Getrawbox Getrawbox

Getrawbox Getrawbox

Related Articles

Reaching retirement often feels like stepping onto a new financial runway. You’ve paid off the mortgage, your kids may be moving out, and you’re finally looking at the freedom to enjoy the years you’ve worked so hard for. Yet, many retirees discover that cash flow can still be a tightrope walk—medical costs rise, travel dreams surface, and home maintenance never stops. One tool that’s gaining traction among seniors is the home equity line of credit, a revolving loan that taps the value you’ve built in your house without forcing you to sell.

Unlike a traditional lump‑sum home equity loan, a home equity line of credit (HELOC) works more like a credit card: you borrow, repay, and borrow again up to a preset limit. For retirees, this flexibility can mean the difference between living comfortably and constantly worrying about unexpected expenses. In this guide we’ll walk through how a home equity line of credit for retirees works, who should consider it, and what pitfalls to avoid, all while keeping the tone relaxed yet professional.

Before diving into the specifics, it’s worth noting that a HELOC isn’t a one‑size‑fits‑all solution. It’s a financial product that requires careful budgeting, an eye on interest rates, and a solid understanding of your home’s equity. If you’re ready to explore whether a home equity line of credit for retirees aligns with your retirement strategy, keep reading.

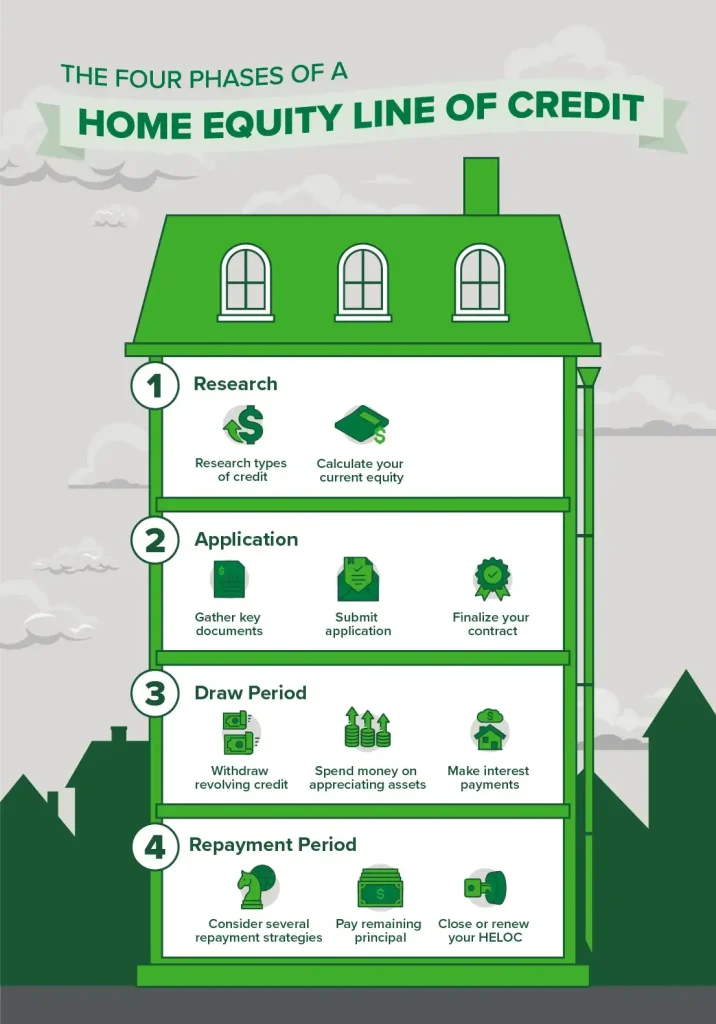

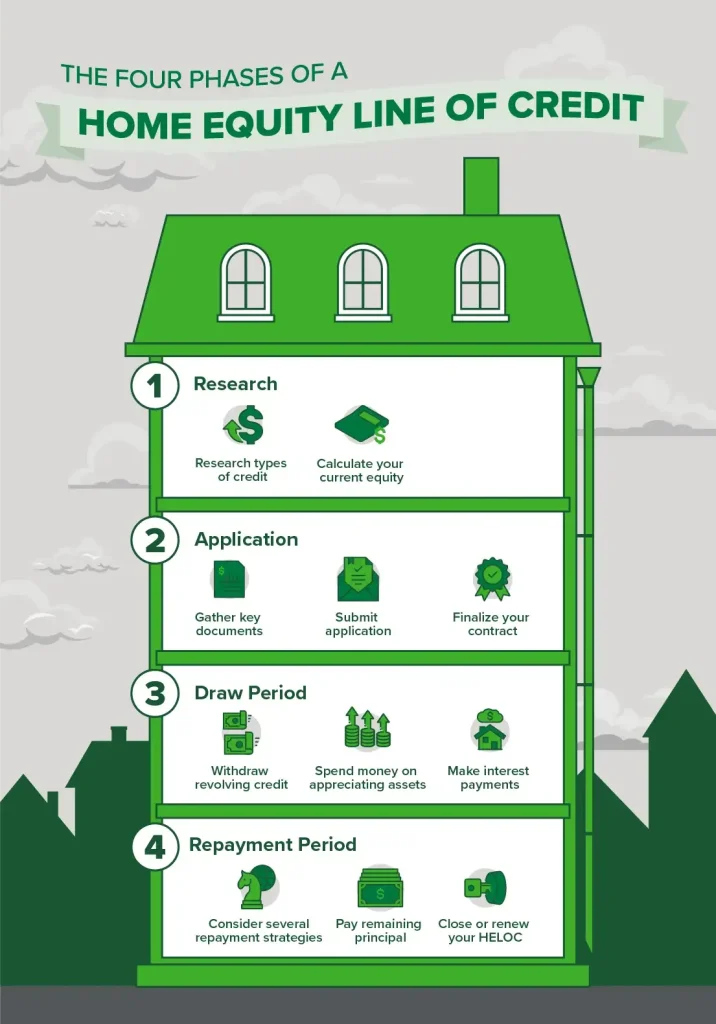

Understanding the Home Equity Line of Credit for Retirees

A home equity line of credit for retirees is essentially a loan secured by the equity you’ve accumulated in your primary residence. Equity is the market value of your home minus any outstanding mortgage balance. Lenders typically allow you to draw up to 80%‑90% of that equity, though the exact amount varies by institution and your credit profile.

What sets a retiree‑focused HELOC apart is the way lenders assess repayment ability. Since many seniors live on fixed incomes, lenders may place more emphasis on the value of the home and less on employment income. Some banks also offer “senior‑friendly” terms, such as longer draw periods or lower minimum payments.

Key Features of a Home Equity Line of Credit for Retirees

- Revolving Credit: Borrow as much as you need, repay, and borrow again within the draw period.

- Interest‑Only Payments (During Draw): Many plans let you make interest‑only payments while you’re still pulling funds.

- Variable vs. Fixed Rates: Most HELOCs start with a variable rate, but some lenders offer a fixed‑rate option for part or all of the balance.

- Tax Considerations: Interest may be deductible if the funds are used for home improvements, but not for general expenses.

- No Early Repayment Penalty: Unlike some mortgages, you can usually pay down the balance without extra fees.

How to Qualify for a Home Equity Line of Credit for Retirees

Qualification hinges on three main pillars: equity, credit score, and income stability.

- Equity Ratio: Lenders typically require you to retain at least 15%‑20% equity after the line is drawn.

- Credit Score: A score of 680 or higher is often the sweet spot, though some community banks may be more flexible.

- Income Verification: Even though you’re retired, lenders will want to see Social Security, pension, or annuity statements to confirm you can meet monthly obligations.

When a Home Equity Line of Credit for Retirees Makes Sense

Not every retiree needs a line of credit, but there are several scenarios where it shines.

Covering Unexpected Medical Expenses

Medical bills can pile up quickly, especially if you need long‑term care or home health services. A home equity line of credit for retirees can provide immediate cash without draining savings or forcing you to sell assets.

Funding Home Renovations

Making your home more accessible—adding a walk‑in bathtub, widening doorways, or installing a stairlift—can dramatically improve quality of life. Since these improvements add value to the property, the interest may even be tax‑deductible.

Supplementing Retirement Income

If your Social Security or pension falls short of covering lifestyle goals, a HELOC can act as a financial buffer. You might draw a modest amount each month, essentially turning your home’s equity into a low‑interest “salary supplement.”

Travel and Lifestyle Goals

Many retirees finally have the time to travel the world or pursue hobbies that were previously out of reach. A home equity line of credit for retirees lets you tap funds as needed, avoiding the pressure of a large lump‑sum loan.

Potential Risks and How to Mitigate Them

Every financial tool carries risk, and a HELOC is no exception. Understanding the downsides helps you make a smarter decision.

Variable Interest Rates

Most HELOCs start with a variable rate tied to the prime rate. If rates climb, your monthly payment could jump unexpectedly. To protect yourself, consider locking in a fixed portion of the balance or setting a budget that can absorb rate hikes.

Over‑Borrowing

The revolving nature can be tempting. It’s easy to dip into the line for non‑essential purchases, which can erode equity and increase debt. Create a clear plan: decide the purpose of each draw and stick to a repayment schedule.

Home as Collateral

If you default, the lender can foreclose on your house. That’s why it’s crucial to only borrow amounts you’re confident you can repay, even if your health or income situation changes.

Impact on Estate Planning

A HELOC reduces the equity that heirs will inherit. Talk to your estate planner about how a line of credit fits into your overall legacy strategy.

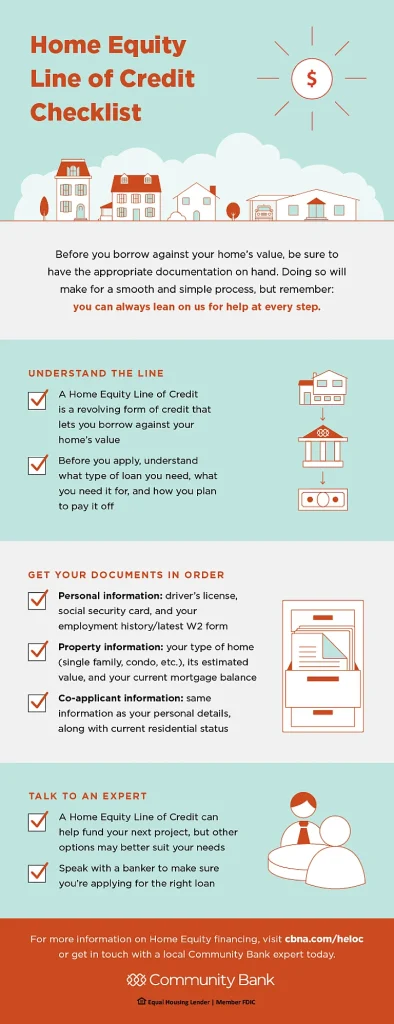

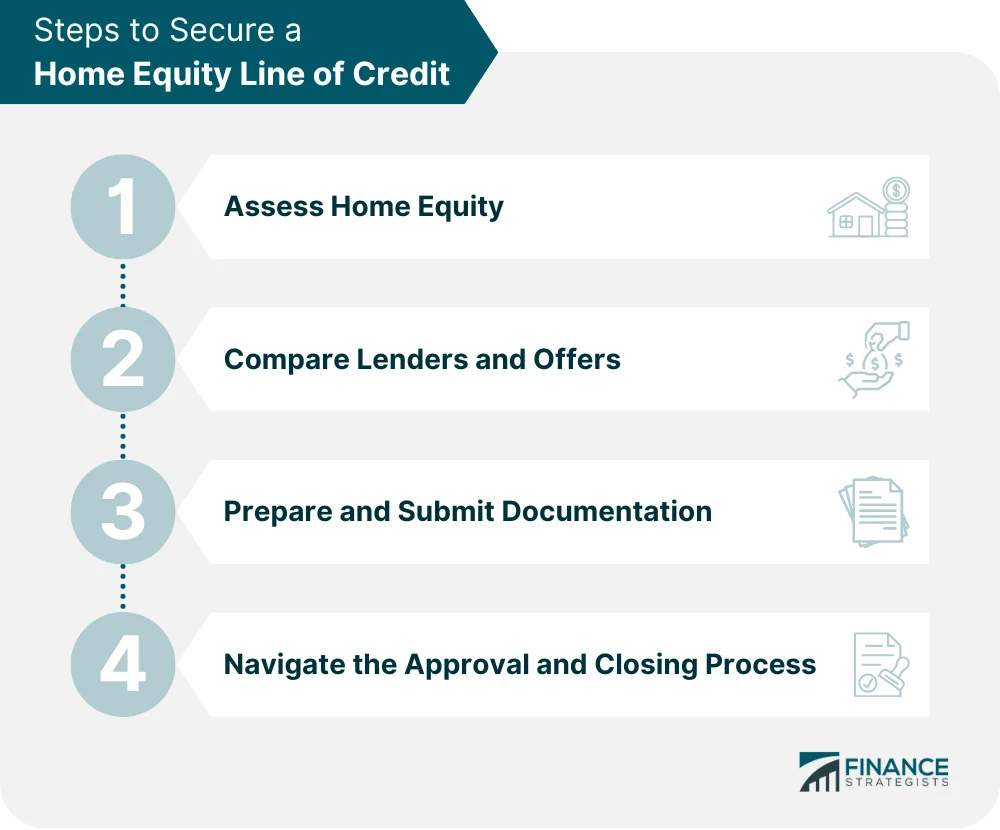

Step‑by‑Step Guide to Applying for a Home Equity Line of Credit for Retirees

Getting a HELOC doesn’t have to be a maze. Follow these steps to streamline the process.

- Assess Your Home’s Value: Use recent appraisal reports, online estimators, or a real‑estate agent’s opinion to gauge equity.

- Check Your Credit Score: Pull your free credit report and address any errors before applying.

- Gather Documentation: Prepare tax returns, proof of retirement income (Social Security statements, pension letters), and existing mortgage details.

- Shop Around: Compare rates, fees, and draw periods from multiple lenders. Some credit unions offer senior‑friendly terms.

- Submit an Application: Fill out the lender’s form, attach documentation, and be ready for a possible home appraisal.

- Review the Terms: Scrutinize the interest rate structure, repayment schedule, and any early‑termination fees.

- Close the Deal: Sign the agreement, set up online access, and start drawing when needed.

Integrating a Home Equity Line of Credit for Retirees into Your Retirement Plan

A HELOC should complement, not replace, other retirement savings. Think of it as a financial safety net that preserves your liquid assets while still giving you access to funds when you need them.

Blend with Traditional Savings

Keep an emergency fund in a high‑yield savings account for day‑to‑day expenses. Use the HELOC for larger, less frequent costs like home renovations or travel.

Coordinate with Investment Strategies

If you hold a diversified portfolio, you might draw from the HELOC to avoid selling investments during market downturns. This can help you stay on track with long‑term growth goals.

Tax Planning

Consult a tax professional to determine whether your HELOC interest qualifies for deduction. Usually, only funds used for home‑related improvements meet the IRS criteria.

Estate Considerations

Discuss the line of credit with your heirs. If you intend to leave the home untouched, you may want to plan repayment before passing the property on.

For a broader view of how a HELOC can fit into an overall retirement strategy, you might explore retirement plan options for small businesses, which often include similar principles of leveraging assets for cash flow.

Frequently Asked Questions About a Home Equity Line of Credit for Retirees

Can I Use a HELOC to Pay Off Credit Card Debt?

Yes, you can consolidate high‑interest credit card balances into a HELOC, potentially saving on interest. However, be mindful that you’re swapping unsecured debt for secured debt—your home becomes the collateral.

What Happens If I Reach the End of the Draw Period?

When the draw period ends (usually 5‑10 years), the loan shifts to repayment mode. You’ll need to start paying both principal and interest, which can increase monthly payments.

Is a Home Equity Line of Credit for Retirees Available Nationwide?

Most major banks and many regional lenders offer HELOCs, but terms vary by state. Some local credit unions tailor products specifically for seniors, so it’s worth checking community options.

Do I Need a Home Inspection?

Lenders often require a professional appraisal to verify the home’s current market value. This is separate from a routine inspection, but the cost is usually modest.

Can I Have More Than One HELOC?

Technically yes, but having multiple lines of credit on the same property can complicate repayment and affect your credit score. It’s generally advisable to keep a single, well‑managed line.

For retirees who already have investment accounts, learning how a HELOC interacts with your portfolio can be valuable. The Vanguard Target Retirement 2035 Trust Select guide, for example, discusses strategies for balancing asset growth with liquidity needs—principles that apply when you decide how much equity to tap.

In the end, a home equity line of credit for retirees can be a powerful tool when used responsibly. It offers the flexibility to handle emergencies, fund home upgrades, and even enhance your lifestyle without draining savings. The key is to treat it as a strategic component of a comprehensive retirement plan, keeping an eye on interest rates, repayment ability, and long‑term goals.

Whether you’re looking to smooth out cash flow, preserve your investment portfolio, or simply gain peace of mind, understanding the ins and outs of a home equity line of credit for retirees puts you in the driver’s seat of your golden years.