Getrawbox Getrawbox

Getrawbox Getrawbox

Related Articles

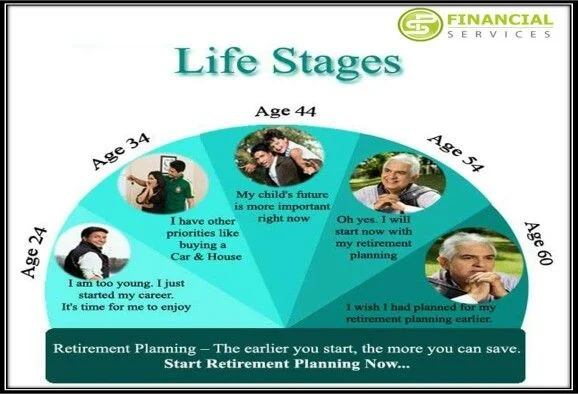

Planning for retirement can feel like navigating a maze with endless twists and turns. One moment you’re figuring out how much you need to save, and the next you’re wondering whether a 401(k) or an IRA is the better fit. The truth is, you don’t have to go it alone. Knowing exactly who to talk to about retirement planning can make the difference between a smooth transition into your golden years and a stressful scramble for cash.

In this article we’ll walk you through the key players you should consider adding to your retirement planning team. From certified financial planners who can map out your investment strategy to tax specialists who keep more of your money in your pocket, we’ll break down the roles, the questions to ask, and how to pick the right professional for your unique situation.

Whether you’re just starting your career, hitting the mid‑life mark, or already retired and looking to stretch your nest egg, having the right experts in your corner is essential. Let’s dive into who to talk to about retirement planning and how each conversation can bring you one step closer to a financially secure future.

who to talk to about retirement planning: Building Your Advisory Team

Think of retirement planning as a collaborative project. No single person has all the answers, but a well‑rounded team can cover every angle—investment growth, tax efficiency, risk management, and lifestyle considerations. Below are the main professionals you should consider adding to your roster.

who to talk to about retirement planning – Choosing the Right Financial Advisor

A certified financial planner (CFP) or a registered investment advisor (RIA) is often the first name that comes to mind. These professionals are trained to create comprehensive financial plans that align with your goals, risk tolerance, and time horizon. When you meet with a potential advisor, ask about:

- Their fiduciary status—are they legally obligated to act in your best interest?

- Fee structure—do they charge a flat fee, hourly rate, or a percentage of assets under management?

- Experience with retirement accounts—do they have a track record helping clients transition from accumulation to distribution phases?

Choosing a CFP who specializes in retirement can help you answer critical questions like how much to withdraw each year, when to claim Social Security, and which investment vehicles best suit your risk profile.

Tax Professionals: Who to Talk to About Retirement Planning Taxes

Tax implications can make or break your retirement budget. A qualified CPA or tax attorney can help you navigate the complexities of required minimum distributions (RMDs), Roth conversions, and the tax treatment of various retirement accounts. If you’re interested in a deeper dive, check out our Tax Planning to and Through Early Retirement: A Complete Guide for actionable strategies.

When interviewing a tax professional, discuss their experience with retirement‑specific issues and ask for examples of how they’ve helped clients minimize tax liabilities during the drawdown phase.

Human Resources and Workplace Benefits Specialists

Many employers offer retirement benefits that are often underutilized. Your HR department or a benefits specialist can explain the nuances of your 401(k) match, profit‑sharing plans, and any automatic enrollment features. They can also point you toward employer‑sponsored financial wellness programs, which sometimes include free consultations with external advisors.

Don’t overlook these internal resources—they’re usually free and can provide a solid foundation before you bring in outside experts.

Estate Planning Attorneys

Retirement isn’t just about income; it’s also about preserving wealth for your heirs. An estate planning attorney can help you draft wills, trusts, and powers of attorney that align with your retirement goals. They’ll ensure your assets are distributed according to your wishes while minimizing probate costs and potential tax burdens.

Insurance Agents and Longevity Risk Experts

Longevity risk—outliving your savings—is a real concern. An insurance agent can discuss annuities, long‑term care insurance, and other products that protect against unexpected health expenses or a longer-than-expected lifespan. While annuities aren’t for everyone, they can provide a guaranteed income stream that supplements your other retirement assets.

Social Security Advisors

Social Security benefits form a critical part of most retirement plans. Specialized advisors can run “break‑even” analyses to determine the optimal age to claim benefits based on your health, life expectancy, and other income sources. Timing your claim correctly can add thousands of dollars to your lifetime benefits.

How to Vet the Professionals You’ll Talk to About Retirement Planning

Now that you know who to talk to about retirement planning, the next step is vetting them. Here are some practical tips to ensure you’re working with qualified, trustworthy experts.

Check Credentials and Licenses

Look for certifications such as CFP, CPA, or Chartered Financial Analyst (CFA). Verify their licenses through regulatory bodies like the SEC’s Investment Adviser Public Disclosure (IAPD) website or the FINRA BrokerCheck tool.

Ask for References

Speak with current or former clients who have similar retirement goals. Their experiences can provide insight into the advisor’s communication style, responsiveness, and overall effectiveness.

Understand the Fee Structure

Transparent fees are a hallmark of a trustworthy advisor. Avoid “hidden” commissions by choosing fee‑only planners whenever possible. A clear fee schedule helps you compare costs across different professionals.

Review Their Planning Process

Good advisors will walk you through a step‑by‑step plan, including cash flow projections, investment allocation, and risk assessment. Ask for a sample financial plan to see how detailed and personalized their approach is.

Assess Their Communication Style

Retirement planning is an ongoing conversation, not a one‑time meeting. Choose someone who explains concepts in plain language, is accessible for follow‑up questions, and provides regular updates on your portfolio’s performance.

Common Scenarios: Who to Talk to About Retirement Planning at Different Life Stages

Everyone’s retirement journey is unique, but certain life events often dictate which professional you should prioritize.

Early‑Career Professionals

If you’re in your 20s or 30s, a financial advisor who specializes in retirement savings can help you set realistic contribution targets and choose the right mix of tax‑advantaged accounts. You might also want to talk to a tax professional early on to understand the benefits of Roth versus traditional contributions.

Mid‑Life Employees (40‑55)

At this stage, you’ll likely have a larger nest egg and may be considering catch‑up contributions. An estate planning attorney becomes more relevant as you start thinking about legacy. Additionally, a benefits specialist can ensure you’re maximizing employer matches and exploring any available pension plans.

Pre‑Retirees (55‑70)

Transitioning from accumulation to distribution is a delicate phase. This is the time to lean heavily on your financial advisor for withdrawal strategies, a tax professional for RMD planning, and a Social Security advisor for benefit timing. You may also explore annuity options with an insurance agent to lock in guaranteed income.

Retirees (70+)

Once you’re drawing down assets, the focus shifts to preserving wealth and managing healthcare costs. An estate planning attorney and a longevity risk expert become your primary contacts. Regular check‑ins with a tax professional can also help you stay on top of any changes in tax law that affect your withdrawals.

Putting It All Together: A Sample Retirement Planning Conversation Flow

Here’s a practical roadmap you can follow the next time you sit down to discuss retirement planning with a professional.

- Start with a Financial Advisor: Outline your current assets, debts, and retirement goals. Get a high‑level plan that includes investment allocation and projected savings needed.

- Bring in a Tax Professional: Review the advisor’s plan for tax efficiency. Discuss strategies like Roth conversions, charitable contributions, and timing of withdrawals.

- Consult Your HR/Benefits Specialist: Verify that you’re maximizing any employer contributions, understand vesting schedules, and explore any additional retirement benefits.

- Meet an Estate Planning Attorney: Draft or update wills, trusts, and powers of attorney. Ensure your plan aligns with your desired legacy.

- Talk to an Insurance Agent: Evaluate if an annuity or long‑term care policy fits into your risk mitigation strategy.

- Check in with a Social Security Advisor: Run simulations to decide the optimal age to claim benefits based on your overall financial picture.

This systematic approach ensures you’re covering all bases and that each professional’s advice complements the others, rather than creating conflicting strategies.

Remember, the best retirement plan is one that evolves with you. As your circumstances change—whether you receive a windfall, encounter a health issue, or decide to travel the world—keep the conversation open with your team. Regular reviews (at least annually) can help you stay on track and make adjustments before small issues become big problems.

In the end, the answer to “who to talk to about retirement planning” isn’t a single person but a network of experts who each bring a piece of the puzzle. By assembling the right crew, you empower yourself to make informed decisions, protect your assets, and enjoy the retirement you’ve worked so hard to build.

Ready to start building your retirement advisory team? Begin with a simple conversation with a certified financial planner and let the momentum carry you through the rest of the process.