Getrawbox Getrawbox

Getrawbox Getrawbox

Related Articles

When you’ve spent a career serving the federal government, the thought of tapping into that hard‑earned retirement money can feel both tempting and confusing. Maybe you’re facing an unexpected medical bill, a home repair, or simply want a short‑term cash boost while you transition to civilian life. The natural question that pops up is: can i borrow from my fers retirement? In this article we’ll walk through the mechanics, the legal limits, and the practical considerations so you can make an informed decision without jeopardizing your future security.

First, let’s clear up a common misconception. Unlike a 401(k) or a traditional IRA, the Federal Employees Retirement System (FERS) does not provide a built‑in loan feature. That doesn’t mean you’re completely out of options, but it does mean you’ll need to look at external avenues and understand the impact on your pension and tax situation. We’ll break down those alternatives, compare them to a hypothetical “FERS loan,” and give you actionable tips for managing cash flow in retirement.

Can I Borrow From My FERS Retirement? Understanding the Basics

The short answer is no—FERS itself does not allow you to take a direct loan against your pension or the Thrift Savings Plan (TSP) that’s bundled with it. However, the broader picture includes a few pathways that can feel like borrowing:

- Take a distribution early—you can withdraw money from your TSP before age 59½, but you’ll face ordinary income tax and possibly a 10% early‑withdrawal penalty.

- Roll over to an IRA—once you’ve separated from service, you can roll your TSP into a traditional IRA, which may offer loan provisions (some IRA custodians allow a 5‑year, 10% loan limit).

- Use a home equity line of credit (HELOC)—if you own property, a HELOC can give you access to cash using the equity you’ve built, effectively borrowing against a different asset.

Each of these options has pros and cons, and the decision often hinges on your immediate need, tax implications, and long‑term retirement goals.

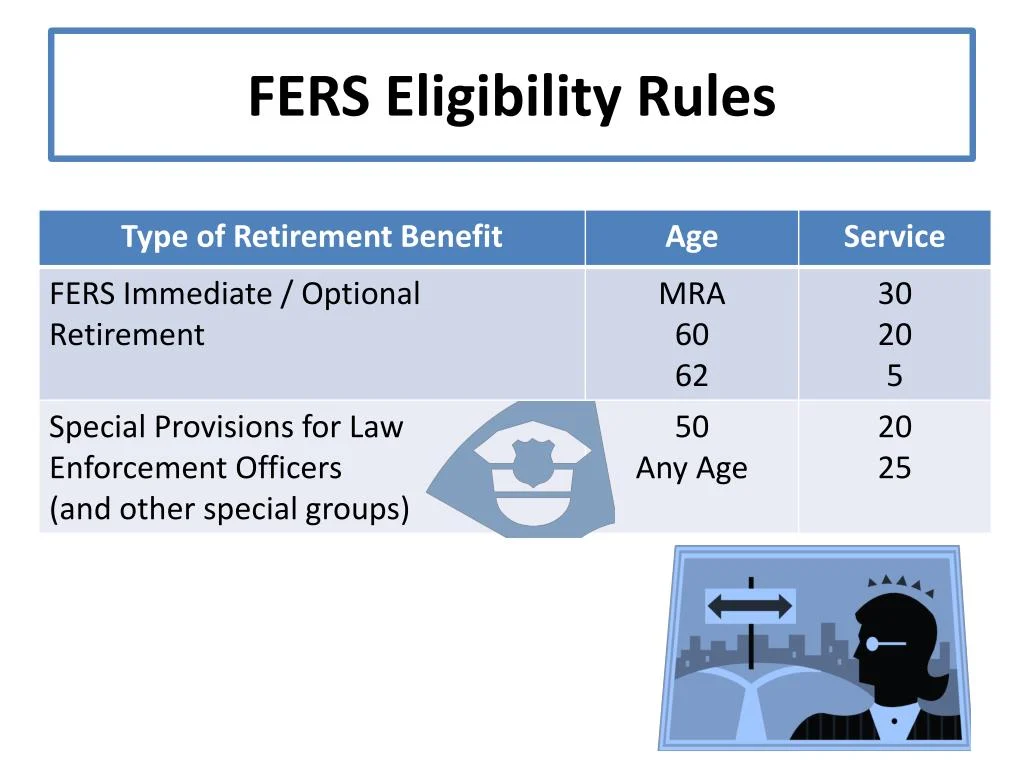

Can I Borrow From My FERS Retirement – Eligibility Rules

Because the FERS pension itself is a defined benefit plan, it’s designed to pay you a fixed monthly annuity once you reach eligibility age (usually 62 with 5 years of service, or 60 with 20 years). The system does not have a loan provision, which means you cannot simply “borrow” a portion of your future annuity and repay it later. The only way to access those funds before retirement is through a separation from service and a subsequent distribution.

If you’re still an active employee, the only realistic way to get cash is by:

- Taking a after‑tax retirement annuity from a separate retirement product you own, not from FERS itself.

- Applying for a short‑term personal loan from a bank or credit union, using your steady federal salary as a strong repayment credential.

Can I Borrow From My FERS Retirement – Tax and Penalty Implications

When you withdraw money from your TSP before meeting the age and service requirements, the IRS treats it as ordinary income. If you’re under 59½, a 10% early‑withdrawal penalty typically applies, unless you qualify for an exception (e.g., separation from service after age 55, certain medical expenses, or a qualified first‑time home purchase). The penalty can turn a seemingly attractive cash infusion into a costly move.

Let’s illustrate with a quick example: Suppose you have $50,000 in your TSP and need $10,000 for a home repair. If you withdraw that amount at age 54, you’ll owe ordinary income tax on the $10,000 (let’s say 22% federal tax) plus a $1,000 penalty (10%). That’s $3,200 in taxes and penalties, leaving you with only $6,800. The net cost is 32% of the amount you wanted.

Alternative Strategies When You Need Money Fast

Because “borrowing” directly from FERS isn’t an option, consider these alternatives that can preserve your retirement security:

- Emergency Savings Fund – Building a separate emergency fund of 3‑6 months of living expenses is the most straightforward safety net.

- Short‑Term Loan from a Credit Union – Federal employees often receive favorable rates from credit unions that understand the stability of government salaries.

- HELOC or Home Refinancing – If you own a home, tapping equity can be cheaper than a personal loan, especially if you can secure a low interest rate.

- Rollover to an IRA with Loan Feature – After you leave federal service, rolling your TSP into an IRA that permits loans can give you a limited borrowing option, but remember the loan must be repaid within five years and you’ll lose any tax‑advantaged growth on the borrowed amount.

Each of these routes has its own eligibility requirements and cost structures, so it’s worth running the numbers before you decide.

Impact on Your Future FERS Pension

Even though you can’t take a loan directly against the pension, any early withdrawal from the TSP reduces the balance that will later be rolled into your retirement income. The FERS pension formula is based on your highest three years of basic pay and years of service, so the pension itself isn’t directly affected by TSP withdrawals. However, the supplemental income you would have received from the TSP can be a significant portion of your overall retirement budget.

If you’re planning a phased retirement or anticipate needing extra cash in the first few years after you leave, think about how a reduced TSP balance might affect your lifestyle. You might offset the shortfall by:

- Delaying Social Security benefits to increase your monthly payout.

- Investing in low‑risk, income‑generating assets such as a dividend‑focused mutual fund (for example, the nuveen large cap growth index fund retirement).

- Utilizing a part‑time job or consulting work during the early retirement years.

Can I Borrow From My FERS Retirement and Still Qualify for Benefits?

Eligibility for other federal benefits—like the Federal Employees Health Benefits (FEHB) program or the Federal Employees Group Life Insurance (FEGLI)—is not directly tied to your TSP balance. However, if you reduce your overall retirement savings dramatically, you might find yourself relying more heavily on these programs, which could affect your budgeting decisions.

In short, borrowing (or withdrawing) from your retirement savings can create a cascade of financial adjustments. That’s why many financial planners advise treating early TSP withdrawals as a last resort, reserved for true emergencies or situations where the cost of borrowing elsewhere outweighs the tax penalties.

Practical Tips for Managing Cash Flow Without Borrowing from FERS

Even though the answer to “can i borrow from my fers retirement” is a firm no, there are proactive steps you can take to ensure you won’t need to consider it in the first place:

- Build a Tiered Savings Strategy – Keep three buckets: an emergency fund (high‑yield savings), a short‑term goal fund (money‑market account), and a long‑term growth fund (TSP or IRA).

- Automate Contributions – Set up automatic transfers from your checking account to your savings buckets right after each paycheck arrives.

- Review Your Budget Annually – Small adjustments—like reducing discretionary spending or refinancing high‑interest debt—can free up cash that you might otherwise consider borrowing.

- Leverage Federal Employee Discounts – Many banks, insurance providers, and retailers offer reduced rates for federal workers; these savings can accumulate into a meaningful buffer.

- Consider a Roth Conversion – If you’re in a lower tax bracket now, converting a portion of your TSP to a Roth IRA can give you tax‑free withdrawals later, essentially providing a “tax‑free loan” in retirement.

When you combine disciplined saving with smart use of available benefits, the need to ask “can i borrow from my fers retirement” often disappears.

Can I Borrow From My FERS Retirement? Frequently Asked Questions

Q: Can I take a loan against my TSP like I can with a 401(k)?

A: No. The TSP does not offer a loan provision, regardless of whether you’re still employed or retired.

Q: If I separate from federal service at age 55, can I withdraw without penalty?

A: Yes. The “age 55 rule” applies to federal employees who separate after age 55, allowing penalty‑free withdrawals (though taxes still apply).

Q: Are there any circumstances where a FERS pension can be used as collateral?

A: Not directly. Some lenders may consider your future annuity as part of your overall credit profile, but you cannot legally pledge the pension itself as collateral.

Q: Could a life insurance policy serve as a substitute for borrowing?

A: Absolutely. Certain permanent life insurance policies build cash value that you can borrow against. For a deeper dive, read Can Life Insurance Be Used for Retirement?.

Wrapping It Up

While the instinct to “borrow” from any retirement account is understandable, the Federal Employees Retirement System simply does not support direct loans. Instead, you’ll need to explore other financial tools—early withdrawals (with tax and penalty considerations), IRA rollovers, HELOCs, or personal loans—each with its own set of rules and costs.

The key takeaway is to treat any early access to retirement money as a strategic decision rather than a quick fix. By building robust emergency savings, understanding the tax landscape, and leveraging alternative financing options, you can protect the long‑term value of your FERS benefits while still meeting short‑term cash needs.

Remember, the strength of a federal retirement plan lies in its stability and predictability. Preserving that foundation will serve you far better than a short‑term cash infusion that could jeopardize years of hard work.