Getrawbox Getrawbox

Getrawbox Getrawbox

Related Articles

Planning for retirement can feel like navigating a maze, especially when you’re trying to pick a fund that will grow with you over the next three decades. One option that consistently pops up in the conversation is the Vanguard Target Retirement 2055 inv vffvx. Whether you’re a young professional just starting out or a seasoned investor fine‑tuning your 401(k) mix, understanding how this fund works can make a huge difference in your financial confidence.

In this article we’ll break down the essentials of the Vanguard Target Retirement 2055 inv vffvx, walk through its asset allocation, discuss the fee structure, and compare it with other target‑date options on the market. By the end, you’ll have a clear picture of whether this fund deserves a spot in your retirement toolbox.

Before diving deep, let’s quickly set the stage: target‑date funds like the Vanguard 2055 are designed to automatically shift their risk profile as you near the retirement year printed in their name—in this case, 2055. This “set‑and‑forget” approach can be a lifesaver for busy investors who prefer a hands‑off strategy while still benefiting from professional management.

vanguard target retirement 2055 inv vffvx – Core Features and How It Works

The Vanguard Target Retirement 2055 inv vffvx (ticker: VFFVX) is part of Vanguard’s well‑known suite of target‑date retirement funds. Its primary goal is to provide a diversified mix of stocks, bonds, and international assets that gradually becomes more conservative as 2055 approaches. Here’s a snapshot of the fund’s core components:

- Asset Allocation: Starts with roughly 90% equities (U.S., international, and emerging markets) and 10% fixed income. By 2055, the split shifts to about 60% equities and 40% bonds.

- Management Style: Passively managed using Vanguard’s index funds as building blocks, which helps keep expenses low.

- Expense Ratio: 0.12% – significantly lower than many actively managed alternatives.

- Rebalancing Frequency: Annual “glide‑path” adjustments plus periodic rebalancing to maintain target weights.

If you’re curious about a deeper, side‑by‑side comparison with similar funds, check out the Vanguard Target Retirement 2055 Fund (VFFVX) – In‑Depth Review & Guide. That piece walks through performance metrics, risk measures, and scenarios that help you gauge how VFFVX stacks up against its peers.

Why Choose vanguard target retirement 2055 inv vffvx Over Other Options?

There are a few compelling reasons investors gravitate toward this specific fund:

- Low Cost Structure: Vanguard’s reputation for ultra‑low fees shines here, meaning more of your money stays invested.

- Automatic Glide‑Path: The fund’s built‑in timeline reduces the need for manual rebalancing, perfect for those who prefer a “set it and forget it” mentality.

- Diversified Exposure: By blending U.S. large‑cap, small‑cap, international, and emerging‑market equities, VFFVX spreads risk across multiple economic cycles.

- Tax Efficiency: As a mutual fund, it’s structured to minimize capital gains distributions, which can be beneficial in taxable accounts.

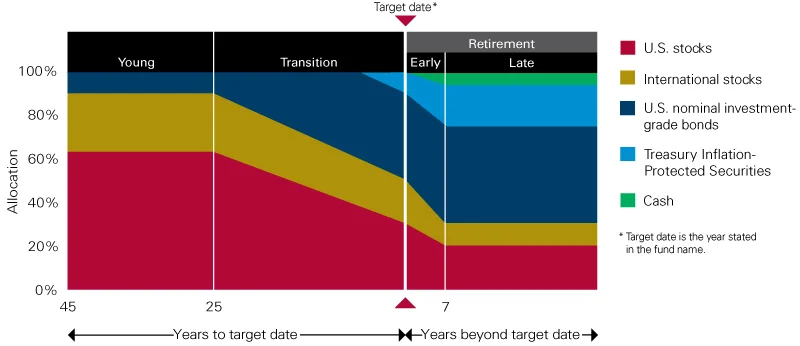

Understanding the Glide‑Path: How vanguard target retirement 2055 inv vffvx Evolves Over Time

The glide‑path is the engine that drives a target‑date fund’s risk reduction. For the Vanguard 2055, the journey looks roughly like this:

- 2024‑2030 (Early Years): 90% equities, 10% bonds – aggressive growth focus.

- 2031‑2035 (Mid‑Stage): 80% equities, 20% bonds – still growth‑oriented but with a bit more stability.

- 2036‑2040 (Pre‑Retirement): 70% equities, 30% bonds – balancing growth and preservation.

- 2041‑2055 (Retirement Horizon): 60% equities, 40% bonds – prioritizing income and lower volatility.

These percentages are not set in stone; Vanguard may tweak the glide‑path based on market conditions and evolving best practices. The key takeaway is that as you get closer to 2055, the fund leans more heavily on fixed‑income investments to cushion against market downturns.

How vanguard target retirement 2055 inv vffvx Handles Market Volatility

During periods of high volatility—think the 2008 financial crisis or the COVID‑19 market shock—target‑date funds like VFFVX benefit from their diversified nature. While equity portions may dip, the bond component provides a stabilizing effect. Moreover, the fund’s low turnover helps keep transaction costs down, allowing more of the portfolio to stay fully invested.

Fee Structure and Cost Comparison

One of the biggest advantages of the Vanguard Target Retirement 2055 inv vffvx is its expense ratio of 0.12%. To put that in perspective, here’s how it compares with a few other popular target‑date funds:

- Fidelity Freedom 2055 Fund (FFFEX): 0.29%

- T. Rowe Price Retirement 2055 Fund (TRRZX): 0.68%

- American Funds Target Date 2055 (AFITX): 0.79%

Lower fees translate directly into higher net returns over the long run, especially when compounded over three decades. If you want a deeper dive into other retirement fund options, the Retirement Plan Options for Small Businesses – A Complete Guide outlines various vehicle choices, including target‑date funds, SEP‑IRAs, and SIMPLE IRAs.

Performance Track Record

While past performance is not a guarantee of future results, it does give a useful benchmark. Over the past ten years, the Vanguard Target Retirement 2055 inv vffvx has delivered an average annual return of roughly 7.3%, closely mirroring the broader market while offering lower volatility than a pure equity index fund. During the 2020 pandemic sell‑off, VFFVX fell about 12% in Q2 but recovered to pre‑crash levels by the end of the year, illustrating its resilience.

Comparing vanguard target retirement 2055 inv vffvx to Vanguard Target Retirement 2035 Trust Select

If you’re wondering how the 2055 fund stacks up against earlier‑dated options, take a look at the Vanguard Target Retirement 2035 Trust Select – In‑Depth Look. The 2035 fund has a more aggressive equity tilt for the near term, making it suitable for investors who expect to retire earlier. Meanwhile, the 2055 fund offers a longer runway, allowing you to stay more heavily invested in equities for an extended period.

Who Should Consider vanguard target retirement 2055 inv vffvx?

The answer boils down to your retirement timeline and risk tolerance. Here are some typical investor profiles that align well with this fund:

- Young Professionals (Age 25‑35): With 20‑30 years until retirement, they can capitalize on the high equity exposure to maximize growth.

- Mid‑Career Investors (Age 36‑45): Those who still have a decade or more before 2055 can benefit from the gradual shift while maintaining a growth orientation.

- Passive Investors: Anyone who prefers a hands‑off approach, trusting Vanguard’s glide‑path to adjust risk automatically.

- Cost‑Conscious Savers: Individuals who want to keep expenses low without sacrificing diversification.

If you own a home and are exploring ways to boost retirement cash flow, you might also want to read about the Home Equity Line of Credit for Retirees – A Smart Way to Unlock Home Value. Combining a low‑cost fund like VFFVX with strategic home‑equity use can enhance your overall retirement plan.

Potential Drawbacks and Considerations

No investment is perfect. Here are a few points to keep in mind before allocating a sizable chunk of your portfolio to the Vanguard Target Retirement 2055 inv vffvx:

- One‑Size‑Fits‑All Glide‑Path: While convenient, the glide‑path may not perfectly match every investor’s risk appetite. Some may prefer a more aggressive or conservative shift.

- Limited Customization: Because the fund is a blended mix of Vanguard index funds, you can’t tweak individual holdings without moving money out of the fund.

- Tax Implications in Taxable Accounts: Though tax‑efficient, any capital gains distributions will still be taxable. Consider holding VFFVX in a tax‑advantaged account if possible.

How to Incorporate vanguard target retirement 2055 inv vffvx Into a Broader Portfolio

Think of VFFVX as the core of a “core‑satellite” strategy. Pair it with a few satellite holdings—perhaps a REIT for real‑estate exposure or a small allocation to a sector‑specific ETF—to tailor the portfolio to your unique goals. This approach lets you keep the low‑cost, diversified base while still adding personal flair.

Getting Started: Practical Steps to Invest in vanguard target retirement 2055 inv vffvx

Ready to add the Vanguard Target Retirement 2055 inv vffvx to your retirement plan? Follow these straightforward steps:

- Open an Account: If you don’t already have a Vanguard brokerage or a retirement account (IRA, 401(k) with a brokerage window), start there.

- Check Minimum Investment: Vanguard typically requires a $3,000 minimum for most target‑date mutual funds.

- Allocate Funds: Decide what portion of your portfolio will be dedicated to VFFVX. A common rule of thumb is 70‑80% of your retirement savings if you’re young.

- Set Up Automatic Contributions: Dollar‑cost averaging can smooth out market volatility over time.

- Monitor Periodically: While the fund is hands‑off, an annual review ensures it still aligns with your evolving goals.

For investors with a small business, the Retirement Plan Options for Small Businesses – A Complete Guide offers insight on how to integrate target‑date funds into employer‑sponsored plans.

Bottom Line: Is vanguard target retirement 2055 inv vffvx Right for You?

In a landscape crowded with active managers, high fees, and complex strategies, the Vanguard Target Retirement 2055 inv vffvx stands out for its simplicity, low cost, and disciplined glide‑path. If you have a long horizon, prefer a set‑and‑forget approach, and value Vanguard’s reputation for stewardship, this fund can serve as a solid foundation for your retirement savings.

Remember, the best retirement plan is one that you can stick with consistently. Whether you combine VFFVX with other assets, use a Home Equity Line of Credit to supplement income, or explore additional retirement plan options, the key is to start early, stay disciplined, and let time work its magic.