Getrawbox Getrawbox

Getrawbox Getrawbox

Related Articles

Real estate development isn’t just about finding a good plot of land and putting up a building. Behind every skyscraper, apartment complex, or mixed‑use project lies a mountain of expenses that need to be tracked, categorized, and reported correctly. When developers get the accounting right, they can spot cost overruns early, secure financing with confidence, and ultimately boost profitability.

But let’s face it: the financial side of a development can feel as complex as the architectural plans. From land acquisition to permitting, from hard‑construction costs to soft‑service fees, each line item has its own set of rules. That’s why a solid grasp of accounting for real estate development costs is essential for anyone serious about turning a blueprint into cash flow.

In this article we’ll break down the main components of development accounting, walk through the most common methods, and share practical tips you can apply to your next project. Whether you’re a seasoned developer, a financial analyst, or just curious about how these numbers come together, you’ll find a roadmap that’s both relaxed and professional.

accounting for real estate development costs: core concepts you need to know

At its heart, accounting for real estate development costs means recording every outlay that contributes to the creation of a real‑estate asset. Unlike standard property accounting—where you might only track rent and maintenance—development accounting captures the entire life cycle from pre‑development through construction to completion.

Key steps in accounting for real estate development costs

- Identify and categorize expenses: Split costs into land, soft costs (permits, design, legal), hard costs (materials, labor), financing, and post‑completion items.

- Choose a cost‑allocation method: Most developers use either the completed‑contract method or the percentage‑of‑completion method to recognize revenue and expenses.

- Set up a dedicated project ledger: Keep each development in its own accounting bucket to avoid commingling with other assets.

- Monitor budgets vs. actuals: Regular variance analysis helps you catch overruns before they become crises.

- Prepare financial statements and disclosures: Accurate reporting is required for lenders, investors, and tax authorities.

Understanding these steps gives you a solid foundation, but the real art lies in how you treat each cost category.

Breaking down the cost categories

Land acquisition costs

Land is often the single biggest upfront expense. When accounting for real estate development costs, you record the purchase price, title fees, and any related due‑diligence expenses. If the land is held for future development, it’s usually listed as a long‑term asset on the balance sheet. Once development begins, you may need to reclassify part of the land cost to “construction in progress” under certain accounting standards.

Soft costs

Soft costs include everything that doesn’t directly touch the building’s physical structure. Think architectural and engineering fees, permits, impact fees, environmental studies, legal services, and marketing expenses. Although they’re “soft,” they’re anything but insignificant—soft costs can easily eat up 20‑30 % of a project’s total budget.

For developers looking to boost lead flow while keeping marketing budgets lean, checking out free real estate leads for agents can be a smart move. The guide walks you through cost‑effective lead generation tactics that fit nicely into the soft‑cost budget.

Hard costs

Hard costs are the tangible construction expenses: concrete, steel, labor, HVAC systems, roofing, and interior finishes. Because they’re the most visible portion of the budget, they’re also the most heavily scrutinized by lenders. Accurate job‑cost accounting software can track each invoice, change order, and subcontractor payment in real time.

Financing costs

Interest on construction loans, loan fees, and commitment costs fall under financing costs. Under the completed‑contract method, you typically capitalize these costs as part of the asset’s basis. With the percentage‑of‑completion method, you allocate interest proportionally as the project progresses.

Post‑completion costs

Even after the building is ready for occupancy, you may incur costs for lease‑up activities, tenant improvements, and warranty work. These are usually expensed as incurred, unless they directly add to the asset’s value, in which case they’re capitalized.

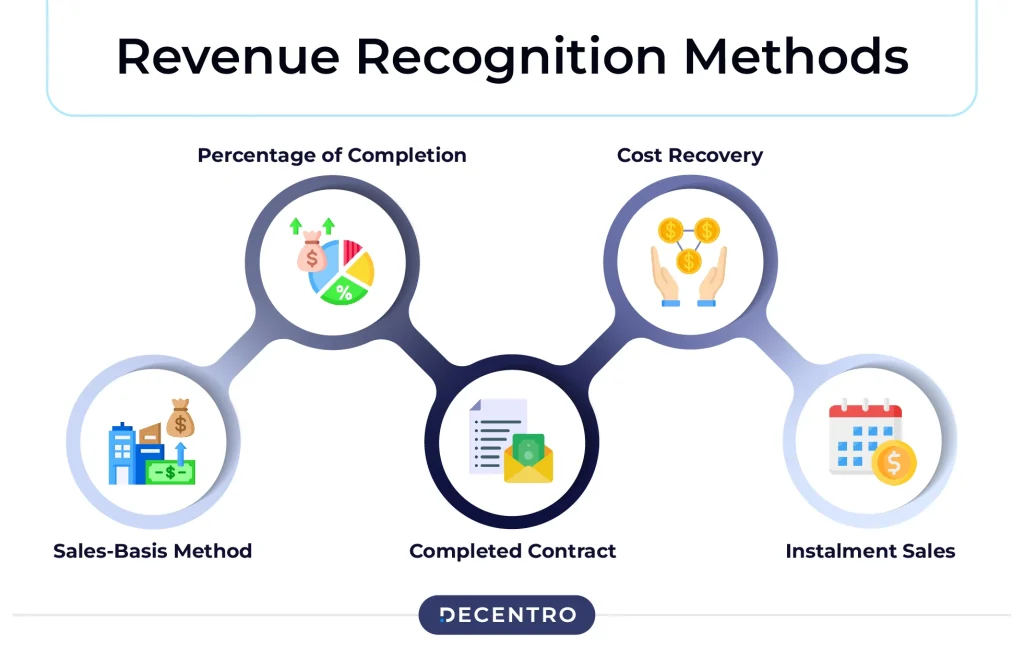

Choosing the right revenue recognition method

The two most common methods—completed‑contract and percentage‑of‑completion—have distinct implications for how you record development costs.

Completed‑contract method

Under this approach, you defer all revenue and expense recognition until the project is finished. It’s simpler and often preferred for short‑term projects or when there’s significant uncertainty about final costs. However, it can create a “boom‑or‑bust” effect on earnings, showing large spikes once a project wraps.

Percentage‑of‑completion method

This method spreads revenue and expenses over the life of the project based on the proportion of work completed. It provides a smoother earnings profile, which lenders and investors appreciate. The challenge is accurately estimating the percentage complete—a task that relies on reliable cost data and solid project management.

Whichever method you choose, consistency is key. Switching methods mid‑project can raise red flags with auditors and tax authorities.

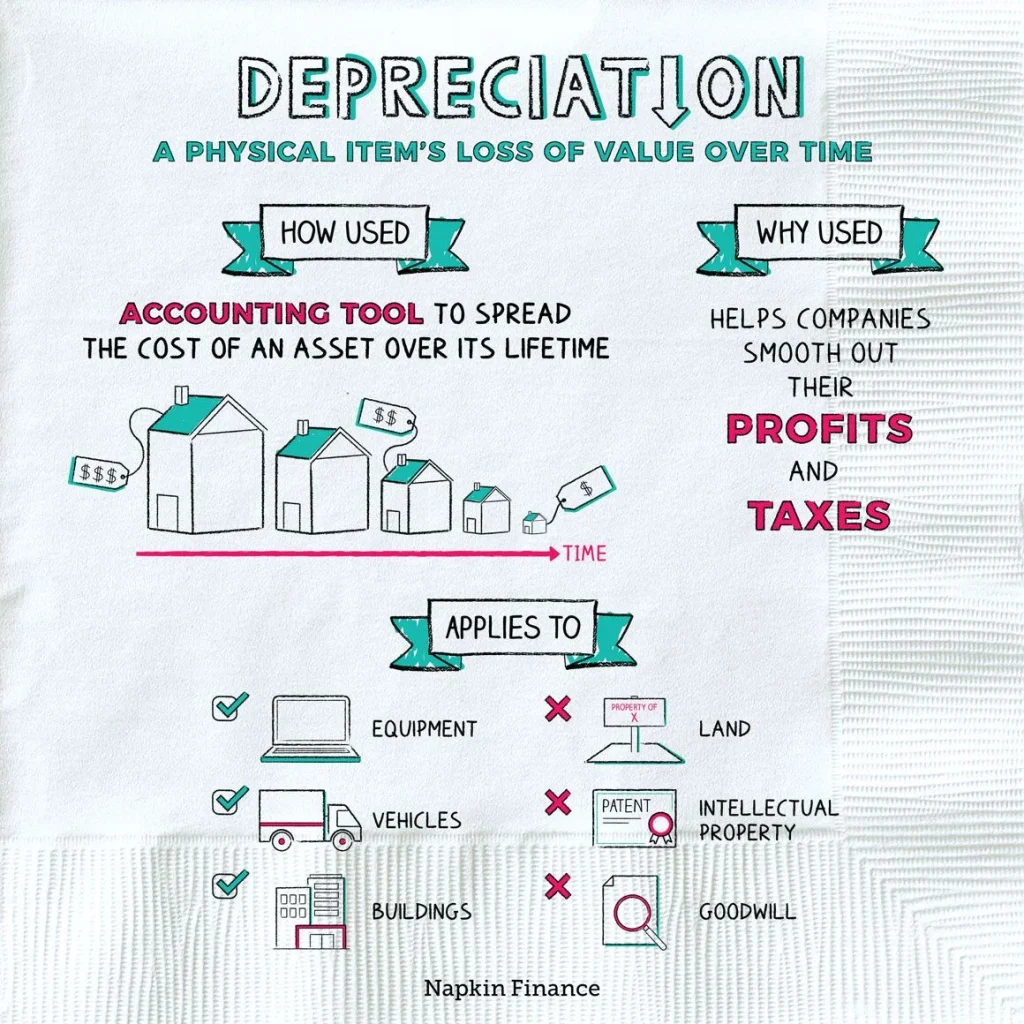

Tax considerations and depreciation

Tax rules add another layer of complexity to accounting for real estate development costs. In many jurisdictions, you can capitalize certain expenses and then depreciate the asset over its useful life, reducing taxable income.

Capitalization vs. expense

Generally, costs that directly contribute to the creation or improvement of the property are capitalized. Examples include land purchase, construction, and major system installations. Conversely, routine maintenance, advertising, and some financing fees are expensed in the period incurred.

Section 179 and bonus depreciation

In the U.S., Section 179 allows you to expense qualifying assets up to a certain limit in the first year, while bonus depreciation can accelerate deductions for certain property classes. These provisions can dramatically impact cash flow, but they’re subject to phase‑outs and eligibility rules.

Tax credits and incentives

Many local governments offer tax credits for affordable housing, green building, or historic preservation. Properly accounting for these incentives can lower your effective tax rate and improve project viability. Make sure to track the credit amounts as a reduction of tax expense, not as revenue.

Technology tools that simplify development accounting

Modern accounting software tailored to construction and real estate can automate many of the tedious tasks we’ve discussed. From integrated budgeting to real‑time cost tracking, these tools help ensure that your accounting for real estate development costs stays accurate and audit‑ready.

If you’re also looking to boost your digital presence, learning how to build a high‑converting website can bring in more clients and investors. The article how to create a website for real estate that sells offers practical steps that align perfectly with your marketing budget.

Best practices for staying on top of development costs

- Maintain a master budget: Start with a detailed line‑item budget and update it regularly as bids come in and change orders are issued.

- Implement a robust change‑order process: Every scope change should be documented, cost‑estimated, and approved before work begins.

- Conduct weekly variance reviews: Compare actual costs to budgeted amounts and investigate any significant deviations.

- Use job‑cost accounting software: Tools that link purchase orders, invoices, and time‑cards reduce manual entry errors.

- Engage with your lender early: Transparent cost reporting builds trust and can lead to better financing terms.

- Plan for contingencies: Set aside 5‑10 % of the budget for unexpected expenses; treat it as a separate line item.

Real‑world example: From land purchase to lease‑up

Imagine a developer acquiring a 2‑acre parcel for $2 million. The project includes $1 million in soft costs (architectural fees, permits), $8 million in hard construction costs, $500 k in financing fees, and $300 k in post‑completion marketing.

Using the percentage‑of‑completion method, the developer estimates the project will be 40 % complete after six months, having spent $5 million. The accounting entry would recognize 40 % of the total projected revenue (say $15 million) and match it with the $5 million in costs, yielding a proportional profit for the period.

Throughout the process, the developer updates the project ledger, tracks every invoice, and runs weekly variance reports. By the time construction finishes, the financial statements clearly show the total capitalized cost of $11.8 million (land + soft + hard + financing) and the resulting asset value, ready for depreciation and future sale analysis.

Common pitfalls and how to avoid them

Even seasoned developers can stumble when it comes to accounting for real estate development costs. Below are some frequent mistakes and quick fixes.

Pitfall: Mixing personal and project expenses

Solution: Use a separate bank account and accounting code for each project. This segregation simplifies audits and protects you from inadvertent tax issues.

Pitfall: Under‑estimating soft costs

Solution: Conduct a thorough pre‑development feasibility study that includes all regulatory, design, and marketing expenses. Include a contingency line for soft‑cost overruns.

Pitfall: Ignoring tax credit timelines

Solution: Track the application dates and compliance requirements for any incentives. Set calendar reminders to file required documentation before deadlines.

Pitfall: Delayed cost recognition

Solution: Adopt the percentage‑of‑completion method if you need smoother earnings reporting, and ensure your cost allocation metrics are updated weekly.

Putting it all together: A checklist for each development project

- Define the project scope and develop a detailed budget.

- Set up a dedicated project ledger in your accounting system.

- Classify every expense (land, soft, hard, financing, post‑completion).

- Select the appropriate revenue recognition method.

- Implement a change‑order approval workflow.

- Track actual costs against budget weekly.

- Prepare interim financial statements for lenders/investors.

- Identify and apply any tax credits or incentives.

- Finalize accounting entries at project completion.

- Begin depreciation schedule and plan for asset disposition.

Following this checklist helps you keep the accounting for real estate development costs transparent, accurate, and compliant—key ingredients for a successful venture.

At the end of the day, meticulous accounting isn’t just a regulatory requirement; it’s a strategic advantage. By understanding where every dollar goes, you can make smarter decisions, protect your margins, and build a reputation for delivering projects on budget and on time.