Getrawbox Getrawbox

Getrawbox Getrawbox

Related Articles

Planning for retirement can feel like navigating a maze, especially when you’re bombarded with countless fund options and jargon‑heavy brochures. One name that often pops up for investors eyeing a smooth ride toward their golden years is the American Funds 2025 target date retirement fund. Whether you’re a seasoned saver or just starting to think about life after work, understanding this fund’s design, risk profile, and how it fits into a broader retirement strategy is essential.

In this article we’ll break down the core components of the American Funds 2025 target date retirement fund, compare it with similar offerings, and give you practical tips on how to decide if it’s the right fit for your portfolio. By the end, you’ll have a clear picture of what makes this fund tick and how it can help you stay on track for a comfortable retirement.

Before we dive in, remember that a solid retirement plan isn’t just about picking a single fund. It’s about aligning your investments with your timeline, risk tolerance, and overall financial goals. If you’re still figuring out the basics of setting up a retirement account, you might want to check out How to Set Up Retirement Account – A Step‑by‑Step Guide for a helpful walkthrough.

American Funds 2025 Target Date Retirement Fund: An Overview

The American Funds 2025 target date retirement fund is part of a series of “target‑date” funds that automatically adjust their asset allocation as the target retirement year approaches. Specifically, this fund is designed for investors who plan to retire around the year 2025. Its glide path—a pre‑determined schedule of shifting from growth‑focused assets to more conservative investments—aims to balance growth potential with risk mitigation as you get closer to retirement.

Key features of the American Funds 2025 target date retirement fund include:

- Age‑Based Allocation: Starts with a higher proportion of equities (stocks) for growth, gradually moving toward bonds and cash equivalents.

- Diversified Portfolio: Holds a mix of American Funds’ own mutual funds, providing exposure to large‑cap, mid‑cap, small‑cap, international, and fixed‑income markets.

- Active Management: Fund managers actively select securities within each underlying fund, aiming to outperform passive benchmarks.

- Expense Ratio: Typically higher than index‑based target‑date funds but justified by active management and research capabilities.

Because it’s a “target date” product, you don’t have to manually rebalance your holdings each year. The fund’s managers take care of that for you, shifting assets from high‑risk to low‑risk categories as the 2025 target date draws nearer.

American Funds 2025 Target Date Retirement Fund: Asset Allocation Details

At launch, the fund’s allocation might look something like this:

- 55% equities (U.S. large‑cap, mid‑cap, small‑cap, and international stocks)

- 35% fixed income (government and corporate bonds, mortgage‑backed securities)

- 10% cash and short‑term instruments

As the fund moves through 2023, 2024, and finally 2025, the equity portion typically drops to around 30‑40%, while the fixed‑income and cash components rise to provide stability and preserve capital. This glide path mirrors the strategy used in the American Funds 2040 target date fund, which you can explore in more depth at American Funds 2040 Trgt Date Retire R6 – What You Need to Know.

Why Choose a Target Date Fund Like American Funds 2025?

Target‑date funds simplify retirement investing. Instead of juggling multiple mutual funds or ETFs, you select a single fund that aligns with your expected retirement year, and the fund’s managers handle the rest. For the American Funds 2025 target date retirement fund, the benefits include:

- Convenient “Set‑and‑Forget” Approach: Ideal for busy professionals who want a hands‑off strategy.

- Professional Oversight: Access to American Funds’ seasoned portfolio managers and research teams.

- Built‑In Diversification: Exposure to a wide array of asset classes reduces the impact of any single market downturn.

- Retirement‑Focused Rebalancing: The fund’s glide path automatically reduces volatility as you near retirement.

However, the convenience comes with a trade‑off—higher fees compared to index‑based target‑date alternatives. If you’re cost‑sensitive, you might weigh those fees against the potential for higher returns from active management.

American Funds 2025 Target Date Retirement Fund: Fees and Expenses

Understanding the cost structure is crucial because fees can erode your retirement nest egg over time. The American Funds 2025 target date retirement fund typically carries an expense ratio in the range of 0.70% to 0.85% annually. This includes management fees, administrative costs, and the underlying expenses of the mutual funds it holds.

While this fee is higher than some low‑cost index funds (which can be as low as 0.05%–0.15%), it reflects the active management approach and the extensive research resources that American Funds brings to the table. If you’re comfortable with a slightly higher cost in exchange for potentially better risk‑adjusted performance, the fund may still be a solid choice.

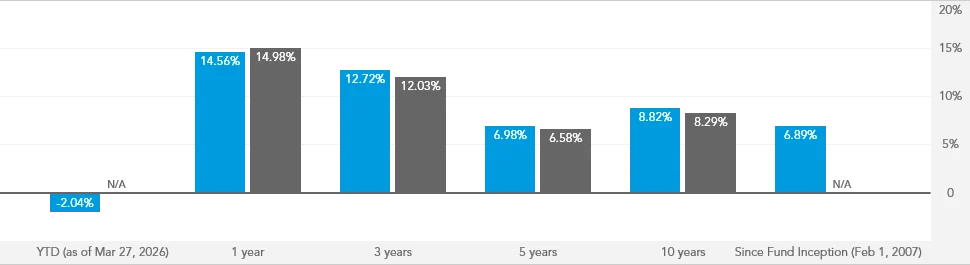

Performance Snapshot: How Has the American Funds 2025 Fund Performed?

Historical performance provides a glimpse into how the fund has navigated market cycles. Over the past five years, the American Funds 2025 target date retirement fund has delivered an average annual return of roughly 7%–8%, aligning closely with broader market benchmarks such as the S&P 500 plus a modest fixed‑income component. During periods of market turbulence, the fund’s diversified nature helped cushion losses better than a pure equity fund.

It’s important to remember that past performance is not a guarantee of future results. The fund’s future returns will depend on market conditions, the effectiveness of the managers’ stock selection, and the evolving composition of its asset mix as we move closer to 2025.

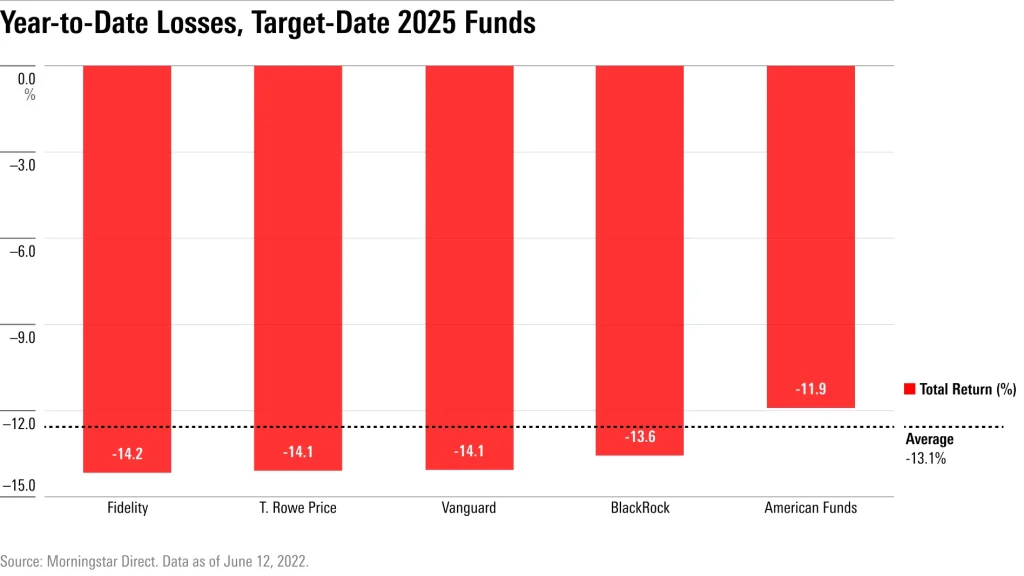

Comparing American Funds 2025 with Other Target Date Options

When evaluating the American Funds 2025 target date retirement fund, you might also consider alternatives from Vanguard, Fidelity, or T. Rowe Price. Many of those competitors offer lower expense ratios but rely more heavily on passive indexing strategies. If you value active management and the brand reputation of American Funds, the 2025 fund could be a better fit despite its higher cost.

For a deeper dive into a similar fund with a later retirement horizon, see American Funds 2040 Target Date Retirement Fund – A Deep Dive for Future Retirees. Comparing glide paths, risk levels, and fee structures across these products can help you fine‑tune your retirement strategy.

How to Incorporate the American Funds 2025 Fund into Your Retirement Plan

Integrating the American Funds 2025 target date retirement fund into a broader retirement plan requires a holistic view of your finances. Here are some steps to consider:

- Assess Your Current Savings: Determine how much you have saved in 401(k)s, IRAs, and other accounts.

- Evaluate Your Risk Tolerance: If you’re comfortable with moderate volatility, the 2025 fund’s equity exposure fits well.

- Check Employer Match Options: If your employer offers a matching contribution, prioritize that before allocating extra money to the target‑date fund.

- Diversify Beyond the Target Date Fund: While the 2025 fund covers many bases, you might still want a separate Roth IRA or taxable brokerage account for flexibility.

- Review Annually: Even though the fund rebalances automatically, a yearly review ensures it still aligns with any changes in your life—like a new job, a move, or an unexpected expense.

For newcomers who need a step‑by‑step framework on setting up retirement accounts, the guide How to Set Up Retirement Account – A Step‑by‑Step Guide walks you through everything from choosing a custodian to making your first contribution.

Tips for Maximizing the Benefits of American Funds 2025

To get the most out of the American Funds 2025 target date retirement fund, consider these practical tips:

- Start Early: The sooner you invest, the longer the compounding effect works in your favor.

- Contribute Consistently: Set up automatic payroll deductions to ensure regular contributions.

- Take Advantage of Tax‑Advantaged Accounts: Use a 401(k) or Traditional IRA to defer taxes on contributions, and consider a Roth IRA for tax‑free withdrawals later.

- Stay Informed About Fund Changes: American Funds may adjust the glide path or underlying holdings; keep an eye on fund updates.

- Don’t Forget Emergency Savings: Maintain a separate cash reserve so you’re not forced to sell investments during market dips.

Potential Drawbacks and Risks to Watch

While the American Funds 2025 target date retirement fund offers many advantages, it’s not without risks. Here are some considerations before you lock in your savings:

- Higher Expense Ratio: As mentioned, fees are above the industry average for passive funds.

- Market Risk: Even with a balanced allocation, the fund will still experience fluctuations, especially in the early years when equities dominate.

- Glide Path Inflexibility: The predetermined asset shift may not match every investor’s unique risk tolerance or changing financial situation.

- Potential Overlap: If you already hold other American Funds mutual funds, you might end up with duplicated exposure, reducing diversification benefits.

Balancing these risks against your personal retirement timeline and comfort level with volatility is essential. If you’re uncertain, consulting a financial advisor can provide tailored guidance.

When Might You Choose a Different Target Date?

If you anticipate retiring later than 2025 or want a more aggressive growth profile, you might opt for a fund with a later target year, such as the American Funds 2040 target date retirement fund. Conversely, if you plan to retire earlier or have a lower risk appetite, a fund targeting 2020 or 2022 could be more appropriate. The key is aligning the fund’s glide path with your own retirement horizon.

Final Thoughts on the American Funds 2025 Target Date Retirement Fund

Choosing the right retirement vehicle is a personal decision that hinges on your timeline, risk tolerance, and overall financial picture. The American Funds 2025 target date retirement fund offers a well‑structured, actively managed solution for those aiming to retire around 2025. Its diversified asset mix, automatic rebalancing, and reputable management team provide a convenient pathway for investors who prefer a “set‑and‑forget” approach.

That said, the higher expense ratio and predetermined glide path mean you should weigh it against lower‑cost, passive alternatives and ensure it meshes with the rest of your retirement portfolio. By reviewing your goals, staying disciplined with contributions, and periodically checking that the fund’s strategy still fits your evolving circumstances, you can make the American Funds 2025 target date retirement fund a solid component of a comprehensive retirement plan.

Remember, retirement planning is a marathon, not a sprint. Whether you end up selecting this fund, a different target‑date option, or a blend of individual mutual funds, the most important step is to start now and keep moving forward. Happy investing!

[Finance]: Finance