

- Interest Savings: Pay interest solely on the drawn amount, not the entire credit limit.

- Speed: Once the line is set up, drawing funds can be instantaneous—perfect for urgent expenses.

- Improved Credit Profile: Responsible use and timely repayments can boost your business credit score.

- Strategic Growth: Enables you to act on opportunities without waiting for cash to accumulate.

Eligibility and Qualification Tips

Getting approved isn’t a mystery, but it does require a solid financial foundation. Below are practical steps to improve your odds:

- Maintain a Strong Credit Score: Most lenders look for a personal and business credit score of 650+.

- Show Consistent Revenue: Demonstrating steady cash flow—often at least $50,000–$100,000 in annual revenue—helps reassure lenders.

- Prepare Clear Financial Statements: Up‑to‑date profit & loss statements, balance sheets, and bank statements are essential.

- Limit Existing Debt: A lower debt‑to‑income ratio signals that you can manage additional credit responsibly.

- Leverage Collateral (if needed): Some lenders offer unsecured lines, but securing the line with assets can increase the limit and lower rates.

Choosing the Right Lender for Your Line of Credit

The market is crowded with banks, credit unions, and online lenders, each with its own terms and quirks. Here’s how to cut through the noise:

- Interest Rates & Fees: Look beyond the advertised APR. Watch for annual fees, draw fees, and early‑termination penalties.

- Credit Limit Flexibility: Some lenders allow you to request a limit increase after a few months of good performance.

- Repayment Terms: Compare minimum payment requirements and whether the lender offers interest‑only payments during the draw period.

- Access Methods: Online portals, mobile apps, and debit cards can make drawing funds more convenient.

- Customer Support: Responsive service is crucial when you need quick answers about your balance or draw limits.

For a deeper dive into revenue‑based financing alternatives, check out Small Business Loans Based on Revenue – A Complete Guide. It offers a complementary perspective on flexible funding that can work alongside a line of credit.

Managing Your Credit Line Wisely

Having a line of credit is only half the battle; managing it prudently ensures it remains a financial ally rather than a burden. Follow these best‑practice tips:

- Draw Only When Necessary: Treat the line as a buffer, not a cash‑cow. Over‑reliance can signal financial distress to lenders.

- Pay More Than the Minimum: Reducing the principal faster lowers overall interest costs and frees up credit faster.

- Monitor Utilization Ratio: Aim to keep usage below 30% of your limit to maintain a healthy credit profile.

- Set Up Automatic Payments: This helps you avoid missed payments that could trigger higher rates or a frozen line.

- Review Statements Regularly: Spot any unexpected fees or suspicious activity early.

When a Small Business Line of Credit May Not Be Ideal

Even a flexible financing tool has its limits. Consider alternative options if you encounter any of the following scenarios:

- Long‑Term Capital Needs: For sizable equipment purchases or expansion projects, a term loan with a fixed schedule might be cheaper.

- Very Low Credit Score: If your score falls below 600, you may face prohibitive rates or be denied outright.

- Irregular Revenue Streams: Businesses with wildly fluctuating cash flow might struggle with the minimum payment requirements.

If you’re exploring other financing avenues, you might also want to understand how a High Loan to Value Home Equity Loan could serve as a backup source, especially for owners who already possess real‑estate assets.

Real‑World Example: A Boutique Coffee Shop’s Success Story

Sarah owns a boutique coffee shop that experiences a seasonal dip in winter. By securing a $50,000 small business line of credit loans, she was able to:

- Purchase bulk coffee beans at a discounted rate during the high‑demand fall season.

- Cover payroll and utilities during the slower months without tapping high‑interest credit cards.

- Launch a limited‑time holiday menu that boosted sales by 15% once the line was repaid.

Within a year, Sarah’s careful draw‑and‑repay strategy not only kept the shop afloat during the off‑season but also improved her business credit score, qualifying her for a higher limit the following year.

Key Takeaways for Entrepreneurs

To recap, a small business line of credit loans offers:

- Flexible access to funds when cash flow gaps appear.

- Interest costs that align with actual usage.

- Opportunities to strengthen creditworthiness through disciplined repayment.

- A safety net that can be paired with other financing tools for a robust capital strategy.

Remember, the right line of credit is one that aligns with your revenue cycles, credit profile, and growth plans. Take the time to compare lenders, understand fee structures, and set clear internal policies for borrowing. When used strategically, a line of credit can be the quiet engine that powers your business forward, day after day.

Looking for more financing insights? Our guide on Does Sofi Refinance Private Student Loans – Complete Guide demonstrates how careful comparison shopping can save you money across different loan types—a habit that serves small business owners just as well.

In the end, the decision to tap into a small business line of credit loans should be guided by both immediate cash‑flow needs and long‑term strategic goals. Treat the line as a partnership with your lender: the more transparent and proactive you are, the more likely you’ll enjoy favorable terms, higher limits, and a financing relationship that grows alongside your business.

Good luck, and may your credit line be as adaptable as the entrepreneurial spirit that built your business.