Getrawbox Getrawbox

Getrawbox Getrawbox

Related Articles

Planning for retirement can feel like trying to predict the weather a decade in advance. You want a strategy that balances growth with safety, adapts to market shifts, and aligns with your personal timeline. One popular tool that aims to do exactly that is the american funds 2040 trgt date retire r6. If you’re targeting retirement around the year 2040, this fund might already be on your radar, but what does it really offer? How does its “R6” designation affect its risk profile? And most importantly, does it make sense for your unique financial situation?

In this article we’ll break down the fund’s core components, walk through its asset allocation, discuss the pros and cons, and give you practical tips on how to incorporate it into a broader retirement plan. Whether you’re a seasoned investor comfortable with target‑date funds or a beginner looking for a “set‑and‑forget” solution, the insights here will help you decide if the american funds 2040 trgt date retire r6 deserves a spot in your portfolio.

Before diving deep, remember that no single fund can guarantee a perfect retirement. It’s always wise to pair any investment with a solid savings habit, emergency fund, and, when appropriate, professional advice. If you’re curious about other retirement‑related topics, you might also enjoy reading about Life Insurance as a Retirement Plan or exploring how to use retirement to pay off debt.

Understanding the american funds 2040 trgt date retire r6

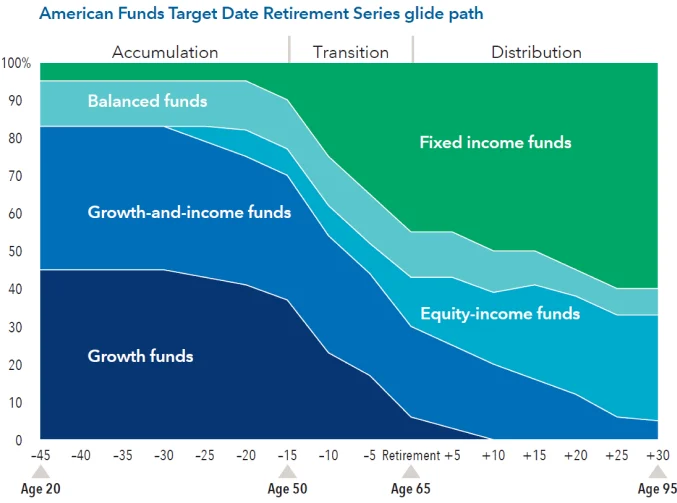

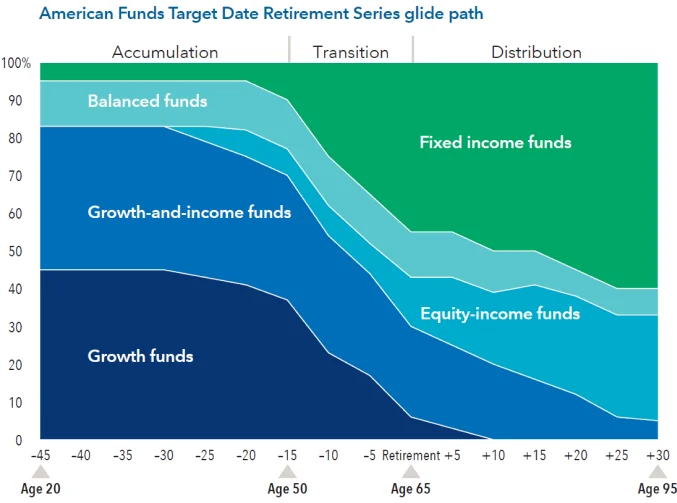

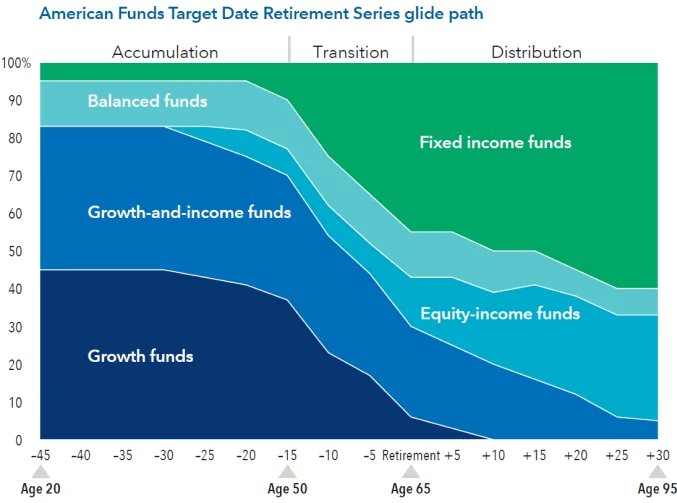

The american funds 2040 trgt date retire r6 is part of American Funds’ Target Date series, a collection of mutual funds designed to automatically shift asset allocation as the target retirement year approaches. The “2040” indicates the expected retirement year, while “R6” denotes the risk level—R6 being a moderate‑to‑moderately‑aggressive stance. This risk tier typically translates to a mix that leans more heavily on equities early on, gradually adding bonds and other fixed‑income assets as 2040 nears.

Here’s a snapshot of the typical glide path for an R6 fund:

- Early years (2020‑2025): Roughly 80% equities, 20% fixed income.

- Mid‑stage (2026‑2035): Around 70% equities, 30% fixed income.

- Approach to retirement (2036‑2040): About 60% equities, 40% fixed income.

- Post‑retirement (2041+): Shifts further toward 50/50 or even more conservative, depending on the specific fund’s policy.

This gradual de‑risking is meant to protect investors from market volatility as they get closer to needing the money. However, the exact percentages can vary slightly based on market conditions and the fund manager’s discretion.

Key components of the american funds 2040 trgt date retire r6

Understanding the building blocks helps you see where the risk and return come from:

- U.S. Large‑Cap Stocks: These form the core equity exposure, providing growth potential from established companies.

- International Stocks: Adding diversification beyond the U.S. market, capturing growth in emerging and developed economies abroad.

- Small‑Cap & Mid‑Cap Stocks: Higher volatility but can boost long‑term returns.

- Bond Funds: A blend of government, corporate, and mortgage‑backed securities aimed at generating stable income.

- Real Estate and Alternative Assets (in some versions): Provide further diversification and potential inflation protection.

Because the fund is managed by American Funds, you also get the benefit of a seasoned investment team that conducts rigorous research and adheres to a disciplined rebalancing schedule.

Why investors choose the american funds 2040 trgt date retire r6

Target‑date funds have surged in popularity for several reasons, and the american funds 2040 trgt date retire r6 is no exception. Below are the main attractions:

- Convenience: One ticker, one purchase, and the fund automatically adjusts over time. No need to manually rebalance.

- Diversification: By holding a mix of stocks, bonds, and sometimes real assets, you gain exposure to multiple market segments without buying each individually.

- Professional Management: The fund’s managers continuously monitor market trends and adjust holdings, which can be especially valuable for investors without the time or expertise to do so themselves.

- Risk Alignment: The R6 designation gives a clear picture of the fund’s risk level, helping you match it with your comfort zone.

For many, the biggest selling point is the “set‑and‑forget” nature. If you’re contributing to a 401(k) or IRA through an employer plan, you can often select the target‑date fund as your default option, and the contributions will automatically flow into the appropriate vehicle.

Potential drawbacks of the american funds 2040 trgt date retire r6

No investment is without its trade‑offs. Here are some considerations that might make you think twice:

- Higher fees than index funds: While American Funds’ expense ratios are competitive within the actively managed space, they are typically higher than low‑cost index ETFs.

- One‑size‑fits‑all glide path: The automatic de‑risking may not align perfectly with your personal timeline or risk tolerance. If you plan to retire earlier or later than 2040, you may need to adjust.

- Potential for overexposure to U.S. equities: Even with international holdings, the bulk of the equity portion is U.S.-centric, which could be a concern if you anticipate a shift in global growth patterns.

- Liquidity considerations: As with any mutual fund, you’ll need to wait until the market close to execute trades, unlike ETFs that trade throughout the day.

If any of these points raise a red flag, you might want to explore other retirement options. For instance, the American Funds 2040 Target Date Retirement Fund – A Deep Dive for Future Retirees article provides a broader perspective on similar funds and may help you compare alternatives.

How the american funds 2040 trgt date retire r6 fits into a holistic retirement plan

A single fund can’t cover every aspect of retirement planning. Think of the american funds 2040 trgt date retire r6 as a core holding that provides growth and a built‑in safety net, but you’ll likely need additional pieces to complete the puzzle:

- Emergency Savings: Keep 3‑6 months of living expenses in a liquid account to avoid dipping into retirement assets during market dips.

- Tax‑Advantaged Accounts: Maximize contributions to 401(k)s, IRAs, or Roth IRAs to benefit from tax deferral or tax‑free growth.

- Supplemental Investments: Consider adding a low‑cost index fund or a small allocation to a real‑estate investment trust (REIT) for extra diversification.

- Insurance and Estate Planning: Tools like life insurance, long‑term care coverage, and a will can protect your assets and loved ones. For more on life‑insurance options, check out Life Insurance as a Retirement Plan.

When you blend these elements, the target‑date fund acts as the engine that drives growth, while the other components cushion volatility and address non‑investment risks.

Tips for maximizing the american funds 2040 trgt date retire r6

Even a “hands‑off” fund can benefit from a few strategic moves:

- Periodic Review: At least once a year, assess whether the fund’s risk level still matches your comfort zone. If you’ve experienced a major life change—marriage, a new child, or a shift in career—consider adjusting your allocation.

- Stay the Course: Market volatility can tempt investors to sell during downturns. Remember that the fund’s glide path is designed for long‑term horizons, so resist the urge to make reactionary moves.

- Combine with a Small‑Cap Tilt: If you crave a bit more growth, you could allocate a modest portion of your portfolio (5‑10%) to a dedicated small‑cap fund, complementing the broader exposure in the target‑date fund.

- Utilize Dollar‑Cost Averaging: Consistent contributions smooth out market timing risk, especially important for a fund that will experience both bull and bear markets before 2040.

Comparing the american funds 2040 trgt date retire r6 with other options

When you’re evaluating the american funds 2040 trgt date retire r6, it helps to line it up against a few alternatives:

- Vanguard Target Retirement 2040 Fund (VTIVX): Typically lower expense ratios, but a slightly different glide path that may be more conservative in the early years.

- Fidelity Freedom 2040 Fund (FFFEX): Similar risk level, but with a heavier emphasis on international exposure.

- Self‑Built Portfolio: Using a mix of index ETFs (e.g., VTI, VXUS, BND) can lower costs, but requires more active management.

Choosing between them hinges on three factors: fee sensitivity, desire for active versus passive management, and confidence in handling rebalancing yourself. If you’re comfortable with a bit more hands‑on approach and want to shave off expenses, a DIY portfolio could win. Conversely, if you value the research depth and stability that American Funds provides, the american funds 2040 trgt date retire r6 remains a solid choice.

When to consider exiting the american funds 2040 trgt date retire r6

There are moments when staying in the fund might not align with your goals:

- Retirement has arrived: As you transition into the post‑retirement phase, you may want a more income‑focused allocation, such as a bond ladder or a dividend‑heavy equity fund.

- Significant change in risk tolerance: If you become more risk‑averse after a market crash, shifting to a lower‑risk target‑date fund (e.g., R5) could be prudent.

- Better opportunities emerge: If a new low‑cost fund with a superior glide path is introduced, it might merit a switch.

Always consult with a financial advisor before making major changes. If you’re not sure who to talk to, the article Who Do I Talk to About Retirement? Your Guide to the Right Advisors can help you find the right professional.

In summary, the american funds 2040 trgt date retire r6 offers a well‑structured, professionally managed path toward retirement for investors aiming around the 2040 horizon. Its moderate‑to‑moderately‑aggressive risk profile makes it a good fit for those who want growth early on but also desire a built‑in de‑risking mechanism as retirement approaches. While fees are higher than pure index options and the glide path may not suit every unique timeline, the fund’s convenience, diversification, and active oversight make it a compelling component of a broader retirement strategy.

Pair it with solid savings habits, complementary investments, and the right insurance safeguards, and you’ll be well‑positioned to enjoy a comfortable, financially secure retirement.