Getrawbox Getrawbox

Getrawbox Getrawbox

Related Articles

Saving for retirement might feel like a distant concern when you’re busy with daily work, bills, and short‑term goals. Yet the earlier you start, the more you benefit from compounding returns and tax advantages. Whether you’re fresh out of college, mid‑career, or approaching the “golden years,” figuring out how to get a retirement account is a foundational step toward financial security.

In this article we’ll walk through the different types of retirement accounts available, the eligibility requirements, and the practical actions you can take right now. We’ll also sprinkle in some real‑world tips—like when a target‑date fund might be a good fit or how you can even use retirement funds to launch a small business—so you can tailor the strategy to your unique situation.

By the end of the read, you’ll have a clear roadmap, know exactly where to open an account, and understand the key decisions that will shape your retirement nest egg. Let’s dive in!

how to get a retirement account: Choosing the Right Type

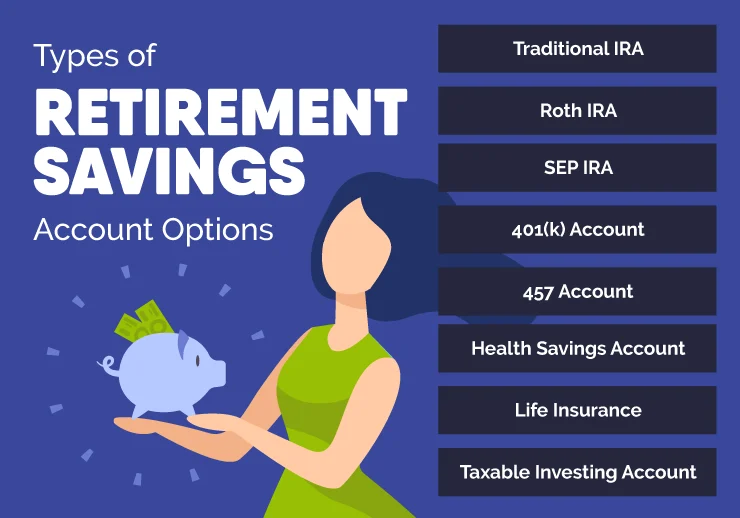

The first decision in how to get a retirement account is picking the vehicle that matches your employment status, income level, and long‑term goals. Below are the most common options:

- Employer‑Sponsored Plans – 401(k), 403(b), and 457 plans are offered by many companies and often include matching contributions.

- Individual Retirement Accounts (IRAs) – Traditional and Roth IRAs are opened independently of an employer.

- Self‑Employed Plans – SEP‑IRA, SIMPLE IRA, and Solo 401(k) are tailored for freelancers and business owners.

- Target‑Date Funds – A “set‑and‑forget” option that automatically shifts asset allocation as you approach retirement.

how to get a retirement account: Opening an Employer‑Sponsored Plan

If you work for a company that offers a 401(k) or similar plan, the process is usually straightforward:

- Enroll during the company’s open enrollment period or when you become eligible (often after 30 days of service).

- Choose your contribution rate. A common recommendation is at least enough to capture the full employer match.

- Select your investment mix. Many participants opt for a target‑date fund, like the Vanguard Target Retirement 2040 Trust Select, which automatically rebalances over time.

- Set up automatic payroll deductions. This “pay‑it‑forward” method ensures consistent savings without extra effort.

Remember, the key to how to get a retirement account through your employer is to act early and take full advantage of any matching contributions—otherwise, you’re essentially leaving free money on the table.

how to get a retirement account: Starting an IRA on Your Own

When you don’t have access to an employer plan, an IRA is the go‑to solution. Here’s how to get a retirement account of this type:

- Determine eligibility. For a Traditional IRA, you need earned income; for a Roth IRA, there are income limits.

- Select a brokerage or financial institution. Look for low fees, a broad selection of investments, and solid customer service.

- Complete the application. Most platforms allow you to sign up online in minutes, providing your personal information and linking a bank account.

- Fund the account. You can contribute up to $6,500 per year (or $7,500 if you’re 50 or older) for 2024.

- Choose your investments. Many beginners start with a diversified portfolio of index funds or a target‑date fund such as the American Funds 2025 Target Date Retirement Fund.

Opening an IRA is a perfect illustration of how to get a retirement account without relying on an employer. The flexibility to choose investments and contribution limits makes it a versatile cornerstone of any retirement strategy.

Step‑by‑Step Blueprint: How to Get a Retirement Account from Scratch

Now that you know the options, let’s break down the exact steps you should follow, no matter which route you choose. This step‑by‑step guide is designed to be actionable and easy to follow.

Step 1: Assess Your Financial Situation

Before you dive into how to get a retirement account, take a quick inventory of your income, expenses, and existing debt. Use a simple spreadsheet or budgeting app to see how much you can realistically set aside each month for retirement.

Step 2: Choose the Right Account Type

Based on your employment status and income, decide whether an employer‑sponsored plan, an IRA, or a self‑employed plan is the best fit. If you’re unsure, you can always open an IRA first and later add a 401(k) if your job offers one.

Step 3: Pick a Provider

Look for providers with low expense ratios, a solid reputation, and user‑friendly platforms. Companies like Vanguard, Fidelity, and Charles Schwab frequently appear in top‑ranked lists. For a deep dive on a specific fund, check out the How to Set Up Retirement Account – A Step‑by‑Step Guide article for more detailed instructions.

Step 4: Complete the Application

Most providers let you finish the paperwork online. You’ll need to provide your Social Security number, contact details, and bank account information for funding. Keep a copy of your confirmation number for future reference.

Step 5: Fund the Account

Set up an initial contribution—often as low as $50—and schedule recurring contributions that align with your budget. Automating the process helps you stay consistent, which is vital when learning how to get a retirement account that truly grows over time.

Step 6: Choose Investments Wisely

If you’re not an investment guru, a target‑date fund can simplify the process. For instance, the American Funds 2040 Trgt Date Retire R6 automatically shifts toward more conservative assets as 2040 approaches. Alternatively, you can build a diversified mix of index funds, bonds, and perhaps a few individual stocks.

Step 7: Review and Adjust Annually

Life changes—salary bumps, marriage, kids, or a new job—so revisit your retirement strategy at least once a year. Increase contributions when possible, and rebalance your portfolio to stay aligned with your risk tolerance.

Special Considerations When Learning How to Get a Retirement Account

Tax Implications

Understanding the tax side of things is essential. Traditional accounts let you defer taxes until withdrawal, while Roth accounts tax‑free your earnings if you follow the rules. Knowing which option suits your current and expected future tax bracket can significantly affect your long‑term wealth.

Using Retirement Funds for Business Ventures

Did you know you can leverage retirement savings to start a business? The Using Retirement Funds to Start a Business – A Practical Guide explains how a Rollover as Business Startup (ROBS) allows you to invest your 401(k) or IRA into a new company without penalties. While it’s an advanced tactic, it’s another facet of how to get a retirement account that can serve multiple financial goals.

Retirement Accounts for Non‑Profit Employees

Non‑profit workers often have access to 403(b) plans, which function similarly to 401(k)s but are tailored for tax‑exempt organizations. If you’re part of a charitable or educational institution, look into a 403(b) to see if it offers matching contributions or lower fees.

Life Insurance as a Retirement Tool

Some high‑net‑worth individuals use permanent life insurance policies as a supplemental retirement vehicle. While not a primary method of how to get a retirement account, it’s a strategy worth exploring if you’re interested in tax‑advantaged cash value growth. For a deep dive, see the Life Insurance as a Retirement Plan: A Comprehensive Guide.

Common Pitfalls and How to Avoid Them

- Procrastination: Delaying the first contribution can cost you thousands in lost compound growth. Set a calendar reminder to open your account within 30 days of deciding.

- Overlooking Employer Match: Not contributing enough to capture the full match is essentially leaving free money on the table.

- Choosing High‑Fee Funds: Fees eat into returns. Opt for low‑expense index funds or reputable target‑date funds.

- Ignoring Tax Implications: Failing to consider whether a Traditional or Roth account aligns with your tax situation can reduce your after‑tax wealth.

- Not Rebalancing: As markets move, your portfolio can drift away from your intended risk profile. Annual rebalancing keeps you on track.

Quick Checklist for How to Get a Retirement Account

- Determine eligibility and contribution limits.

- Pick the appropriate account type (401(k), IRA, etc.).

- Select a reputable provider with low fees.

- Complete the application and link a funding source.

- Set up automatic contributions.

- Choose diversified investments or a target‑date fund.

- Review annually and adjust as needed.

Following this checklist transforms the often‑daunting question of how to get a retirement account into a series of manageable steps. Consistency, low fees, and smart investment choices are the three pillars that will carry your nest egg forward.

In the end, the journey of building a retirement account is less about a single decision and more about a series of disciplined actions. By taking the time now to understand the options, set up contributions, and stay engaged with your investments, you’ll be well on your way to a comfortable, financially independent retirement. So, roll up your sleeves, follow the steps, and watch your future self thank you.