Table of Contents

- Understanding the Role of Business Loans 3 Month Bank Statements in the Application Process

- Preparing Business Loans 3 Month Bank Statements for Maximum Impact

- Common Mistakes to Avoid When Submitting Business Loans 3 Month Bank Statements

- How to Leverage Other Financial Documents Alongside Business Loans 3 Month Bank Statements

- Profit and Loss Statements (P&L)

- Tax Returns

- Accounts Receivable Aging Report

- Choosing the Right Lender for Business Loans 3 Month Bank Statements Applications

- Traditional Banks

- Online Lenders

- Credit Unions and Community Banks

- Tips to Speed Up Approval When Using Business Loans 3 Month Bank Statements

- Organize Digitally Before Submitting

- Provide a Cover Letter

- Pre‑emptively Answer Common Questions

- Leverage Existing Relationships

- Real‑World Example: Turning a 3‑Month Snapshot Into a $50,000 Loan

- Additional Resources to Strengthen Your Application

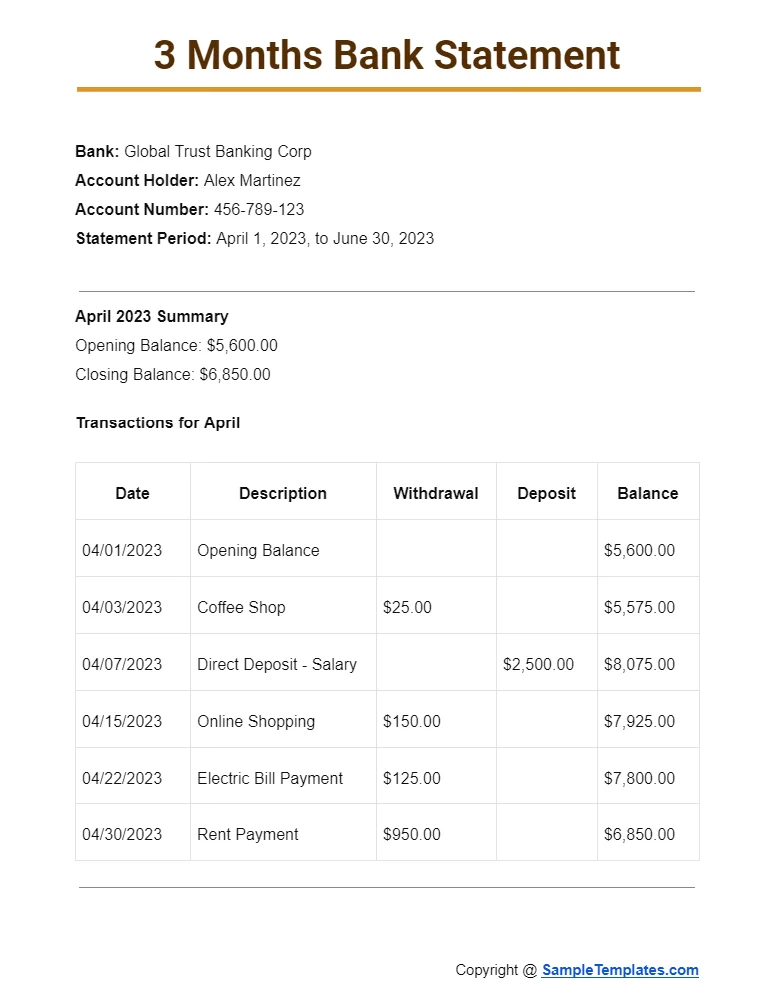

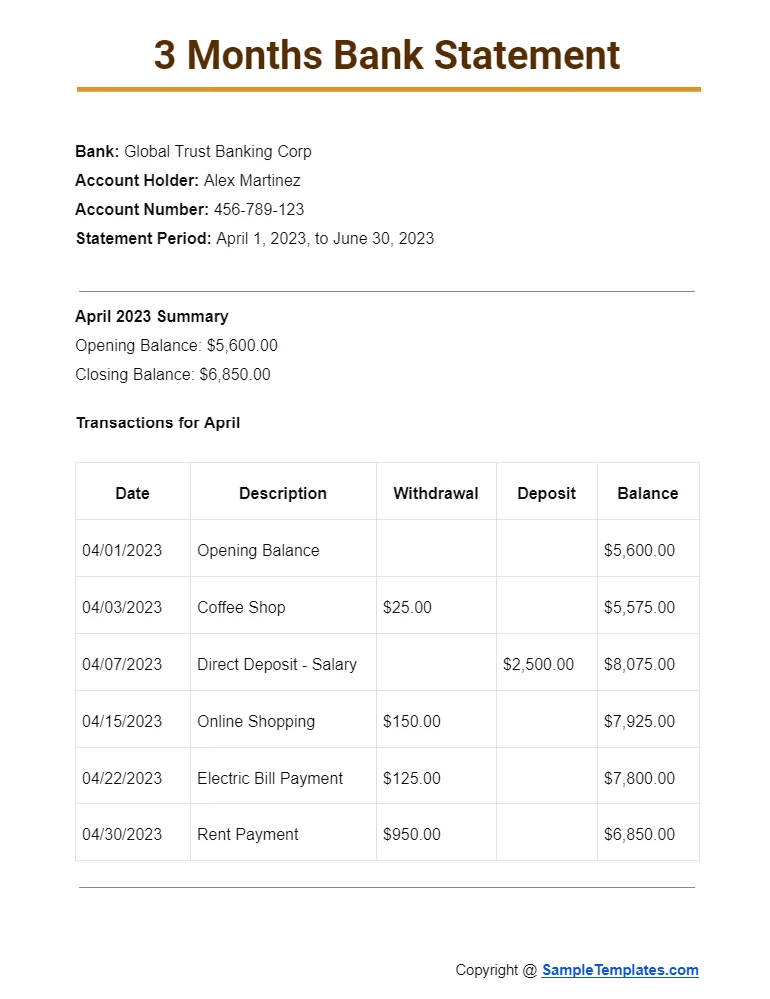

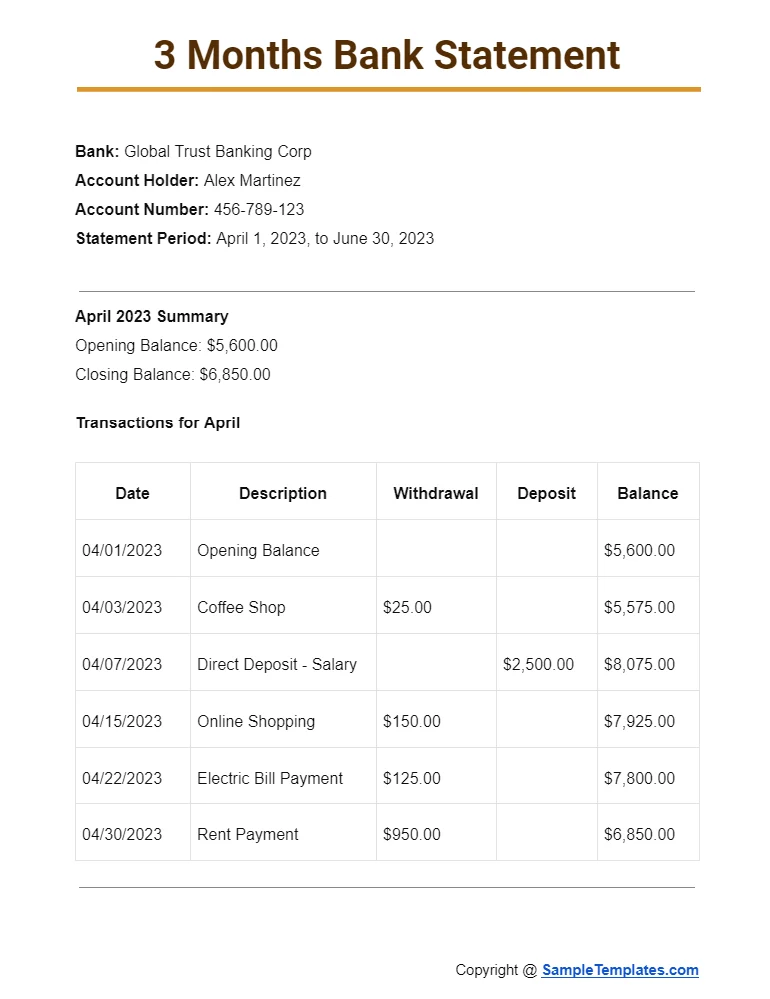

Getting a loan for your business can feel like navigating a maze, especially when lenders ask for a mountain of paperwork. One common request that often trips up entrepreneurs is the need to provide three months of bank statements. If you’re wondering how to turn a simple “business loans 3 month bank statements” requirement into a smooth, stress‑free step, you’ve landed in the right spot.

In this article we’ll break down why lenders focus on the most recent three months, how you can present those statements to look their best, and what extra pieces of the puzzle you might need. Whether you’re a brand‑new startup or a seasoned company looking to expand, the tactics below will help you make the most of those three months of data.

Before we dive in, keep in mind that the quality of your bank statements often matters more than the sheer volume of documents. A clean, well‑organized three‑month snapshot can sometimes outweigh a longer, messier history. Let’s explore how to make those three months work for you.

Understanding the Role of Business Loans 3 Month Bank Statements in the Application Process

Lenders use the “business loans 3 month bank statements” request as a quick health check. They’re looking for cash flow trends, seasonality, and any red flags that might indicate risk. By focusing on the most recent quarter, banks can gauge how your business is performing right now, rather than getting lost in historical data that may no longer reflect reality.

Here are the core reasons why the three‑month window is so popular:

- Current Cash Flow Visibility: Recent statements show the actual inflow and outflow of cash, helping lenders assess whether you can meet repayment schedules.

- Seasonal Patterns: If your business is seasonal, lenders can spot peaks and troughs and adjust loan terms accordingly.

- Risk Management: A short, recent snapshot reduces the chance of outdated or irrelevant information skewing the decision.

- Efficiency: It speeds up the underwriting process, which is a win for both borrower and lender.

Preparing Business Loans 3 Month Bank Statements for Maximum Impact

Now that you know why lenders care, let’s talk preparation. A few strategic moves can turn a plain set of PDFs into a compelling financial story.

- Clean Up the Numbers: Remove any non‑business transactions if you use a personal account for business purposes. If that’s not possible, be ready to explain each personal expense.

- Highlight Consistency: Use simple annotations or a separate summary page to point out regular revenue streams—like recurring client payments.

- Show Seasonality: If you have a high‑season period, add a short note explaining the dip or surge, so lenders understand it’s not a red flag.

- Provide Context: Attach a brief narrative (one page max) that ties the numbers to real‑world events—new contracts, marketing campaigns, or supply chain changes.

Common Mistakes to Avoid When Submitting Business Loans 3 Month Bank Statements

Even a well‑prepared set of statements can be derailed by simple oversights. Watch out for these pitfalls:

- Submitting statements that are not in chronological order, making it hard for the underwriter to follow the cash flow trend.

- Leaving large, unexplained deposits or withdrawals—these raise red flags and can delay approval.

- Using PDFs that are blurry or password‑protected, which forces the lender to request a clearer copy.

- Failing to match the statements with other financial documents, like profit‑and‑loss statements, creating inconsistencies.

How to Leverage Other Financial Documents Alongside Business Loans 3 Month Bank Statements

While the three‑month statements are the centerpiece, they don’t exist in a vacuum. Pairing them with complementary documents can strengthen your case dramatically.

Profit and Loss Statements (P&L)

A P&L provides a broader view of revenue, expenses, and profitability over a longer period. When you attach a P&L that aligns with the three‑month bank data, lenders see consistency and gain confidence in your financial management.

Tax Returns

Recent tax filings (usually the last two years) demonstrate compliance and provide a verified baseline of income. Even if you’re only providing three months of statements, a solid tax history can reassure lenders that your business is stable.

Accounts Receivable Aging Report

If a sizable portion of your cash flow is tied up in receivables, an aging report clarifies when you expect those funds to hit the bank. This helps lenders differentiate between “cash on hand” and “cash that’s coming soon.”

Choosing the Right Lender for Business Loans 3 Month Bank Statements Applications

Not every lender treats the three‑month requirement the same way. Some are more flexible, while others may ask for additional proof. Here’s a quick guide to matching your business profile with the right financing partner.

Traditional Banks

Traditional banks often have stricter underwriting criteria, but they also offer lower interest rates. If your three‑month statements show steady cash flow and you have a solid credit history, a bank could be a good fit.

Online Lenders

Online lenders tend to be more flexible with documentation. Many will accept a simple “business loans 3 month bank statements” packet plus a brief narrative. However, expect higher rates compared to banks.

Credit Unions and Community Banks

These institutions often blend the best of both worlds: competitive rates and a more personalized approach. They may be willing to overlook minor inconsistencies if you have a strong local reputation.

Tips to Speed Up Approval When Using Business Loans 3 Month Bank Statements

Speed matters, especially if you need funds for inventory, payroll, or a time‑sensitive opportunity. Follow these proven tactics to keep the process moving.

Organize Digitally Before Submitting

Convert all statements to high‑resolution PDFs, label them clearly (e.g., “Bank Statement – Jan 2024”), and combine them into a single file. A tidy digital package reduces back‑and‑forth emails.

Provide a Cover Letter

A short cover letter (one page) summarizing the key points of your three‑month cash flow can guide the underwriter’s eye to the most relevant information.

Pre‑emptively Answer Common Questions

Include a FAQ section at the end of your submission that addresses likely concerns, such as “Why is there a large deposit on 15 Feb 2024?” or “What caused the dip in March?” This shows you’re proactive and transparent.

Leverage Existing Relationships

If you already have a banking relationship, ask your account manager to flag your loan application. A familiar face can accelerate review times.

Real‑World Example: Turning a 3‑Month Snapshot Into a $50,000 Loan

Let’s walk through a hypothetical scenario. Jane runs a boutique coffee roastery. She needs $50,000 to upgrade her espresso machines. Her bank statements for the last three months look like this:

- January: $18,500 net cash flow (steady sales, small marketing spend)

- February: $20,300 net cash flow (new corporate contract secured)

- March: $22,100 net cash flow (seasonal uptick for spring events)

By pairing these statements with a concise P&L, a two‑year tax return, and a one‑page narrative explaining the new contract and seasonal trend, Jane presented a clear story of growth. An online lender, impressed by the upward trajectory and the documented contract, approved her loan within 48 hours at a 9% APR.

Additional Resources to Strengthen Your Application

Beyond polishing your three‑month statements, there are other tools that can make your financing journey easier. For instance, setting up a dedicated business bank account not only separates personal and business finances but also streamlines the statement‑gathering process. Check out our guide on how to open a free business bank account – a complete guide for step‑by‑step instructions.

If you’re interested in managing your finances digitally, our article on online banking for small business owners – a complete guide explains the benefits of using modern banking platforms, which can also simplify the submission of those essential three‑month statements.

For LLC owners who need a separate account, see online business bank account for LLC – a complete guide. A dedicated account ensures that every transaction that appears on your statements is purely business‑related, removing any ambiguity for lenders reviewing your “business loans 3 month bank statements”.

Remember, the goal isn’t just to hand over three months of numbers; it’s to tell a compelling financial story that convinces lenders you’re a low‑risk borrower with a clear repayment plan.

By following the strategies outlined above—cleaning up your statements, adding context, pairing with complementary documents, and choosing the right lender—you’ll turn that three‑month snapshot into a powerful asset that opens doors to the capital you need.

Good luck, and may your next loan be approved faster than you imagined!