Getrawbox Getrawbox

Getrawbox Getrawbox

Related Articles

Planning for retirement can feel like navigating a maze without a map. One moment you’re saving diligently, the next you’re faced with a sea of options—annuities, Social Security, investment accounts, and more. It’s no wonder many retirees search for “the definitive guide to retirement income pdf” hoping to find a clear, downloadable blueprint. While PDFs can be handy, the real value lies in understanding the concepts they present and applying them to your unique situation.

In this article, we’ll break down the essential components of retirement income planning, walk you through the most common sources of cash flow, and show you how to stitch everything together into a cohesive strategy. Think of this as your personalized playbook—one that you can easily convert into a PDF for future reference, but also a living document you’ll revisit as life unfolds.

Whether you’re approaching the finish line of your career or you’re a few decades away, the principles covered here remain timeless. And, because no guide stands alone, we’ll sprinkle in a few handy internal resources that dive deeper into specific topics like target‑date funds and IRA setups.

the definitive guide to retirement income pdf: Foundations of a Secure Cash Flow

Before you hit “download” on any PDF, ask yourself what you truly need from a retirement income plan. The core goal is simple: generate enough reliable cash flow to cover your lifestyle while preserving capital for unexpected expenses. This involves three pillars—Earned Income Replacement, Investment Income, and Safety Nets—each of which we’ll unpack below.

the definitive guide to retirement income pdf – Mapping Your Income Sources

Start by listing every potential stream of money you expect to receive after you stop working full‑time. Common sources include:

- Social Security benefits

- Pension payments (if you have a defined benefit plan)

- Required Minimum Distributions (RMDs) from traditional IRAs and 401(k)s

- Dividend and interest income from taxable accounts

- Annuity payouts

- Part‑time work or consulting gigs

- Home equity (via a reverse mortgage or HELOC)

When you have this inventory, you can start matching each source to the type of expense it’s best suited for—fixed versus variable, short‑term versus long‑term. This step is the backbone of any “definitive guide to retirement income PDF” you might eventually create.

Building a Multi‑Layered Income Strategy

Relying on a single source of retirement cash is risky. A diversified income plan reduces the impact of market volatility, policy changes, or health emergencies. Below are the layers you should consider.

1. Safety‑First Layer: Guaranteed Income

Guaranteed income is the cornerstone for most retirees because it provides peace of mind. Options include:

- Social Security – Typically the largest single source for many Americans. Timing your claim (age 62 vs. 70) can dramatically affect monthly benefits.

- Pension plans – If you’re lucky enough to have a defined benefit plan, treat it as a “salary” you can count on.

- Immediate or deferred annuities – Convert a lump sum into a predictable stream. Be mindful of fees and inflation riders.

When drafting your PDF guide, illustrate these guarantees with a simple table that shows projected monthly income at different ages. This visual aid helps you see where gaps may exist.

2. Growth‑Oriented Layer: Investment Income

Even in retirement, a portion of your portfolio should stay invested for growth and inflation protection. Consider the following vehicles:

- Dividend‑yielding equities (e.g., high‑quality blue‑chip stocks)

- Bond ladders that provide staggered maturities and regular interest payments

- Target‑date funds that automatically reallocate assets as you age. For an in‑depth look, read our t rowe price retirement 2050 fund: A Comprehensive Guide article.

These investments can be taxed differently, so factor in tax efficiency when you build the cash‑flow model for your PDF.

3. Flexibility Layer: Contingency & Lifestyle Income

Life rarely follows a straight line. Health costs, travel dreams, or helping family members may require extra cash. Flexible sources include:

- Roth IRA withdrawals (tax‑free if qualified)

- Home equity lines of credit (HELOC) – a smart way to tap home value without selling. Learn more in our Home Equity Line of Credit for Retirees – A Smart Way to Unlock Home Value guide.

- Part‑time consulting or gig work that leverages your career expertise.

These layers act like a financial safety net, allowing you to adapt without jeopardizing core income.

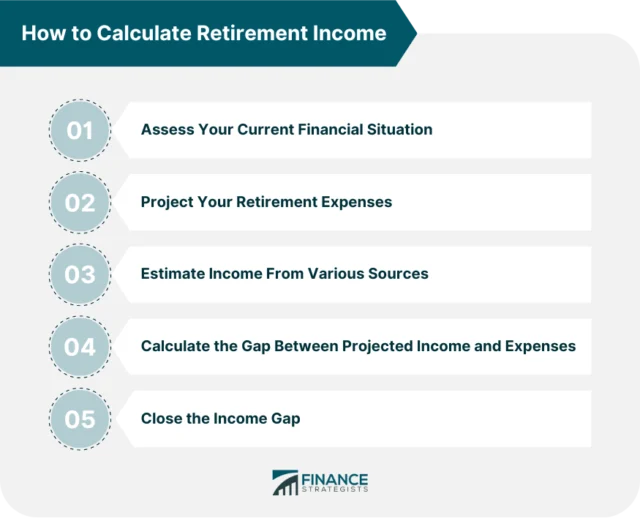

Calculating Your Retirement Income Needs

Now that you have a structure, it’s time to put numbers to the plan. Most financial planners recommend using the 4% rule as a starting point—withdraw 4% of your pre‑retirement portfolio each year, adjusted for inflation. However, the rule is a simplification; a personalized approach yields better results.

Step‑by‑Step Calculator

- Estimate annual expenses – Include housing, healthcare, food, travel, and a buffer for emergencies.

- Subtract guaranteed income – Total Social Security, pensions, and annuities.

- Determine the shortfall – This is the amount you need from investments and other sources.

- Run withdrawal scenarios – Use different asset allocations (e.g., 60/40 stocks/bonds) and see how long the portfolio lasts under various market returns.

Document each step in your PDF so you can revisit and adjust as circumstances evolve. A spreadsheet linked to the PDF works wonders for ongoing tracking.

Tax‑Efficient Withdrawal Strategies

Taxes can eat a sizable chunk of your retirement income if you’re not careful. The order in which you tap accounts matters. A common hierarchy looks like this:

- Withdraw from taxable accounts first (to take advantage of lower capital gains rates).

- Next, draw from tax‑deferred accounts (traditional IRAs, 401(k)s) up to the age‑59½ mark to avoid penalties.

- Finally, use tax‑free accounts (Roth IRAs, Roth 401(k)s) for any remaining needs.

By following this sequence, you often minimize overall tax liability while preserving the tax‑advantaged growth potential of Roth accounts for later years.

Special Consideration: Required Minimum Distributions (RMDs)

Starting at age 73 (as of 2024), the IRS mandates RMDs from most traditional retirement accounts. Failure to take the required amount triggers a 25% penalty (up to 50% if the error isn’t corrected). Incorporate RMD calculations into your PDF so you never miss a deadline.

Protecting Your Income Against Risks

Even the best‑crafted plan can be derailed by unexpected events. Here’s how to safeguard your cash flow.

1. Longevity Risk

Outliving your savings is a real concern. Solutions include:

- Purchasing a longevity annuity that kicks in at age 80 or 85.

- Maintaining a modest, growth‑oriented portfolio to keep pace with inflation.

2. Market Volatility

A well‑balanced asset allocation reduces the impact of market swings. Consider a “bucket strategy”:

- Bucket 1 – Cash and short‑term bonds for the next 1‑3 years.

- Bucket 2 – Intermediate‑term bonds and dividend stocks for years 4‑10.

- Bucket 3 – Growth‑oriented equities for beyond 10 years.

3. Healthcare Costs

Healthcare expenses tend to rise faster than inflation. Options to manage them include:

- Medicare Supplement (Medigap) policies.

- Health Savings Accounts (HSAs) if you’re still eligible.

- Long‑term care insurance—evaluate whether the premium fits your budget.

Creating Your Own “Definitive Guide to Retirement Income PDF”

Now that you’ve gathered the data, the final step is packaging it into a clear, downloadable PDF. Here’s a quick workflow:

- Write the content in a word processor using headings that mirror the structure above.

- Insert tables, charts, and the bucket‑strategy diagram to visualize cash flow.

- Export to PDF and add bookmarks for easy navigation.

- Store the PDF in a cloud folder (Google Drive, Dropbox) and share it with your financial advisor.

If you need guidance on setting up retirement accounts that will feed into your PDF, check out our How s set up an individual retirement account – A Complete Guide article for step‑by‑step instructions.

Tools and Resources to Streamline the Process

Technology can make retirement planning less daunting. Below are a few tools you might find useful:

- Retirement calculators – Many brokerage sites (Vanguard, Fidelity) offer free calculators that project income based on different withdrawal rates.

- Financial planning software – Tools like Personal Capital or Mint can aggregate all accounts in one view.

- PDF editors – Adobe Acrobat or free alternatives (PDFescape) let you annotate and update your guide without starting from scratch.

Combining these tools with the framework we’ve outlined turns a vague idea into a concrete, actionable plan.

Remember, the “definitive guide to retirement income pdf” isn’t a static document you file away and forget. Treat it as a living roadmap—review it annually, adjust for market changes, and refine your assumptions about lifespan and expenses. By staying engaged, you’ll enjoy the confidence that comes from knowing exactly how you’ll fund the life you’ve imagined.

Happy planning, and may your retirement years be as rewarding as the hard work that got you there.

[Finance]: Finance