Getrawbox Getrawbox

Getrawbox Getrawbox

Related Articles

Table of Contents

- does consolidating student loans affect credit score: The Core Mechanics

- does consolidating student loans affect credit score: Immediate Credit Inquiry

- does consolidating student loans affect credit score: Opening a New Account

- does consolidating student loans affect credit score: Closing Old Loans

- Long‑Term Credit Implications of Consolidation

- Common Myths About Consolidation and Credit Scores

- Myth 1: Consolidation Always Improves Your Score

- Myth 2: Closing Original Loans Erases Their Positive History

- Myth 3: You Can’t Consolidate Federal and Private Loans Together

- Strategic Tips to Minimize Negative Credit Impacts

- When Consolidation Might Not Be Worth It

- Real‑World Example: Emma’s Journey

- Bottom Line: Weighing the Credit Trade‑Offs

When you’re juggling multiple student loans, the idea of rolling them into one neat package can sound like a financial miracle. The promise of a single monthly payment, a potentially lower interest rate, and a simplified repayment schedule is tempting—especially when you’re already juggling tuition, rent, and a budding career. But before you click “apply,” it’s worth pausing to ask the question on everyone’s mind: does consolidating student loans affect credit score?

In this deep‑dive, we’ll unpack how loan consolidation interacts with the three pillars of your credit score—payment history, amounts owed, and credit history length—plus the less obvious psychological and financial shifts that come with consolidation. We’ll also sprinkle in practical tips, common pitfalls, and a few real‑world examples to help you make an informed decision. By the end, you should have a crystal‑clear picture of whether consolidating your student loans is a credit‑boosting move or a hidden risk.

does consolidating student loans affect credit score: The Core Mechanics

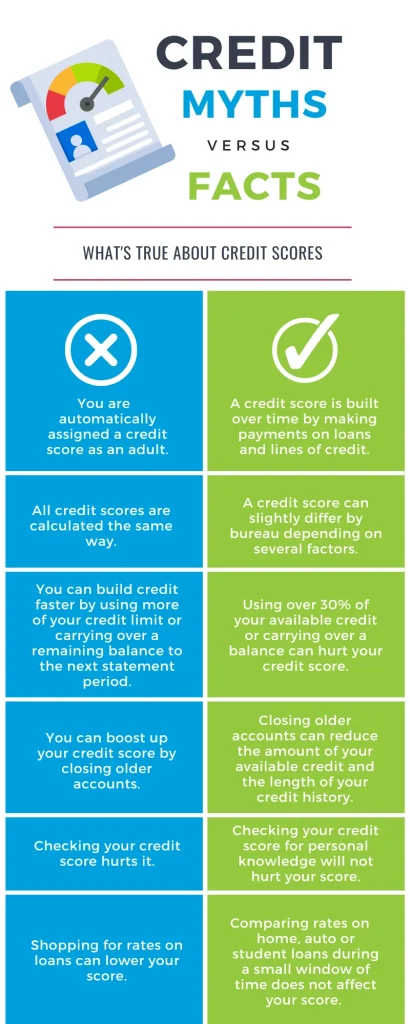

Understanding the credit impact starts with the basics of how credit scores are calculated. The most widely used FICO model weighs the following factors:

- Payment History (35%): Timely payments keep this slice healthy.

- Amounts Owed (30%): This looks at credit utilization and the total debt you owe.

- Length of Credit History (15%): Older accounts contribute positively.

- New Credit (10%): Recent hard inquiries and newly opened accounts.

- Credit Mix (10%): Variety of credit types (installments, revolving, etc.)

When you consolidate student loans, you’re essentially swapping a handful of installment accounts for a single new installment account. This shift triggers changes across several of those categories, which is why the short answer—yes, it can affect your credit score—needs a nuanced explanation.

does consolidating student loans affect credit score: Immediate Credit Inquiry

The first credit event you’ll notice is a hard inquiry. When a lender pulls your credit report to evaluate eligibility for a consolidation loan, the inquiry shows up on your report for up to two years, but it only impacts your score for the first 12 months. A single hard pull typically knocks off 5–10 points, which is a modest dip. However, if you shop around and submit multiple applications in a short window, the cumulative effect can be more noticeable.

does consolidating student loans affect credit score: Opening a New Account

Once approved, the new consolidation loan becomes a fresh installment account. This adds to your “new credit” factor—another slight dip. Simultaneously, the average age of your credit accounts may shrink, especially if you’ve had your original student loans for several years. A younger average age can tug at the “length of credit history” slice, potentially lowering your score a bit.

does consolidating student loans affect credit score: Closing Old Loans

Most consolidation processes involve paying off the original loans, which means those accounts close. Closing installment accounts doesn’t directly impact credit utilization (since that metric focuses on revolving credit), but it does affect your overall debt amount. If the consolidated loan’s balance is lower than the combined balances of the original loans, the “amounts owed” factor could improve, nudging your score upward.

Conversely, if the new loan has a higher balance—perhaps because you rolled in additional debt or extended the repayment term—your total debt might increase, which could weigh negatively on the “amounts owed” component.

Long‑Term Credit Implications of Consolidation

While the immediate score fluctuations are usually modest, the long‑term effects hinge on how you manage the new loan. Here’s what to watch for:

- Payment Consistency: A single payment due date can make it easier to stay current. Consistently on‑time payments will reinforce the payment history factor, often boosting your score over time.

- Debt Reduction Strategy: If consolidation lets you secure a lower interest rate, you might pay off the principal faster, reducing the total debt and improving the “amounts owed” metric.

- Credit Mix: Adding another installment loan doesn’t drastically change your credit mix, but if you previously only had revolving credit (like credit cards), the new installment loan can diversify your mix, potentially adding a few points.

In short, the long‑term impact is less about the act of consolidation itself and more about the repayment behavior it encourages. If you’re disciplined, consolidation can be a credit‑building tool; if you fall behind, it can amplify the negative impact.

Common Myths About Consolidation and Credit Scores

Let’s bust a few myths that often cause confusion:

Myth 1: Consolidation Always Improves Your Score

Not true. If you consolidate into a higher‑balance loan or miss payments on the new account, your score can suffer. The key is to ensure the new terms align with your financial capacity.

Myth 2: Closing Original Loans Erases Their Positive History

Closed accounts in good standing remain on your credit report for up to ten years, continuing to contribute to your payment history. So, you won’t lose that goodwill—just the open‑account benefit.

Myth 3: You Can’t Consolidate Federal and Private Loans Together

While federal consolidation (through a Direct Consolidation Loan) can’t mix with private loans, you can use a private refinance loan to combine both types. The credit impact principles stay the same, though the process differs.

Strategic Tips to Minimize Negative Credit Impacts

If you decide that consolidation is the right move, follow these tactics to keep your credit score healthy:

- Shop Within a Short Window: Most credit scoring models treat multiple inquiries for the same type of loan as one, as long as they occur within a 30‑day window. This minimizes hard pull damage.

- Choose a Lender That Reports Promptly: Timely reporting ensures your on‑time payments are reflected quickly, helping build a positive payment history.

- Maintain Low Balances on Revolving Accounts: Since consolidation won’t affect credit utilization on credit cards, keep those balances low to protect that portion of your score.

- Set Up Automatic Payments: Auto‑pay not only reduces missed‑payment risk but often qualifies you for an interest‑rate discount.

- Monitor Your Credit Reports: Use free annual credit reports to verify that the old loans are marked as “paid in full” and that the new loan is accurately recorded.

For a deeper look at how loan terms affect repayment, you might also want to read What is Grace Period for Student Loans? Everything You Need to Know. Understanding the grace period can help you schedule payments strategically during consolidation.

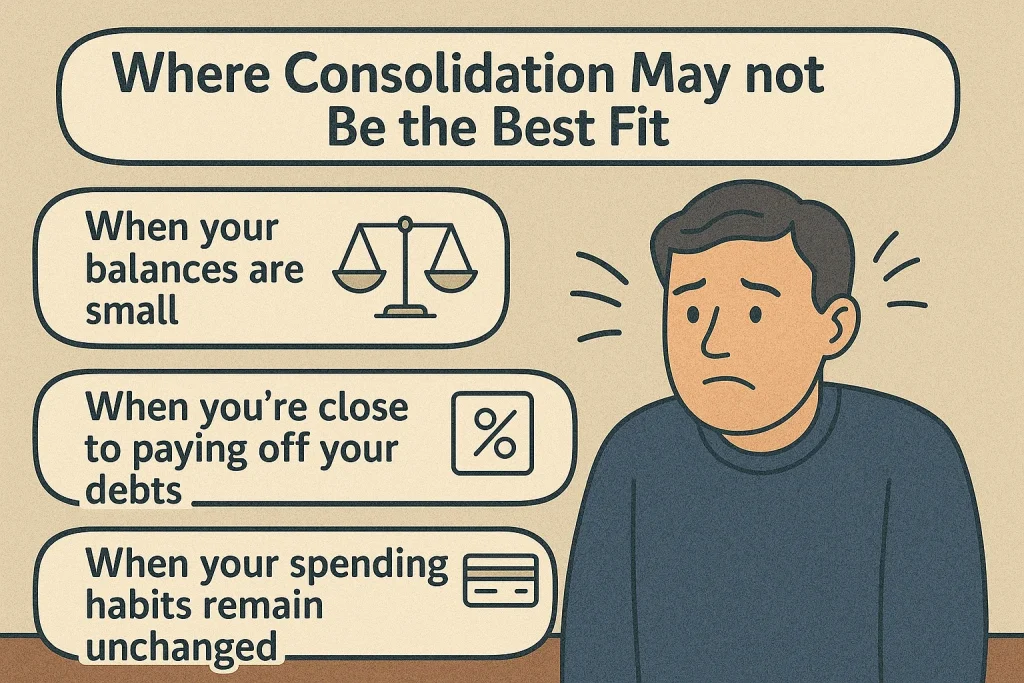

When Consolidation Might Not Be Worth It

Even if you’re excited about a single payment, consider these scenarios where consolidation could be more harmful than helpful:

- Loss of Federal Benefits: Federal loans offer income‑driven repayment plans, deferment, forbearance, and forgiveness options. Consolidating into a private loan strips away these protections.

- Higher Overall Cost: Extending the loan term can lower monthly payments but increase total interest paid, potentially inflating the “amounts owed” factor.

- Credit Score Sensitivity: If you’re planning a major credit event soon—like buying a home—any dip, however small, could affect loan eligibility or interest rates.

If you’re in any of these situations, it may be wiser to explore alternative strategies such as income‑driven repayment plans or targeted refinancing of only the highest‑interest loans. The What Does Refinancing a Student Loan Mean? A Full Guide article offers a solid comparison of refinancing vs. consolidation.

Real‑World Example: Emma’s Journey

Emma, a 27‑year‑old graphic designer, had three federal loans: $8,000 at 4.5%, $5,000 at 5.0%, and $12,000 at 6.8%. She was making $55,000 a year and struggled to keep track of three due dates. After researching, she opted for a private consolidation loan of $25,000 at 5.5% over a 10‑year term.

- Credit Impact: Emma’s credit score dropped 8 points after the hard inquiry and new account opened. Over the next six months, her score rebounded to its original level thanks to consistent on‑time payments.

- Financial Outcome: Her monthly payment fell from $370 across three loans to $270 on the consolidated loan, freeing $100 each month for savings.

- Long‑Term Effect: After two years, Emma’s total interest paid was $5,200—slightly higher than she would have paid on the original loans—but the simplicity and reduced stress outweighed the extra cost.

Emma’s story illustrates that while the short‑term credit dip is real, disciplined repayment can not only recover the score but also provide financial peace of mind.

Bottom Line: Weighing the Credit Trade‑Offs

So, does consolidating student loans affect credit score? The answer is a nuanced yes. The process triggers a hard inquiry, adds a new account, and closes old ones—all of which can cause a modest, temporary dip. However, the real credit impact depends on the downstream effects: payment history consistency, total debt reduction, and how you manage the new loan.

If you’re proactive—shop wisely, lock in a lower interest rate, and stay on top of payments—consolidation can become a credit‑friendly move that simplifies finances and potentially improves your score over time. Conversely, if you sacrifice federal protections or end up with higher debt, the credit consequences can be negative.

Before you make a decision, run the numbers, consider your short‑term credit goals (like buying a house), and think about the long‑term financial picture. And don’t forget to explore related topics such as the Income Limit for Student Loan Interest Deduction Explained to maximize tax benefits while you navigate consolidation.

At the end of the day, consolidating student loans is a tool—one that can either smooth the road to financial stability or add a new set of bumps if misused. Use it wisely, monitor your credit, and you’ll be on track to keep both your debt and your credit score in good shape.

[Finance]: Finance