Getrawbox Getrawbox

Getrawbox Getrawbox

Related Articles

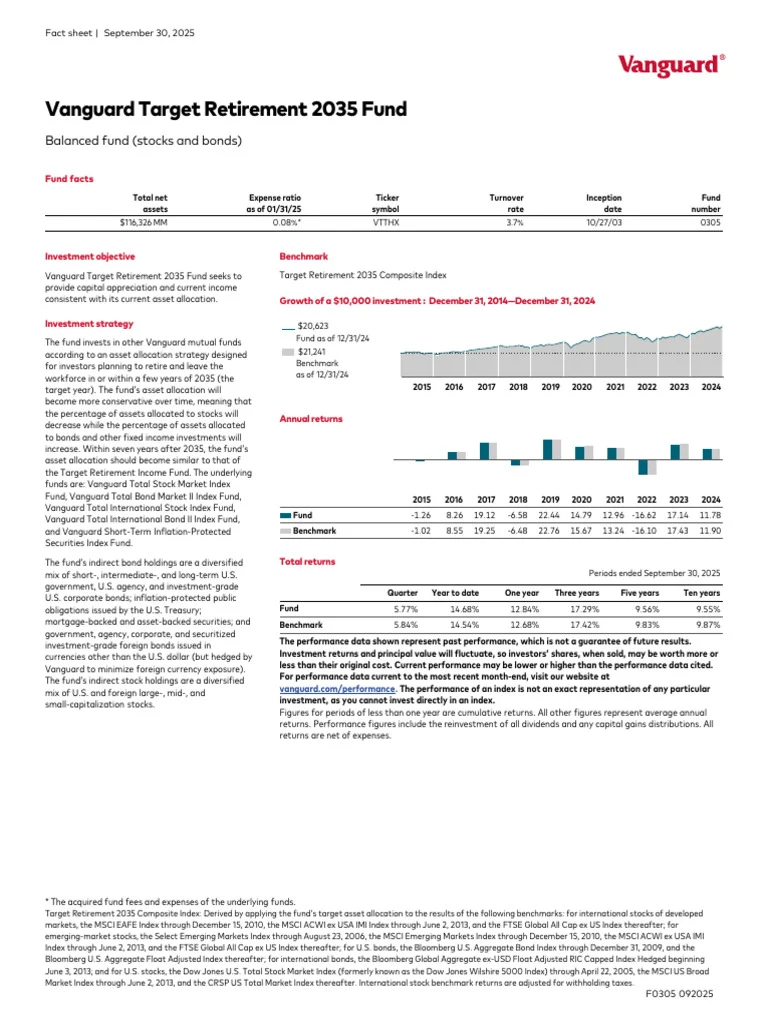

When you start planning for a retirement that’s roughly a decade away, the choices you make today can feel both exciting and overwhelming. Among the myriad of options, target‑date funds have earned a reputation for “set‑and‑forget” simplicity, especially for investors who prefer a hands‑off approach. One of the most talked‑about offerings in this space is the vanguard target retirement 2035 trust select fund.

This vehicle is designed specifically for people who envision hanging up their work shoes around the year 2035. It blends a diversified mix of stocks, bonds, and other assets, automatically shifting toward more conservative holdings as the target date approaches. In this article we’ll unpack what makes the vanguard target retirement 2035 trust select unique, explore its underlying glide‑path, discuss costs, and compare it with other popular target‑date options.

Whether you’re a young professional, a mid‑career saver, or someone nearing retirement, understanding the nuances of this fund can help you decide if it aligns with your financial goals and risk tolerance.

Understanding the Vanguard Target Retirement 2035 Trust Select

The vanguard target retirement 2035 trust select is part of Vanguard’s broader family of Target Retirement Funds. Unlike a traditional mutual fund, a “trust select” structure offers a few distinct advantages, such as potentially lower minimum investment requirements and the ability to be held within a variety of retirement accounts, including IRAs and employer‑sponsored plans.

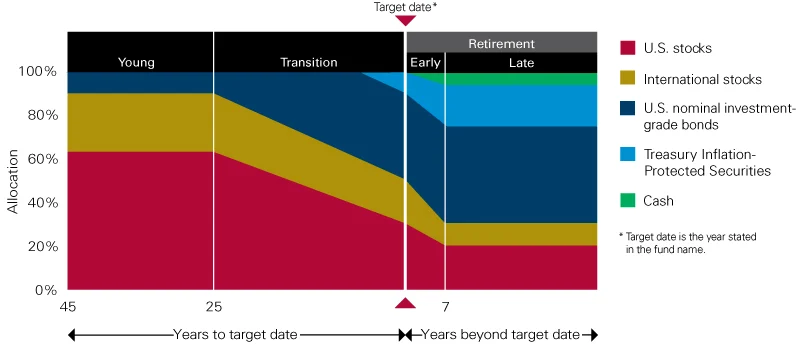

At its core, the fund follows a pre‑determined glide‑path that gradually rebalances its asset allocation. In the early years, the portfolio leans heavily toward equities to capture growth, while later years increase bond exposure to preserve capital and generate income.

Key Features of Vanguard Target Retirement 2035 Trust Select

- Broad diversification: Exposure to U.S. and international stocks, short‑term and intermediate‑term bonds, and inflation‑protected securities.

- Automatic rebalancing: The fund adjusts its mix each quarter, ensuring the glide‑path stays on track.

- Low expense ratio: Vanguard is known for cost efficiency; the 2035 trust select’s expense ratio typically sits below 0.12%.

- Tax‑efficient structure: The trust design can help reduce capital gains distributions compared with some mutual fund formats.

- Investor-friendly minimums: Many plans allow investments as low as $1,000, making it accessible to a wide audience.

How the Glide‑Path Works in Vanguard Target Retirement 2035 Trust Select

The glide‑path is the engine that drives the fund’s risk profile over time. When the fund launched, its allocation was roughly 90% equities and 10% fixed income. As we move closer to 2035, the allocation gradually shifts to about 60% equities and 40% bonds. By the time the fund reaches its “retirement” phase (typically the year after the target date), it settles into a more conservative mix—approximately 40% equities, 55% bonds, and 5% cash equivalents.

This progressive shift helps investors capture market upside during the growth years while reducing exposure to volatility as retirement approaches. The methodology mirrors Vanguard’s “LifeStrategy” philosophy but is tailored to a specific retirement horizon.

Why Choose Vanguard Target Retirement 2035 Trust Select Over Other Options?

If you’re comparing similar products, the Vanguard Target Retirement 2035 Fund VTTHX – In‑Depth Review & Guide provides a deeper dive into the underlying index holdings and performance metrics. However, the trust select version often appeals to investors who prefer a trust structure for estate planning reasons or who want to hold the fund within certain types of employer‑sponsored plans that only accept trusts.

Another frequent comparison is with the American Funds 2030 Target Date Retirement Fund. While both aim to simplify retirement investing, American Funds generally carries higher expense ratios and a more actively managed approach, whereas Vanguard’s trust select leans on passive indexing with a focus on cost savings.

Fees, Expenses, and Cost Efficiency

One of Vanguard’s hallmark strengths is its low‑cost structure. The vanguard target retirement 2035 trust select typically charges an expense ratio of 0.12%, which is well below the industry average for target‑date funds that often sit between 0.50% and 0.80%.

Low fees can have a compounding impact over the years. For example, a $10,000 investment growing at an average annual return of 6% would generate roughly $1,900 more after 15 years if the expense ratio is 0.12% versus 0.70%.

Tips for Managing Costs in Vanguard Target Retirement 2035 Trust Select

- Take advantage of any employer matching contributions to boost your overall investment without additional cost.

- Consider using a brokerage platform that offers commission‑free trades on Vanguard funds.

- Stay aware of any potential transaction fees if you move the trust select fund between accounts.

Tax Considerations and the Trust Structure

The trust select format can be advantageous from a tax perspective. Because the fund is structured as a trust, it may limit the frequency of capital gains distributions compared with a conventional mutual fund. This can be especially beneficial for investors holding the fund in taxable accounts.

However, it’s essential to note that the underlying assets—stocks and bonds—still generate dividend and interest income that is taxable in the year received. Holding the fund inside a tax‑advantaged account like a Roth IRA can shield you from those taxes entirely, allowing the compounding effect to work uninterrupted.

How to Invest in Vanguard Target Retirement 2035 Trust Select

Getting started is straightforward:

- Open an account with a brokerage that offers Vanguard funds. Many major platforms, including Vanguard’s own website, provide direct access.

- Determine your contribution amount based on your retirement goals and cash flow. Remember that many plans allow automatic contributions, making it easier to stay disciplined.

- Select the “vanguard target retirement 2035 trust select” from the fund list. Double‑check the ticker symbol (often VTTHX for the mutual fund version, but the trust may have a different identifier).

- Set up a recurring investment schedule, if possible, to benefit from dollar‑cost averaging.

For those who already have a Vanguard account, you can simply add the trust select fund to an existing portfolio. If you’re using an employer‑sponsored 401(k), verify whether the plan includes the trust version; some plans only offer the mutual fund counterpart.

Performance Review and Historical Returns

While past performance is not a guarantee of future results, it’s useful to glance at historical data. Since its inception, the vanguard target retirement 2035 trust select has delivered an average annual return of around 7% during its growth phase, aligning closely with broader market indices. In the years leading up to 2035, the fund’s return profile has become less volatile as the bond allocation increases.

Investors should compare these figures with their own risk tolerance. If you’re comfortable riding out market swings, the early‑stage high equity exposure may be appealing. Conversely, if you prefer a smoother ride, you might consider a later‑dated target fund or a more conservative allocation.

Common Questions About Vanguard Target Retirement 2035 Trust Select

Is Vanguard Target Retirement 2035 Trust Select appropriate for younger investors?

Yes, especially if you plan to retire close to 2035. The high equity portion can provide growth potential, but younger investors with a longer horizon may opt for a fund with a later target date to maintain higher growth exposure for a longer period.

Can I switch to a different target‑date fund later?

Absolutely. Vanguard allows fund exchanges without triggering a taxable event if done within a tax‑advantaged account. In a taxable account, you would need to consider capital gains implications.

What happens after 2035?

Once the fund reaches its “retirement” phase, it typically stays in a “glide‑path” that continues to become more conservative over time, focusing on income generation and capital preservation. Some investors choose to move to a separate income‑oriented fund at that point.

Comparing Vanguard Target Retirement 2035 Trust Select to Other Target‑Date Funds

When weighing options, consider the following dimensions:

- Expense Ratio: Vanguard’s 0.12% is among the lowest; many competitors charge 0.30%‑0.80%.

- Asset Allocation: Vanguard follows a passive, index‑based approach, while some rivals (e.g., American Funds) employ active management.

- Flexibility: The trust structure may be preferable for certain estate plans or for holding within specific retirement plans.

- Performance Track Record: While all target‑date funds aim for similar long‑term outcomes, Vanguard’s track record often mirrors the underlying market indices closely due to its low‑cost strategy.

Ultimately, the best choice depends on your personal circumstances, fee sensitivity, and comfort with the fund’s management style.

In summary, the vanguard target retirement 2035 trust select offers a compelling blend of low costs, automatic rebalancing, and a well‑designed glide‑path for investors targeting a 2035 retirement. Its trust structure adds an extra layer of flexibility for those navigating specific account types or estate considerations. By understanding its mechanics, fees, and tax implications, you can make an informed decision that aligns with your retirement timeline and risk appetite.