Table of Contents

- How to Open Roth IRA Bank of America: Step‑by‑Step Overview

- Step 1: Verify Eligibility to Open Roth IRA Bank of America

- Step 2: Gather Required Documentation to Open Roth IRA Bank of America

- Step 3: Choose Your Investment Mix While You Open Roth IRA Bank of America

- Step 4: Complete the Online Application to Open Roth IRA Bank of America

- Step 5: Set Up Automatic Contributions and Review Annually

- Benefits of Choosing Bank of America for Your Roth IRA

- Integrated Banking Experience When You Open Roth IRA Bank of America

- Robust Research and Educational Tools

- Competitive Fee Structure (If You Meet Certain Criteria)

- Strong Customer Support and In‑Person Assistance

- Potential Drawbacks and How to Mitigate Them

- Limited Low‑Cost Index Fund Selection

- Higher Minimums for Certain Investments

- Potential for Over‑Diversification

- Tax Implications and Withdrawal Rules for Your Roth IRA

- Frequently Asked Questions About Opening a Roth IRA at Bank of America

- Can I Transfer an Existing Roth IRA to Bank of America?

- Do I Need to Be a Bank of America Customer to Open a Roth IRA?

- What Happens If I Exceed the Contribution Limit?

- How Does the “Preferred Banking” Status Affect My Roth IRA?

- Is There a Minimum Age to Open Roth IRA Bank of America?

- Real‑World Example: How a Young Professional Can Leverage a Roth IRA at Bank of America

- Comparing Bank of America’s Roth IRA to Other Popular Providers

- Steps to Take After You Open Roth IRA Bank of America

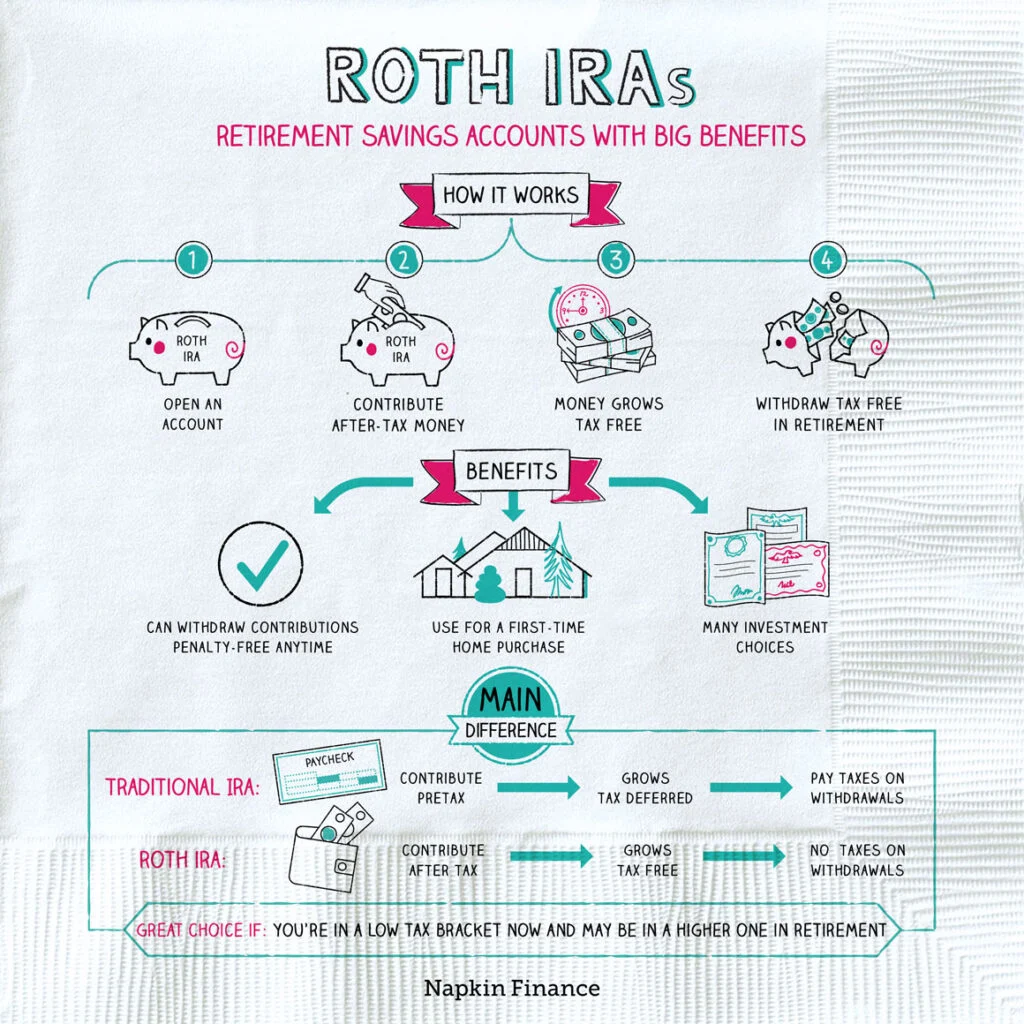

Thinking about bolstering your retirement nest egg while keeping taxes at bay? A Roth IRA is often the go‑to vehicle for many savers, and doing it through a big, familiar institution can add a layer of comfort. Bank of America, one of the nation’s largest banks, offers a Roth IRA that blends the convenience of a full‑service bank with the tax advantages of a Roth account. Whether you’re a seasoned investor or just getting started, understanding how to open Roth IRA Bank of America can set you on the right path.

In this article we’ll break down the basics—who can contribute, what the fee structure looks like, and why you might prefer Bank of America over a pure‑play brokerage. We’ll also walk through the actual enrollment process, highlight common pitfalls, and give you a handful of practical tips to make the most of your new retirement account. By the end, you should feel confident enough to click that “Apply” button and start funding your future.

Ready to dive in? Let’s explore the key reasons why a Roth IRA at Bank of America might be a smart move and how you can get it up and running without a hitch.

How to Open Roth IRA Bank of America: Step‑by‑Step Overview

Opening a Roth IRA with Bank of America isn’t rocket science, but it does involve a few decisions that can affect your long‑term results. Below is a concise roadmap that walks you through the entire journey—from checking eligibility to making your first contribution.

Step 1: Verify Eligibility to Open Roth IRA Bank of America

- Income Limits: Your Modified Adjusted Gross Income (MAGI) must fall below the IRS thresholds for the year you contribute. For 2024, the phase‑out range for single filers is $138,000–$153,000, and $218,000–$228,000 for married couples filing jointly.

- Contribution Limits: You can contribute up to $6,500 per year (or $7,500 if you’re 50 or older) across all Roth IRAs you own.

- Earned Income: You need wages, salary, or self‑employment earnings to qualify.

If you meet these criteria, you’re good to go. If you’re not sure where you stand, Bank of America’s online portal includes a quick eligibility calculator to save you time.

Step 2: Gather Required Documentation to Open Roth IRA Bank of America

Before you start the application, have these items handy:

- Social Security Number (or Taxpayer Identification Number)

- Driver’s license or state ID for identity verification

- Bank account information for funding the Roth IRA (checking or savings account)

- Employer information for employment verification

Having everything ready will keep the process smooth and prevent any annoying back‑and‑forth with the compliance team.

Step 3: Choose Your Investment Mix While You Open Roth IRA Bank of America

Bank of America offers a variety of investment options inside a Roth IRA, ranging from low‑cost index funds to actively managed mutual funds and even individual stocks through its Merrill Edge platform. Think about your risk tolerance and time horizon before locking in a portfolio:

- Conservative: High‑yield savings, short‑term bond funds

- Balanced: A blend of U.S. large‑cap equity and intermediate‑term bond funds

- Aggressive: International stocks, sector‑specific ETFs, or individual equities

For a deeper dive on selecting the right mix, check out the Open a Roth IRA with Bank of America – Step‑by‑Step Guide article, which walks through each fund category in detail.

Step 4: Complete the Online Application to Open Roth IRA Bank of America

Head to Bank of America’s “Investing” section on their website and click “Open a Roth IRA.” The form will ask for:

- Personal details (name, address, contact info)

- Tax information (filing status, dependents)

- Beneficiary designation (who inherits the account)

- Funding method (link a checking account or initiate a transfer from another IRA)

Review the disclosures, confirm you understand the fee schedule, and submit. In most cases, the account is live within 24–48 hours, and you can start investing right away.

Step 5: Set Up Automatic Contributions and Review Annually

One of the biggest advantages of a Roth IRA is the ability to automate contributions, ensuring you never miss a tax‑advantaged saving opportunity. Bank of America lets you schedule monthly transfers from a linked checking account, which you can adjust anytime.

Remember to revisit your asset allocation at least once a year or after any major life event (marriage, new job, etc.). This habit helps keep your retirement plan aligned with your evolving goals.

Benefits of Choosing Bank of America for Your Roth IRA

Bank of America isn’t the only institution offering a Roth IRA, but it brings a few distinctive perks that can tip the scales in its favor.

Integrated Banking Experience When You Open Roth IRA Bank of America

Because Bank of America combines traditional banking with investment services, you get a unified dashboard to track both your everyday accounts and retirement savings. No need to juggle multiple logins or reconcile statements across different platforms.

Robust Research and Educational Tools

The bank’s Merrill Edge research suite provides market commentary, fund ratings, and portfolio analysis tools—all at no extra cost for account holders. Whether you’re a beginner or an advanced trader, these resources can sharpen your decision‑making.

Competitive Fee Structure (If You Meet Certain Criteria)

Bank of America waives most account‑maintenance fees if you maintain a minimum balance of $15,000 across your retirement accounts or if you’re a Preferred Banking client. Otherwise, the annual fee is modest ($25‑$35), which is comparable to many discount brokers.

Strong Customer Support and In‑Person Assistance

Unlike some online‑only brokers, Bank of America offers branch‑based assistance. If you prefer speaking with a financial adviser face‑to‑face, you can schedule an appointment at any of the bank’s thousands of locations.

Potential Drawbacks and How to Mitigate Them

No financial product is perfect, and a Roth IRA at Bank of America has a few quirks worth noting.

Limited Low‑Cost Index Fund Selection

While the bank offers a solid lineup of mutual funds, its expense ratios can be higher than those found at pure‑play brokers like Vanguard or Fidelity. To keep costs low, consider allocating a portion of your Roth IRA to the bank’s no‑transaction‑fee ETFs, which often have competitive expense ratios.

Higher Minimums for Certain Investments

Some mutual funds require a $2,500 minimum investment, which might be a barrier if you’re just starting out. In those cases, you can begin with a money‑market fund or a low‑minimum ETF and gradually shift into higher‑minimum offerings as your balance grows.

Potential for Over‑Diversification

Because Bank of America bundles many investment options under its umbrella, it’s easy to spread your money across too many products, diluting returns. Stick to a core‑plus strategy: a solid core (e.g., a total‑market index fund) and a few satellite positions for growth or sector exposure.

Tax Implications and Withdrawal Rules for Your Roth IRA

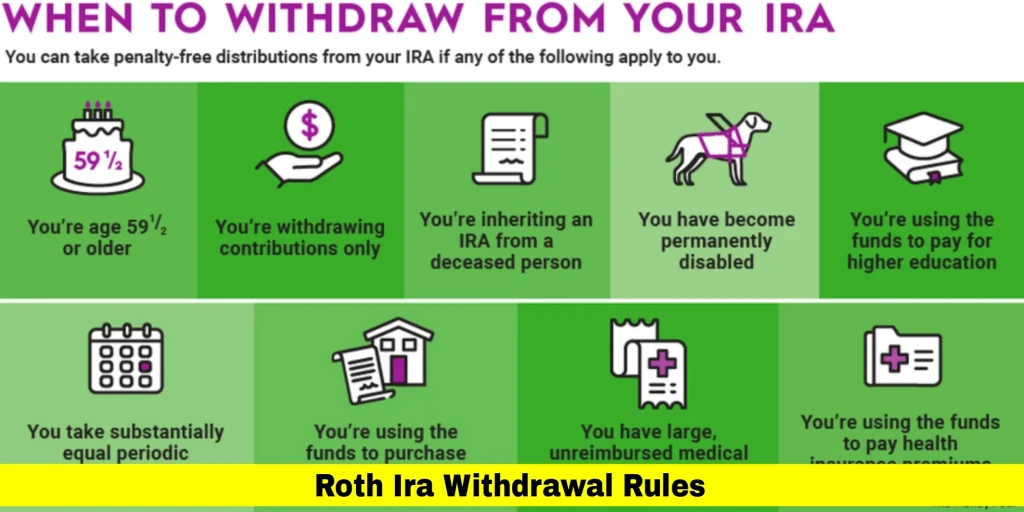

One of the biggest attractions of a Roth IRA is the tax‑free growth and qualified withdrawals. Here’s a quick refresher on the rules that apply once you open Roth IRA Bank of America:

- Qualified Distributions: Tax‑free if you’re at least 59½ and the account has been open for five years.

- Non‑Qualified Distributions: Earnings may be subject to income tax and a 10% penalty, though contributions can be withdrawn anytime tax‑ and penalty‑free.

- Required Minimum Distributions (RMDs): Unlike traditional IRAs, Roth IRAs have no RMDs during the owner’s lifetime.

- Beneficiary Rules: Heirs inherit the account and can stretch tax‑free growth over their lifetimes, provided the five‑year rule is satisfied.

Understanding these nuances helps you avoid costly mistakes down the road and maximizes the tax‑advantaged benefits of your Roth IRA.

Frequently Asked Questions About Opening a Roth IRA at Bank of America

Can I Transfer an Existing Roth IRA to Bank of America?

Absolutely. You can initiate a direct trustee‑to‑trustee transfer, which avoids any tax consequences. Bank of America’s custodian team will walk you through the paperwork, and the process typically takes 2‑3 weeks.

Do I Need to Be a Bank of America Customer to Open a Roth IRA?

No. While having an existing checking or savings account can simplify funding, non‑customers can still open a Roth IRA. You’ll just need to provide an external bank account for initial contributions.

What Happens If I Exceed the Contribution Limit?

Excess contributions are subject to a 6% excise tax each year until corrected. You can either withdraw the excess (plus earnings) before the tax deadline or recharacterize it to a traditional IRA.

How Does the “Preferred Banking” Status Affect My Roth IRA?

Preferred Banking clients (those who maintain $75,000+ in combined accounts) enjoy fee waivers, higher interest on cash balances, and access to dedicated financial advisers—making the overall Roth IRA experience smoother and more cost‑effective.

Is There a Minimum Age to Open Roth IRA Bank of America?

Yes. You must have earned income, which generally means you’re at least 18 and working. However, minors can have a custodial Roth IRA set up by a parent or guardian.

Real‑World Example: How a Young Professional Can Leverage a Roth IRA at Bank of America

Imagine Maya, a 28‑year‑old software engineer earning $85,000 a year. She decides to open Roth IRA Bank of America and contributes $500 each month. Assuming a 7% average annual return, after 30 years she could accumulate roughly $500,000, all tax‑free. By automating her contributions and selecting a low‑cost total‑market index fund within the bank’s platform, she keeps fees under 0.25% and maximizes compounding. This scenario underscores how consistent saving, even at modest levels, can produce a substantial nest egg.

Comparing Bank of America’s Roth IRA to Other Popular Providers

If you’re still on the fence, it helps to benchmark Bank of America against a few competitors:

| Feature | Bank of America | Vanguard | Fidelity |

|---|---|---|---|

| Account Minimum | $0 (but $2,500 for many funds) | $0 for ETFs, $3,000 for most mutual funds | $0 (some funds $0, others $2,500) |

| Expense Ratios | 0.10%‑0.50% (varies) | 0.03%‑0.10% (industry‑low) | 0.04%‑0.35% |

| Fee Waiver | Yes, with $15k balance or Preferred Banking | N/A | None |

| Branch Support | Nationwide | Online only | Online only (some physical locations) |

While Vanguard leads on ultra‑low costs, Bank of America shines in integrated banking services and in‑person help. Your choice should reflect what matters most: cost, convenience, or personal service.

Steps to Take After You Open Roth IRA Bank of America

Getting the account set up is only the beginning. Here’s a concise checklist to keep you on track:

- Set a Contribution Schedule: Automate monthly deposits to hit the annual limit.

- Choose a Core Holding: Typically a total‑market index fund for broad diversification.

- Allocate Satellite Positions: Add sector or international exposure if you’re comfortable with added risk.

- Review Beneficiaries: Keep them up‑to‑date after major life events.

- Monitor Fees: If fees creep above 0.30%, consider moving to a lower‑cost alternative.

Following these steps ensures your Roth IRA remains a high‑performing, tax‑efficient cornerstone of your retirement plan.

As you can see, the process of open Roth IRA Bank of America is straightforward, especially when you leverage the bank’s online tools and branch resources. The combination of tax‑free growth, flexible investment options, and a robust support network makes it a compelling choice for many savers. Whether you’re just starting your career or looking to consolidate existing retirement assets, a Roth IRA at Bank of America can provide the structure and convenience you need to stay on track.

For more context on Bank of America’s retirement offerings, you might also want to read the related piece Does Bank of America Have Roth IRA? A Complete Guide, which delves into additional account features and compares them side‑by‑side with other major banks.

Now that you’ve got the full picture—from eligibility checks to post‑opening maintenance—there’s little reason to wait. Open that Roth IRA, start feeding it regularly, and let compound interest work its magic. Your future self will thank you.