Table of Contents

- Why the “Easiest Bank to Open a Business Account” Matters for New Entrepreneurs

- Key Features of the Easiest Bank to Open a Business Account

- Simple Application Process

- Low or No Minimum Balance Requirements

- Transparent Fees

- Robust Digital Banking Suite

- Customer Support That Actually Helps

- Top Contenders for the Easiest Bank to Open a Business Account in 2024

- 1. Novo – The True Online Champion

- 2. Axos Bank – High‑Tech, Low‑Hassle

- 3. Mercury – Startup‑Friendly and Investor‑Ready

- 4. Lili – Ideal for Freelancers and Solo‑Proprietors

- 5. Chase – Traditional Power with an Online Edge

- Step‑by‑Step Guide to Open the Easiest Bank to Open a Business Account

- Common Pitfalls and How to Avoid Them

- Missing Documentation

- Overlooking State‑Specific Requirements

- Ignoring Fee Structures

- Beyond the Account: Value‑Added Services That Make a Difference

- Final Thoughts on Picking the Easiest Bank to Open a Business Account

Starting a new venture is exciting, but the paperwork that comes with it can feel like a hurdle. One of the first practical steps for any entrepreneur is setting up a business bank account. While the task sounds straightforward, the reality is that not every bank makes the process painless. Some ask for a mountain of documentation, a lengthy in‑person interview, or high minimum balances that can strain a fledgling cash flow.

If you’ve ever wondered which institution truly offers the “easiest bank to open a business account,” you’re not alone. In this article we’ll break down the criteria that make an account opening experience smooth, walk you through the top contenders, and share insider tips to shave minutes—if not hours—off the setup time. By the end, you’ll have a clear roadmap to get your business finances up and running without unnecessary drama.

Whether you run a solo freelance operation, a boutique e‑commerce shop, or a growing startup, the right banking partner can save you time, reduce fees, and even provide tools that help you manage cash flow better. Let’s dive in and see which banks truly earn the title of the easiest bank to open a business account.

Why the “Easiest Bank to Open a Business Account” Matters for New Entrepreneurs

Choosing the easiest bank to open a business account isn’t just about convenience; it directly impacts your ability to focus on what matters most—building your product or service. Here’s why a frictionless onboarding process is a game‑changer:

- Speed to market: The faster you can access a business checking account, the sooner you can start accepting payments, paying vendors, and tracking expenses.

- Cash flow clarity: Early access to online banking tools and real‑time transaction alerts helps you keep a tight grip on cash flow from day one.

- Cost savings: Banks that eliminate hidden fees or minimum balance requirements let you keep more capital in the business.

- Future scalability: A bank that offers seamless upgrades—like merchant services or credit lines—makes growth less painful.

Now that we understand the stakes, let’s look at the features that define the easiest bank to open a business account.

Key Features of the Easiest Bank to Open a Business Account

When evaluating potential banks, keep an eye on these essential attributes. They’re the hallmarks of a streamlined onboarding experience.

Simple Application Process

Ideally, the easiest bank to open a business account provides a short, intuitive online form that can be completed in under 15 minutes. No need for a physical branch visit unless you specifically want one. Look for banks that accept digital copies of your formation documents (e.g., Articles of Incorporation) and an EIN.

Low or No Minimum Balance Requirements

Many traditional banks demand a minimum opening deposit or a monthly balance to avoid fees. The easiest bank to open a business account often waives these requirements, allowing you to start with as little as $0.

Transparent Fees

Hidden fees can quickly eat into a startup’s budget. A good bank will list all costs—monthly maintenance, transaction fees, wire fees—up front. Some even offer free business checking for the first year.

Robust Digital Banking Suite

From mobile check deposit to real‑time alerts, a solid online platform is non‑negotiable. The easiest bank to open a business account typically integrates with popular accounting software like QuickBooks or Xero, reducing manual data entry.

Customer Support That Actually Helps

When you hit a snag, responsive chat or phone support can make all the difference. Look for banks with dedicated small‑business support teams rather than generic call centers.

Top Contenders for the Easiest Bank to Open a Business Account in 2024

Based on the criteria above, here are the banks that consistently rank as the easiest bank to open a business account. Each offers a unique blend of speed, simplicity, and value.

1. Novo – The True Online Champion

Novo’s entire business banking experience is built for the digital age. The application takes under 10 minutes, requires only an EIN and personal ID, and there’s no minimum balance. Their fee structure is crystal clear: no monthly fees, no transaction fees, and free ACH transfers. What really sets Novo apart is its seamless integration with tools like Stripe, PayPal, and accounting platforms—perfect for e‑commerce entrepreneurs.

2. Axos Bank – High‑Tech, Low‑Hassle

Axos offers a Business Checking account with a $0 opening deposit and no monthly maintenance fee if you maintain an average balance of $1,000 (or you can opt for a fee‑free version). Their mobile app is robust, supporting remote check deposit, bill pay, and even a line of credit that can be activated with a few clicks. The online application is straightforward, and most accounts are approved within a day.

3. Mercury – Startup‑Friendly and Investor‑Ready

Mercury targets tech‑savvy startups and has quickly become known as the easiest bank to open a business account for high‑growth companies. They require just your company’s legal name, EIN, and a personal ID. No minimum balance, no monthly fees, and a sleek dashboard that integrates with platforms like Gusto and Plaid. Their “cash management” tools, including virtual cards and API access, make them a favorite among fintech founders.

4. Lili – Ideal for Freelancers and Solo‑Proprietors

If you’re a solo‑proprietor, Lili offers a business checking account that feels more like a personal finance app. The sign‑up process is almost instantaneous, and the platform automatically categorizes expenses, tracks mileage, and helps you set aside tax money. There’s no minimum balance, and the free tier includes unlimited transactions.

5. Chase – Traditional Power with an Online Edge

While Chase is a big‑bank name, its “Chase Business Complete Banking” account has been streamlined for speed. The online application can be completed in minutes, and you can often open the account without stepping into a branch. The catch? There is a $15 monthly fee (waived with a $2,000 daily balance). For entrepreneurs who value a nationwide branch network, Chase remains a solid option.

If you want to compare more options, check out this Easiest Business Bank Account to Open Online – Your Quick Guide for a side‑by‑side look at features and fees.

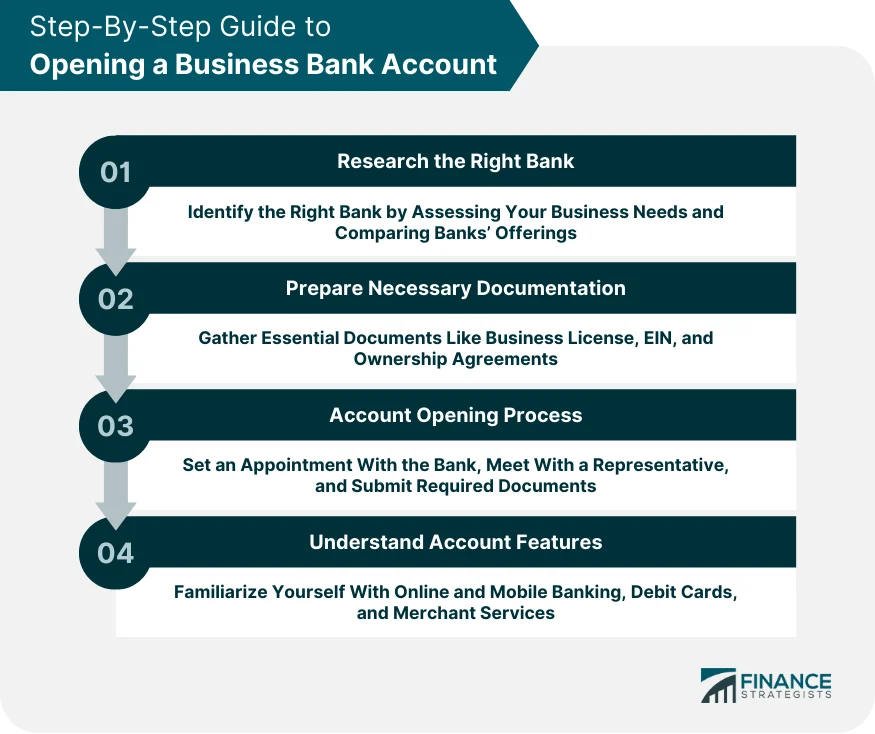

Step‑by‑Step Guide to Open the Easiest Bank to Open a Business Account

Even the simplest bank will require a few pieces of information. Follow this checklist to keep the process smooth:

- Gather your documents: EIN, Articles of Incorporation or Organization, personal ID (driver’s license or passport), and proof of address.

- Choose the right account type: Checking vs. savings, merchant services, and any additional features you may need.

- Complete the online application: Fill out the form, upload digital copies, and double‑check for typos.

- Fund the account: Even if there’s no minimum, a small initial deposit (e.g., $1) can speed up verification.

- Set up online banking: Link to your accounting software, order debit cards, and configure alerts.

Most banks will email you a welcome packet with instructions for setting up two‑factor authentication and linking external accounts. Within a day or two, you’ll be ready to receive payments, pay vendors, and start tracking your finances.

Common Pitfalls and How to Avoid Them

Even when you choose the easiest bank to open a business account, there are a few traps that can slow you down:

Missing Documentation

Make sure you have the correct EIN and that the name on your formation documents matches the name you’re using to apply. A mismatch can cause the bank to request additional paperwork, adding days to the process.

Overlooking State‑Specific Requirements

Some states require additional licenses for certain business types (e.g., cannabis, firearms). Verify that the bank you choose accepts businesses in your industry and location.

Ignoring Fee Structures

Even “free” accounts may charge for certain services like wire transfers or cash deposits. Read the fine print and compare against your anticipated transaction volume.

For a deeper dive into fee structures and free business checking options, you might find this article helpful: Does Wells Fargo Bank Have Free Checking? – Full Review & Details.

Beyond the Account: Value‑Added Services That Make a Difference

Opening the easiest bank to open a business account is just the first step. Look for banks that bundle extra services you’ll need as you grow:

- Merchant Services: Integrated payment processing for credit cards and online payments.

- Business Credit Cards: Reward programs and expense tracking features.

- Line of Credit: Easy access to capital without a full loan application.

- Payroll Integration: Direct sync with payroll platforms like Gusto or ADP.

Mercury, for instance, offers virtual cards and API access that let developers automate expense approvals—a perk that can be a huge time‑saver for tech‑focused firms.

Final Thoughts on Picking the Easiest Bank to Open a Business Account

There’s no one‑size‑fits‑all answer, but the pattern is clear: the easiest bank to open a business account usually lives online, has minimal paperwork, no hidden fees, and a user‑friendly digital platform. Novo, Axos, Mercury, Lili, and even the streamlined version of Chase all fit this mold in slightly different ways, catering to various business sizes and industries.

Take a moment to list your top priorities—whether it’s zero fees, instant online access, or integration with your favorite accounting tool—and match them against the features we’ve outlined. The right fit will let you focus on growing revenue instead of wrestling with paperwork.

Remember, the banking relationship you start today can evolve with your business. Choose a partner that not only offers the easiest onboarding but also provides the tools and support you’ll need tomorrow.