Getrawbox Getrawbox

Getrawbox Getrawbox

Related Articles

Running a non‑profit means juggling mission‑driven goals with the everyday realities of budgeting, compliance, and staff retention. While many leaders focus on fundraising and program delivery, securing a solid retirement benefit for employees often slips through the cracks. Yet, a well‑crafted retirement plan can be a powerful tool for attracting talent, enhancing morale, and reinforcing the organization’s commitment to its people.

In this article we’ll walk through the essentials of retirement plans for non‑profit organizations. From the basics of eligibility and tax‑advantaged options to practical tips on implementation and communication, you’ll come away with a clear roadmap to build a plan that fits your budget and mission. Whether you’re a small charity just starting out or a mid‑size foundation looking to upgrade existing benefits, the strategies below can help you make informed decisions.

Before we dive into the details, it’s worth remembering that “one size fits all” rarely applies in the nonprofit sector. The right retirement solution depends on factors such as staff size, revenue streams, and long‑term financial outlook. By the end of this guide, you’ll be equipped to evaluate those variables, compare plan types, and choose a path that aligns with both fiscal responsibility and employee well‑being.

Retirement Plans for Non‑Profit Organizations: Core Options Explained

Non‑profit organizations have access to several retirement plan structures that differ in cost, complexity, and tax treatment. Below is an overview of the most common choices.

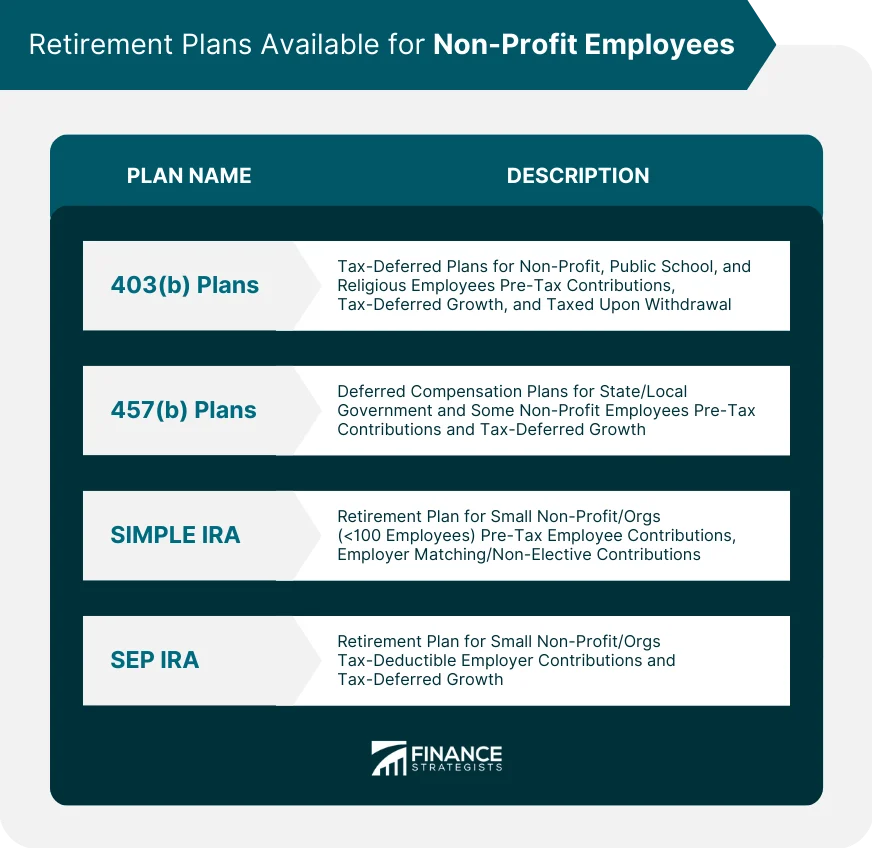

401(k) and 403(b) Plans for Non‑Profit Organizations

A 403(b) plan is the classic retirement vehicle for public schools, hospitals, and many charities. It operates similarly to a 401(k) but is tailored to tax‑exempt entities. Contributions are made pre‑tax, reducing employees’ taxable income, while the organization may also elect to make matching contributions.

- Eligibility: Generally available to all full‑time staff, though part‑time employees can be included if they meet a minimum service threshold.

- Employer Contributions: Matching up to 3‑5% of salary is common and often qualifies for the small‑business retirement plan tax credit.

- Administrative Burden: Requires annual Form 5500 filing and adherence to nondiscrimination testing, but many third‑party providers handle these tasks.

For organizations with a larger payroll, a traditional 401(k) might be an alternative, especially if they already have a for‑profit subsidiary or want to offer a broader investment menu. The decision between 401(k) and 403(b) often hinges on provider relationships and the specific needs of the workforce.

Simple IRA and SEP IRA Options

If your nonprofit is on the smaller side—say fewer than 100 employees—a Simple IRA or SEP IRA can provide a low‑cost, easy‑to‑administer retirement solution.

- Simple IRA: Allows employee salary deferrals up to $15,500 (2024 limit) with mandatory employer contributions of either 2% of compensation or a matching contribution up to 3%.

- SEP IRA: Employer‑only contributions up to 25% of compensation (capped at $66,000 for 2024), making it attractive for organizations that prefer to contribute rather than manage employee payroll deductions.

Both plans qualify for the same tax‑deduction benefits as larger 403(b) plans, but they sidestep many of the compliance complexities, making them a great entry point for nonprofits just beginning to think about retirement benefits.

Roth Variants and Hybrid Models

Roth 403(b) or Roth 401(k) options let employees contribute after‑tax dollars, meaning qualified withdrawals in retirement are tax‑free. Including a Roth component can appeal to younger staff who anticipate being in a higher tax bracket later on. Some providers also offer hybrid solutions—combining traditional pre‑tax and Roth contributions—giving participants flexibility to tailor their savings strategy.

Designing a Retirement Plan That Aligns With Your Mission

Choosing the right vehicle is only half the battle. A retirement plan should reinforce the organization’s values and operational realities. Here are key design considerations.

Budgeting for Employer Contributions

While employee deferrals are voluntary, many nonprofits find that offering a modest match dramatically improves recruitment and retention. A common approach is a 3% match on the first 6% of salary deferral. For a staff member earning $40,000, this translates to a $720 annual contribution—an amount most small charities can comfortably absorb.

Don’t forget to explore the Small Business Retirement Plan Tax Credit. This credit can offset up to 50% of the costs associated with setting up and administering a new plan, up to $5,000 per year, for qualifying employers.

Choosing a Provider That Understands Non‑Profit Needs

Not all retirement plan administrators treat nonprofit clients equally. Look for providers that:

- Offer reduced fees for tax‑exempt organizations.

- Provide educational resources tailored to mission‑driven staff.

- Have experience filing Form 5500 for charities.

Many providers also bundle financial wellness tools, which can be especially useful for employees navigating limited salaries and high living costs.

Communicating the Value to Employees

Even the best‑designed plan won’t deliver results if staff don’t understand it. A clear communication strategy should include:

- Kick‑off webinars during onboarding.

- Quarterly newsletters highlighting enrollment deadlines and matching contributions.

- One‑on‑one counseling sessions with a certified retirement advisor.

For guidance on finding the right advisor, check out Who Do I Talk to About Retirement? Your Guide to the Right Advisors. A knowledgeable advisor can demystify investment choices and help employees align their contributions with long‑term goals.

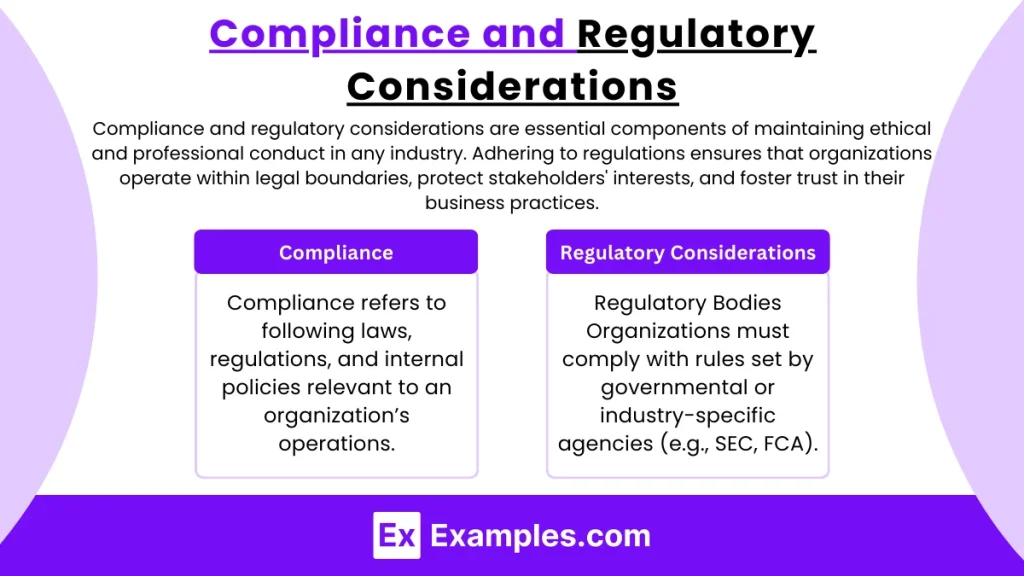

Legal and Compliance Considerations

Retirement plans for non‑profit organizations are subject to the same ERISA regulations as for‑profit plans. Key compliance checkpoints include:

- Nondiscrimination Testing: Ensures that the plan does not disproportionately favor highly compensated employees.

- Annual Reporting (Form 5500): Required for most 401(k) and 403(b) plans; deadlines are typically July 31 of the following year.

- Plan Documentation: The plan must be written, adopted, and made available to participants.

Failure to meet these obligations can result in penalties and jeopardize the organization’s tax‑exempt status. Engaging a fiduciary‑aware administrator or consulting a tax professional familiar with nonprofit law is a prudent safeguard.

Leveraging Retirement Plans for Fundraising and Donor Relations

It may sound unconventional, but a robust retirement benefit can become a subtle fundraising asset. Here’s how:

Showcasing Employee Investment in the Mission

Prospective donors often look for signs that an organization treats its staff well. Highlighting a competitive retirement plan in annual reports or grant applications can signal fiscal responsibility and long‑term stability.

Matching Gift Programs Tied to Retirement Savings

Some foundations encourage employees to make charitable contributions from their retirement accounts (e.g., Qualified Charitable Distributions). By educating staff about these options, nonprofits can potentially boost charitable giving while reinforcing the organization’s mission.

Case Study: Implementing a 403(b) Plan at a Mid‑Size Arts Charity

“The Creative Hub,” a nonprofit serving 75 employees, decided in 2022 to transition from a Simple IRA to a 403(b) plan. Their objectives were to improve benefits, qualify for the small‑business retirement plan tax credit, and provide a Roth option.

Key steps they followed:

- Conducted a staff survey to gauge interest and preferred contribution levels.

- Partnered with a provider experienced in arts‑sector nonprofits, securing a 15% fee discount.

- Implemented a 3% matching policy, funded through a modest reallocation of operating reserves.

- Hosted a series of workshops, referencing resources from Crafting an Effective Retirement Plan for Non Profit Organizations to ensure consistent messaging.

Within one year, enrollment rose from 42% to 78%, and employee turnover dropped by 12%. The organization also claimed a $3,200 tax credit, effectively offsetting the first‑year administrative costs.

Future Trends to Watch

Retirement plans for non‑profit organizations are evolving alongside broader financial trends. Here are three developments to keep on your radar:

Increased Adoption of ESG‑Aligned Investment Options

Many employees now expect their retirement savings to reflect personal values. Providers are adding ESG (Environmental, Social, Governance) funds, allowing staff to invest in companies that align with the nonprofit’s mission.

Digital Enrollment Platforms

Streamlined, mobile‑first enrollment experiences reduce administrative overhead and improve participation rates. Look for providers offering secure, cloud‑based portals that integrate with payroll systems.

Hybrid Retirement Savings Models

Some organizations are experimenting with blended plans that combine a modest 403(b) with a supplemental payroll‑deduction savings account, giving staff more flexibility without adding significant compliance burdens.

Staying abreast of these trends can help your nonprofit remain competitive in the talent market while safeguarding long‑term financial health.

In summary, crafting a retirement plan for a non‑profit organization is a strategic investment that pays dividends in staff satisfaction, compliance confidence, and mission sustainability. By carefully assessing your organization’s size, budget, and goals, selecting the right plan type, and communicating its benefits effectively, you can create a retirement solution that not only meets regulatory requirements but also reinforces the core values that drive your work.

Remember, the journey doesn’t end with plan adoption. Ongoing education, regular reviews of contribution levels, and periodic consultations with fiduciary‑savvy advisors will keep the program vibrant and responsive to both employee needs and organizational changes. With thoughtful planning and a commitment to continuous improvement, retirement plans for non‑profit organizations can become a cornerstone of a thriving, mission‑focused workplace.