Getrawbox Getrawbox

Getrawbox Getrawbox

Related Articles

In the fast‑moving world of property transactions, agents are always on the hunt for the next client, the next listing, the next commission. One model that’s been gaining traction lately is the “real estate leads pay at closing” arrangement. Instead of paying upfront for a lead that may never convert, agents only part with a fee when the deal actually closes. It sounds like a win‑win, but like any payment structure, it comes with its own set of nuances.

Understanding how real estate leads pay at closing works can reshape your budgeting, your risk tolerance, and even the way you approach lead nurturing. This article dives deep into the mechanics, the benefits, the potential pitfalls, and practical tips to make this model work for you. Whether you’re a solo agent, part of a boutique brokerage, or managing a larger team, the insights here will help you decide if this payment style aligns with your business goals.

Before we get into the nitty‑gritty, let’s set the stage with a quick comparison. Traditional lead purchase usually requires a flat fee or a per‑lead cost paid up front, regardless of outcome. The “pay‑at‑closing” model flips that script: you only pay when the lead turns into a closed transaction. This shift can dramatically affect cash flow, marketing ROI, and even your relationship with lead‑generation partners.

real estate leads pay at closing: What You Need to Know

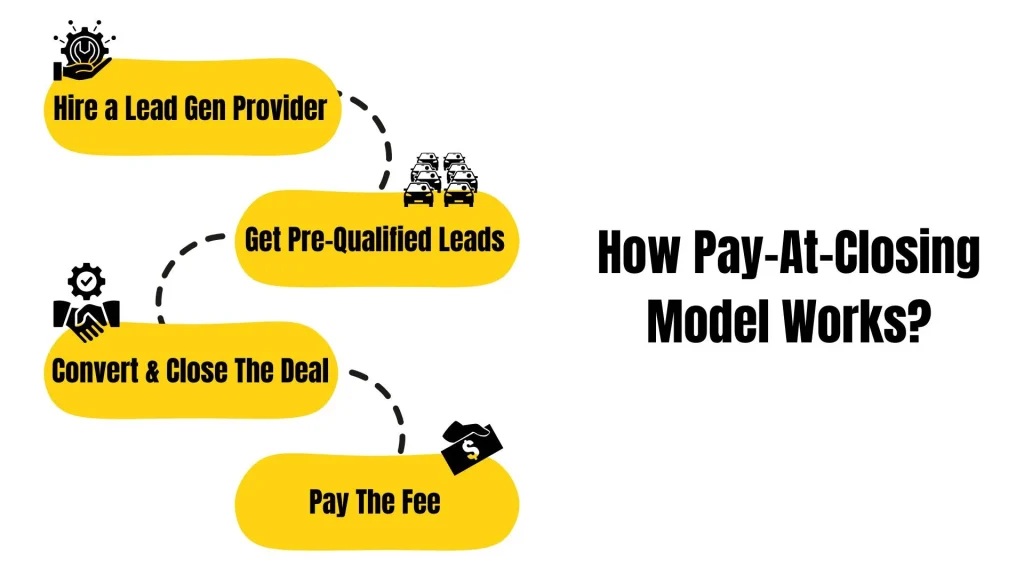

The core premise of real estate leads pay at closing is straightforward: the lead provider—whether it’s a third‑party vendor, a referral network, or a co‑broker—receives compensation only after the transaction is finalized. The fee is typically expressed as a percentage of the agent’s commission or as a flat amount agreed upon beforehand. Because the payment is tied directly to a successful closing, the risk for the agent is reduced, while the lead source assumes more of the risk.

This model is especially appealing for newer agents who may not have deep pockets to front large lead‑buying budgets. It also resonates with seasoned professionals who prefer performance‑based spending over speculative costs.

How real estate leads pay at closing affect your cash flow

Cash flow is the lifeblood of any real‑estate operation. When you adopt a real estate leads pay at closing system, the immediate outlay is minimal. You can allocate funds that would otherwise be locked up in lead purchases toward other business‑critical activities—marketing, technology, or even personal development.

- Reduced upfront risk: No need to gamble on leads that never convert.

- Predictable expense: Since the fee is tied to a closed deal, you can calculate the exact cost as a percentage of the commission you’ll earn.

- Improved budgeting: Your monthly expenses become more aligned with actual revenue, making financial planning smoother.

On the flip side, because the fee is deducted from the commission you receive at closing, it can slightly reduce your net earnings per transaction. That’s why it’s crucial to negotiate a fair percentage and to understand the typical conversion rates of the leads you’re buying.

Key Benefits of the Pay‑At‑Closing Model

1. Performance‑Based Cost Structure – Since you only pay when a deal closes, you’re essentially paying for results, not promises.

2. Higher Lead Quality Incentive – Lead providers have a strong incentive to deliver highly qualified prospects because their revenue depends on it.

3. Lower Financial Barrier to Entry – New agents can test different lead sources without the fear of sunk costs.

4. Better Alignment with Client Interests – When both agent and lead source benefit from a successful transaction, the focus stays on serving the client rather than chasing volume.

Potential Drawbacks and How to Mitigate Them

While the advantages are compelling, there are a few considerations to keep in mind:

- Higher Long‑Term Cost per Deal: Some providers may charge a larger percentage to compensate for the risk they’re assuming.

- Dependency on Provider’s Vetting Process: If the lead source’s qualification standards slip, you could end up with low‑conversion leads.

- Delayed Revenue Recognition: Since you only pay after closing, you might experience a lag in understanding the true cost of acquisition.

Mitigation strategies include: negotiating caps on the percentage, asking for detailed conversion data, and regularly reviewing the provider’s performance metrics. It’s also wise to maintain a diversified lead portfolio—mix pay‑at‑closing sources with a few high‑quality, low‑cost upfront leads to balance risk.

Choosing the Right Pay‑At‑Closing Lead Provider

Not all lead vendors are created equal. Some specialize in exclusive, highly vetted leads, while others offer mass‑generated contacts that may require more nurturing. Here’s a quick checklist to help you evaluate potential partners:

- Transparency of conversion rates and historical performance.

- Clear fee structure—percentage vs. flat fee.

- Contract flexibility—ability to pause or cancel without hefty penalties.

- Support services—does the provider offer follow‑up assistance or marketing collateral?

For agents looking to streamline the entire process, integrating a virtual assistant services for real estate can be a game‑changer. A virtual assistant can handle initial lead contact, schedule appointments, and even manage the paperwork that comes with a closing, ensuring you stay focused on closing the deal.

Practical Steps to Implement a Pay‑At‑Closing Strategy

1. Assess Your Current Lead Costs – Determine how much you’re spending on leads now and what your average conversion rate looks like.

2. Set a Target Percentage – Decide on a comfortable fee range (e.g., 10‑15% of your commission) that won’t erode your profitability.

3. Test with a Small Batch – Start with a limited number of leads from a new provider to gauge quality before scaling up.

4. Track Every Interaction – Use a CRM (consider a free CRM for real estate agents) to monitor lead status, communication history, and eventual outcomes.

5. Review and Adjust Quarterly – Analyze cost per acquisition, conversion rates, and overall ROI. If a provider isn’t delivering, don’t hesitate to switch.

Legal and Ethical Considerations

When you agree to a pay‑at‑closing arrangement, you’re entering a contract that ties compensation to a future event. Ensure the agreement clearly defines:

- What constitutes a “closed” transaction (e.g., recorded deed, funded mortgage).

- Timeframe for payment after closing.

- Any dispute resolution mechanisms.

Additionally, keep in mind compliance with local real‑estate regulations and fair‑housing laws. Some jurisdictions may have restrictions on how leads can be sourced and compensated. Consulting a liability insurance for real estate agents attorney or broker can help you avoid costly missteps.

Integrating Pay‑At‑Closing Leads with Your Existing Marketing Stack

Even if you adopt a pay‑at‑closing model, you shouldn’t abandon other marketing channels. A balanced mix often yields the best results. Here’s how you can blend the two:

- Content Marketing: Publish blogs, videos, and market reports that attract organic traffic.

- Social Media Advertising: Run targeted ads that generate low‑cost leads to supplement pay‑at‑closing sources.

- Referral Programs: Offer incentives to past clients for referrals, which can act as a hybrid between upfront and performance‑based costs.

By overlaying a lead generation tools for real estate suite onto your workflow, you can automatically score leads, prioritize follow‑ups, and ensure that no opportunity falls through the cracks.

Measuring Success: Key Metrics to Watch

When evaluating a pay‑at‑closing lead program, focus on the following KPIs:

- Cost per Closed Deal: Total fees paid divided by the number of closed transactions.

- Conversion Rate: Leads that move from initial contact to closing.

- Average Time to Close: Helps assess whether the lead quality aligns with your sales cycle.

- Net Commission Retention: Commission after deducting lead fees, showing true profitability.

Regularly reviewing these metrics will let you fine‑tune your provider relationships and fee structures, ensuring the model remains financially viable.

In practice, many agents report that real estate leads pay at closing can shrink their acquisition costs by up to 30% compared to traditional upfront models—provided they partner with reputable vendors and maintain disciplined follow‑up processes.

As the real‑estate landscape continues to evolve, flexibility in how you pay for leads will become a competitive advantage. By embracing a performance‑based approach, you align your expenses directly with revenue, reduce unnecessary risk, and position yourself to scale efficiently.

Ultimately, the decision to adopt real estate leads pay at closing hinges on your business’s financial health, your confidence in lead providers, and your ability to track results meticulously. With the right strategy, this model can transform lead acquisition from a gamble into a predictable, revenue‑driven engine.