Getrawbox Getrawbox

Getrawbox Getrawbox

Related Articles

Misplacing the name of the company that handles your student loan can feel like losing the key to a treasure chest—except the treasure is your financial peace of mind. Whether you’re just graduating, considering repayment options, or simply want to verify the details of your loan, knowing how to find my student loan servicer is essential. The good news? You don’t need a detective’s magnifying glass; most of the clues are right at your fingertips.

In this guide we’ll walk through the most reliable methods to uncover the servicer’s identity, verify contact information, and keep your loan records organized. Along the way we’ll sprinkle in a few tips about related topics—like using a 401k to pay student loans or understanding how consolidation can affect your credit score—so you’ll walk away with a well‑rounded view of student loan management.

how to find my student loan servicer: official resources and quick checks

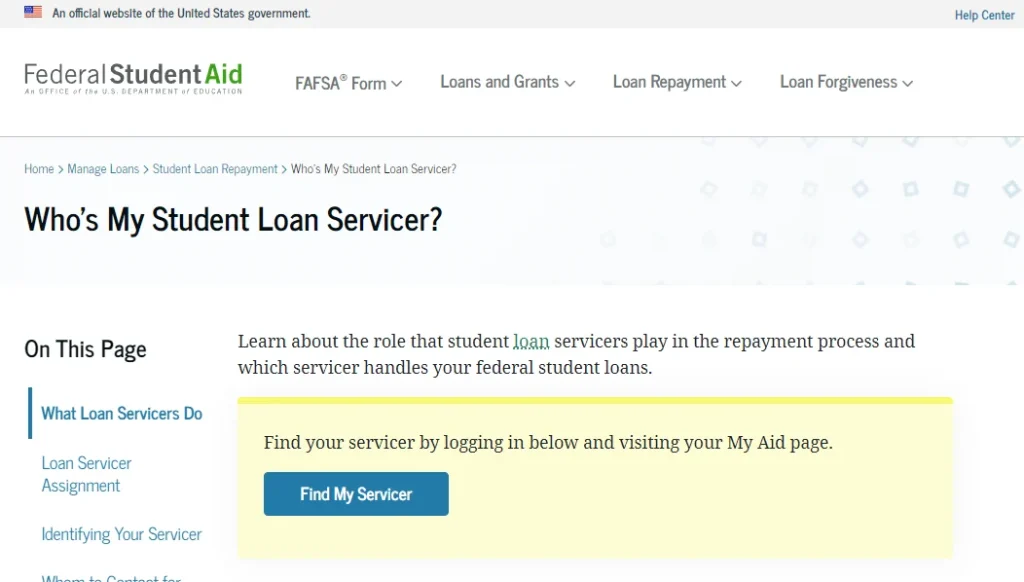

The first place to start when you’re wondering how to find my student loan servicer is the federal government’s own portal. If your loan is federal, the National Student Loan Data System (NSLDS) holds a comprehensive record of every loan you’ve taken out, including the servicer’s name and contact details. Log in with your FSA ID, and you’ll see a clear summary of all active loans.

For private loans, the approach is slightly different. Private lenders usually provide a welcome packet or an email confirmation that includes servicer information. If you can’t locate that paperwork, check your email for keywords like “loan account,” “servicer,” or “payment schedule.” Most lenders also have an online account portal; entering your Social Security number and date of birth should pull up the necessary details.

Step‑by‑step: how to find my student loan servicer using online tools

- Federal loans: Visit studentaid.gov and click “Log In” under the “My Aid” section. After signing in, select “View My Loan Details.” The servicer’s name, phone number, and website will be displayed next to each loan.

- Private loans: Go to the lender’s official website. Look for a “Student Loan” or “My Account” link. If you’re unsure of the lender, try searching your email for the original loan agreement or any billing statements.

- Credit report: Pull a free credit report from AnnualCreditReport.com. Under the “Loans” section, you’ll see entries for each student loan, often listing the servicer as the creditor.

- Contact your school’s financial aid office: They keep records of where they sent your loan documents and can confirm the current servicer.

Remember, the keyword “how to find my student loan servicer” isn’t just a phrase—it’s a prompt for action. By following these steps, you’ll have the servicer’s name and contact info in hand within minutes.

What to do once you’ve identified your servicer

Finding the servicer is half the battle; the next phase is making sure you’re set up for smooth communication. Create a dedicated folder—digital or physical—where you store all correspondence, payment confirmations, and statements. Most servicers offer an online dashboard; logging in regularly helps you keep tabs on balances, interest accrual, and upcoming due dates.

If you discover that your loan has been transferred to a new servicer (a common occurrence after consolidation or acquisition), verify the transition date. Some borrowers miss payments during the hand‑off, which can lead to unnecessary fees or a temporary dip in credit score.

Helpful resources while you navigate your loan

While you’re sorting out the details, you might be contemplating other financial strategies. For instance, using your 401k to pay student loans can seem attractive, but it carries tax implications and potential penalties. Understanding the trade‑offs before tapping retirement savings is crucial.

Another common question is whether consolidating loans will impact your credit. A solid read on this is student loan consolidation and credit score. The article explains how a new consolidation loan creates a fresh credit inquiry but can also simplify payments and lower your monthly amount.

Common pitfalls and how to avoid them

Even after you know how to find my student loan servicer, certain missteps can still trip you up. Below are the most frequent issues and quick fixes.

- Outdated contact info: Servicers may change phone numbers or email addresses. Always confirm the latest details on the official website rather than relying on old emails.

- Missing payments during a transfer: When a loan moves to a new servicer, set up automatic payments a few days before the transition to avoid a gap.

- Confusing multiple servicers: If you have both federal and private loans, you’ll likely have two different servicers. Keep separate logs for each to avoid mixing up due dates.

- Ignoring the grace period: Grace period for student loans varies by loan type. Knowing when it ends helps you plan your first payment and prevents accidental default.

How to verify the servicer’s legitimacy

Scams targeting borrowers have risen, especially during tax season. To confirm you’re dealing with the right entity, compare the phone number you have with the one listed on the Federal Student Aid website or your lender’s official site. Never click on links from unsolicited emails; instead, type the URL directly into your browser.

Staying proactive: monitoring and future steps

Now that you’ve mastered how to find my student loan servicer, keep the momentum going by setting up alerts. Most servicers allow you to receive email or SMS notifications for upcoming payments, balance changes, or important policy updates.

Regularly review your loan statements for any discrepancies. If you spot an unexpected fee, contact the servicer immediately—most issues can be resolved quickly when you have documentation ready.

Lastly, think ahead. As you progress in your career, you may become eligible for income‑driven repayment plans, loan forgiveness programs, or even the ability to refinance at a lower rate. Having a clear record of who services each loan makes the application process for these options much smoother.

In a nutshell, knowing how to find my student loan servicer empowers you to take control of your repayment journey. By leveraging official portals, credit reports, and your school’s financial aid office, you’ll always have the right contact at your fingertips. Keep your information organized, stay alert to changes, and use the resources mentioned to make informed decisions about your broader financial health.