Getrawbox Getrawbox

Getrawbox Getrawbox

Related Articles

When you start thinking about life after work, the first thing that pops into most people’s minds is Social Security. It’s the backbone of retirement income for millions, but it’s rarely a stand‑alone solution. Understanding the nuances of social security potential private retirement benefit information can unlock a more secure, flexible financial future.

In this article we’ll walk through how Social Security interacts with private retirement accounts, what the “potential” really means, and practical steps you can take today. Whether you’re a fresh graduate, a mid‑career professional, or nearing retirement, the insights here will help you stitch together a retirement plan that feels both comfortable and realistic.

social security potential private retirement benefit information: The Big Picture

At its core, Social Security provides a baseline income that replaces a portion of your pre‑retirement earnings. However, the amount you receive is heavily influenced by factors like your lifetime earnings, the age you start collecting, and whether you have other sources of income. That’s where private retirement benefits—401(k)s, IRAs, pensions, and even annuities—come into play. By layering these options, you can often boost the “potential” of your Social Security benefits, turning a modest safety net into a robust income stream.

One common misconception is that Social Security benefits get reduced if you have a private pension. In reality, the two are largely independent, though high private incomes can affect the taxation of your Social Security checks. Knowing these interactions is essential for accurate social security potential private retirement benefit information.

social security potential private retirement benefit information: How Earnings Affect Your Benefit

The Social Security Administration (SSA) calculates your benefit based on your 35 highest‑earning years. If you’ve spent some of those years with lower earnings—perhaps due to a career break, part‑time work, or early retirement—your benefit could be lower than it might be. Private retirement plans can help offset this gap:

- Catch‑up contributions: If you’re 50 or older, you can contribute extra dollars to 401(k) or IRA accounts, increasing the pool of savings that can supplement a modest Social Security check.

- Employer‑sponsored pensions: For those who work for companies offering defined benefit plans, the pension can serve as a “fill‑in” for years where Social Security payouts are lower.

- Investment growth: Private accounts typically offer higher growth potential than Social Security, which is adjusted only for inflation.

By aligning your private retirement savings with the timeline of your Social Security eligibility, you can maximize the overall benefit you receive each month.

Key Strategies to Enhance Your Retirement Income

Now that we’ve covered the basic mechanics, let’s dig into actionable strategies that can elevate your social security potential private retirement benefit information to the next level.

Delay Claiming to Increase Monthly Checks

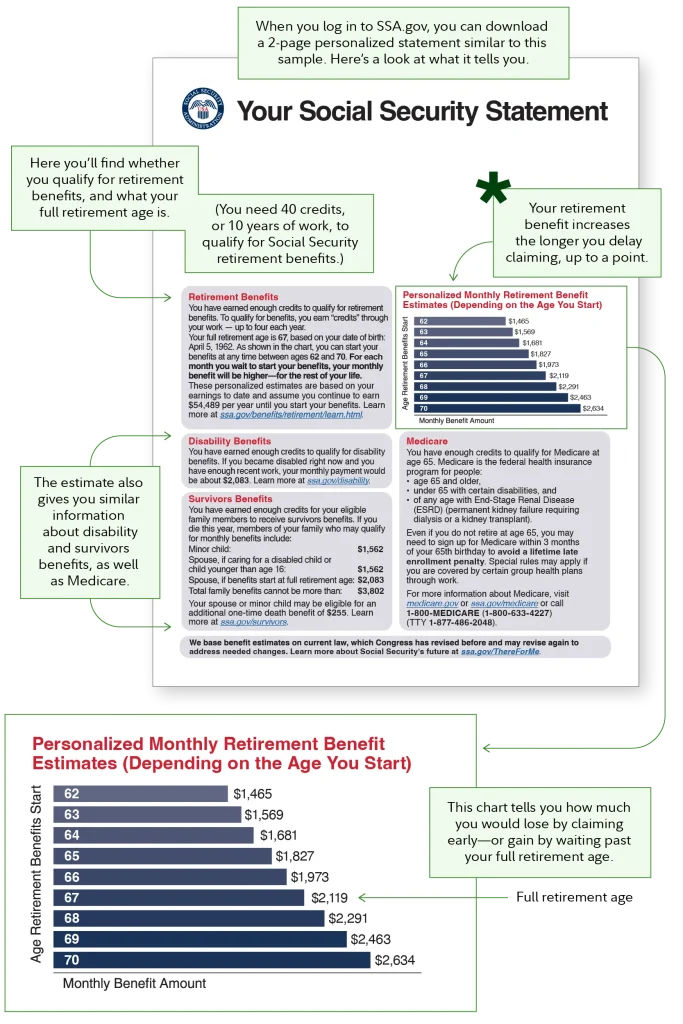

For many, the easiest way to boost Social Security is simply to wait. If you’re eligible at 62 but can afford to postpone, each year you delay past your full retirement age (FRA) adds roughly 8% to your benefit until you hit age 70. This “delayed retirement credit” can dramatically improve the total income you receive, especially when combined with private investments that can bridge the gap in the interim.

Coordinate Spousal Benefits

If you’re married, consider how spousal benefits can complement your own. A lower‑earning spouse can claim a benefit based on the higher earner’s record, up to 50% of the higher earner’s full benefit. This strategy can free up private retirement savings for the higher earner, allowing for targeted growth and tax planning.

Utilize Roth Conversions Wisely

Roth IRA conversions can be a tax‑efficient way to manage income in retirement. Since qualified Roth withdrawals are tax‑free, you can keep your taxable income low, potentially reducing the amount of Social Security benefits that become taxable. This synergy is a prime example of leveraging social security potential private retirement benefit information to keep more money in your pocket.

Take Advantage of Employer Match Programs

Many employers offer matching contributions on 401(k) plans. If you’re not maxing out this match, you’re essentially leaving free money on the table—money that could later supplement a modest Social Security payout. Even a modest match can compound over time and make a noticeable difference in retirement.

Understanding the Interaction with Taxes

While Social Security benefits are often seen as tax‑free, that’s not always the case. If your combined income (including half of your Social Security benefits) exceeds certain thresholds, a portion of those benefits becomes taxable. This is where private retirement planning can play a crucial role.

For example, withdrawing from a traditional IRA adds to your taxable income, possibly pushing more of your Social Security into the taxable range. Conversely, a Roth IRA withdrawal does not increase taxable income, preserving more of your Social Security benefit. Balancing these withdrawals is an art—one that directly impacts your social security potential private retirement benefit information outlook.

Practical Tax Planning Tips

- Monitor your provisional income (adjusted gross income + nontaxable interest + half of Social Security) each year.

- Consider a “tax‑efficient withdrawal ladder” that pulls from Roth accounts first, preserving traditional accounts for later years when thresholds might be higher.

- Explore qualified charitable distributions (QCDs) from IRAs after age 70½ to reduce taxable income without increasing your required minimum distributions (RMDs).

Tools and Resources to Simplify Your Planning

There’s a wealth of calculators and guides out there, but picking the right one can be overwhelming. Here are a few that align well with the concept of social security potential private retirement benefit information:

- Social Security Retirement Estimator – Gives you a personalized projection based on your actual earnings record.

- My Retirement Plan Calculators – Offers a suite of tools for evaluating 401(k), IRA, and pension scenarios.

- FINRA Retirement Resources – Provides educational articles on tax strategies and withdrawal sequencing.

If you’re a public employee, you might want to check out the Teacher Retirement System of New York – A Complete Guide for state‑specific nuances that can affect your overall retirement picture.

Case Study: Small Business Owner

Small business owners often face unique challenges when it comes to retirement planning. The Understanding Retirement Accounts for Small Business Owners guide breaks down options like SEP‑IRAs, SIMPLE 401(k)s, and solo 401(k)s. By leveraging these vehicles, a business owner can create a private retirement nest egg that complements Social Security, effectively raising the “potential” of their overall retirement income.

Common Pitfalls to Avoid

Even with the best intentions, many retirees stumble over avoidable mistakes that diminish their social security potential private retirement benefit information. Here are a few to watch out for:

- Claiming Too Early: While the allure of immediate cash is strong, the long‑term loss in monthly benefits can outweigh short‑term needs.

- Ignoring Spousal Benefits: Failing to coordinate spousal benefits can leave money on the table, especially for couples where one partner earned significantly less.

- Underestimating Healthcare Costs: Health expenses can erode retirement savings quickly. Planning for Medicare premiums and supplemental insurance is essential.

- Not Adjusting for Inflation: Social Security does adjust for inflation, but private accounts need active management to keep pace.

Strategic Review Checklist

- Reassess your Social Security claiming age each year.

- Review your private retirement account balances and contribution levels.

- Run a tax projection to see how much of your Social Security will be taxable.

- Update your beneficiary designations on all accounts.

- Consider consulting a fiduciary financial planner for a holistic review.

By staying proactive and regularly revisiting your plan, you can keep your social security potential private retirement benefit information aligned with your evolving goals and market conditions.

In the end, the secret to a comfortable retirement isn’t just about maximizing one piece of the puzzle; it’s about weaving together Social Security, private savings, tax strategies, and personal circumstances into a cohesive, adaptable plan. The more you understand how each component interacts, the better you can shape a retirement that feels both secure and rewarding.