Getrawbox Getrawbox

Getrawbox Getrawbox

Related Articles

Starting a new venture is exciting, but before you can accept payments, pay suppliers, or keep your personal and company money separate, you’ll need a solid financial foundation. One of the first milestones for any entrepreneur is to apply for a business bank account. It might sound simple, but the process can be a maze of paperwork, eligibility checks, and subtle differences between banks.

In this article we’ll walk you through everything you need to know: why a dedicated business account matters, which documents you’ll have to gather, how to compare banks, and the exact steps to submit your application. Whether you’re a sole proprietor, an LLC, or a corporation, the guidance here works for every structure. By the end, you’ll feel confident to click “Submit” and start managing your business finances like a pro.

Before diving into the nitty‑gritty, keep in mind that the right bank can save you time, money, and headaches down the road. Look for features such as low fees, integrated accounting tools, easy online access, and good customer support. If you’re still unsure which option fits best, you might want to read how to open a small business bank account online for a broader perspective on digital solutions.

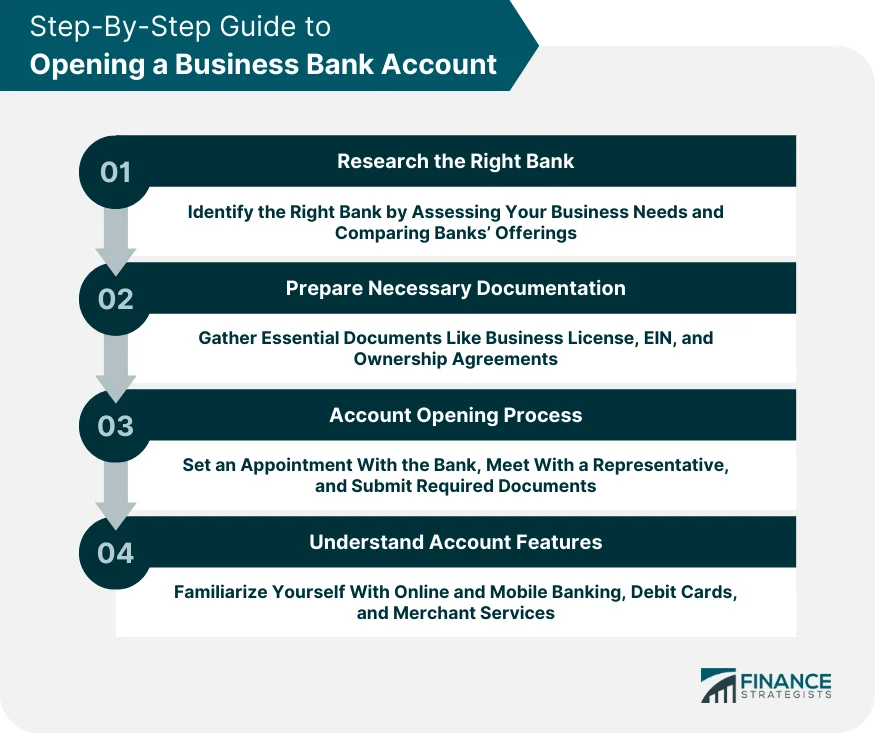

apply for a business bank account: The Essential Checklist

![How To Open a Business Bank Account in 7 Steps [+Checklist]](https://getrawbox.com/wp-content/uploads/2026/02/how-to-open-a-business-bank-account-in-7-steps-checklist.webp)

When you decide to apply for a business bank account, treat the process like a mini‑project. Having a clear checklist helps you stay organized and speeds up approval. Below is a comprehensive list of items you’ll typically need:

- Legal business name and DBA (Doing Business As) registration. The bank will verify that your name matches official records.

- Employer Identification Number (EIN) or Social Security Number. Sole proprietors can often use an SSN, but an EIN adds credibility.

- Formation documents. Articles of incorporation, LLC operating agreement, or partnership agreement, depending on your structure.

- Personal identification. A government‑issued ID (driver’s license, passport) for every signatory.

- Proof of address. Utility bill, lease agreement, or a recent bank statement.

- Business license or permits. Required for certain industries like food service or construction.

- Initial deposit. Some banks demand a minimum opening balance; others waive it for online accounts.

Having these documents ready before you begin the application will keep the experience smooth and prevent the dreaded “please provide additional information” emails.

Why you should apply for a business bank account early

Opening the account early—ideally before you make your first sale—offers several strategic advantages:

- Separate finances. Keeps personal and business expenses distinct, simplifying bookkeeping and protecting personal assets.

- Professional image. Customers and vendors see a business name on checks and invoices, building trust.

- Access to business‑specific services. Credit cards, lines of credit, merchant services, and payroll solutions are usually only available to business account holders.

- Better tax preparation. A dedicated account creates a clear audit trail, making it easier to claim deductions.

For many startups, the choice of bank also influences future financing opportunities. Lenders often look at the health of your business checking account when assessing creditworthiness.

Where to apply for a business bank account: Traditional vs. Online

Not all banks are created equal. Traditional brick‑and‑mortar banks offer personal relationships and in‑person support, while online‑only banks tend to have lower fees and faster onboarding. Below we compare the two major approaches.

Traditional banks

- Pros: Face‑to‑face assistance, established reputation, and often a wider range of loan products.

- Cons: Higher monthly fees, stricter minimum balances, and longer paperwork cycles.

If you value a local branch you can walk into for cash deposits, consider a big‑name institution. You might also enjoy the convenience of linking a business account with a personal checking account at the same bank.

Online banks and fintechs

- Pros: Minimal fees, quick digital onboarding, and seamless integration with accounting software like QuickBooks or Xero.

- Cons: No physical branches, limited cash‑handling options, and sometimes fewer credit products.

Many entrepreneurs find an online solution perfect for a lean startup. If you want to see a concrete example, check out business bank account for LLC online for a step‑by‑step walkthrough.

Step‑by‑step guide to apply for a business bank account

Now that you understand the why and where, let’s dive into the actual application process. Follow these nine steps, and you’ll be well on your way to a functional business banking relationship.

- Research and shortlist banks. Use the checklist above to compare fees, features, and eligibility. Look for banks that specifically mention “business checking” and note any promotional offers.

- Gather required documents. Double‑check that you have all identification, formation papers, and the EIN. Store them as PDFs for easy upload.

- Complete the online or in‑person application. Enter your legal business name exactly as it appears on registration documents. Mis‑spelling can cause delays.

- Provide personal information for each signatory. This includes SSN/EIN, address, and a government ID scan.

- Answer compliance questions. Banks must verify you’re not on any sanctions list and that your business isn’t high‑risk (e.g., adult entertainment, cryptocurrency exchanges).

- Fund the account. Transfer the required opening deposit via ACH, wire, or a cash deposit at a branch.

- Set up online banking. Enable two‑factor authentication, link your accounting software, and order debit/credit cards.

- Order additional services. Consider merchant processing, payroll integration, or a line of credit if you anticipate growth.

- Verify and test. Make a small deposit or payment to confirm everything works. Review statements for any unexpected fees.

Throughout the process, keep an eye on your email inbox. Banks often request additional documentation within 24‑48 hours, and a prompt response can shave days off the timeline.

Common pitfalls to avoid when you apply for a business bank account

- Using the wrong business name. Always match the exact legal name on your formation documents.

- Missing EIN. Even sole proprietors benefit from an EIN; it separates your personal SSN from the business.

- Overlooking fees. Some banks waive monthly fees if you maintain a minimum balance; others charge per transaction. Calculate the total cost based on your expected volume.

- Neglecting to read the fine print. Look for hidden costs such as wire fees, inbound ACH fees, or fees for printed checks.

- Choosing a bank without the right integrations. If you use QuickBooks, make sure the bank offers direct feed to avoid manual data entry.

By staying vigilant on these points, you’ll reduce the chance of a surprise fee or a delayed account activation.

Special considerations for different business structures

While the core steps to apply for a business bank account remain consistent, certain entities have unique requirements.

Sole Proprietorships

For a sole proprietorship, the process is often the simplest. You can usually use your Social Security Number instead of an EIN, and the formation documents are limited to a DBA registration. However, many experts still recommend obtaining an EIN to keep your personal credit separate.

Read more about this approach in the guide Open Sole Proprietorship Bank Account Online.

Limited Liability Companies (LLCs)

LLCs need an EIN, Articles of Organization, and an operating agreement that lists the members who will have signing authority. Some banks also request a resolution authorizing the opening of the account, especially if the LLC has multiple members.

If you want a deep dive, check out Business Bank Account for LLC Online: A Complete Guide for nuances such as “member‑only” versus “manager‑only” authority.

Corporations (C‑Corp & S‑Corp)

Corporations must provide Articles of Incorporation, a corporate resolution, and a list of authorized signatories with corporate titles. Banks may also ask for a copy of the most recent bylaws and a corporate seal, though the latter is less common today.

Because corporations often need credit lines early on, selecting a bank with a strong commercial lending division can be beneficial.

After you’ve applied: Managing your new business account

Opening the account is only the beginning. To get the most out of your business bank account, follow these best practices:

- Reconcile weekly. Match your bank statements with your bookkeeping software to catch errors early.

- Separate payroll. Use a dedicated sub‑account or a payroll service linked to your business account to avoid commingling.

- Monitor fees. Set up alerts for any fee charges so you can negotiate or switch banks if necessary.

- Leverage cash flow tools. Many banks offer forecasting dashboards that predict low‑balance periods and suggest short‑term financing.

- Maintain good standing. Keep the minimum balance, avoid overdrafts, and respond quickly to any compliance requests.

Remember that your bank relationship can evolve. As your business scales, you may qualify for a treasury management suite, merchant cash advances, or a dedicated relationship manager.

For a quick refresher on how to add a bank account to a brokerage platform, see How to Add Bank Account to E*TRADE – Step‑by‑Step Guide. The steps are similar, and mastering one makes the other feel routine.

Finally, if you ever need a backup plan, consider a second‑chance account or a separate “operating” account to keep essential cash flow flowing while you sort out any issues.

Securing a business bank account may feel like a bureaucratic hurdle, but with the right preparation it becomes a straightforward step toward financial stability. By understanding the documents you need, the type of bank that fits your style, and the exact actions required to apply for a business bank account, you set the stage for smoother operations, clearer accounting, and easier access to future financing.

Now that you’ve read the roadmap, take a deep breath, pick a bank from your shortlist, and start the application. Your business’s financial future is just a few clicks away.