Table of Contents

- What Is a US Bank Balance Transfer Credit Card?

- Key Features of a US Bank Balance Transfer Credit Card

- How the Balance Transfer Process Works

- When a US Bank Balance Transfer Credit Card Makes Sense

- Hidden Costs and Pitfalls

- Tips for Maximizing Your US Bank Balance Transfer Credit Card

- Choosing the Right US Bank Balance Transfer Credit Card

- Real‑World Example: Calculating Savings

- Common FAQs About US Bank Balance Transfer Credit Cards

- Can I transfer more than one balance?

- What happens if I exceed my credit limit after the transfer?

- Do balance transfers affect my credit score?

- Is there a limit on how much I can transfer?

- Strategic Uses Beyond Debt Consolidation

- Final Thoughts on Using a US Bank Balance Transfer Credit Card

When you’re juggling multiple credit‑card balances, the idea of moving debt to a single card with a lower interest rate can feel like a lifesaver. In the United States, banks have refined the art of the balance‑transfer credit card, offering promotional APRs that can shrink monthly payments and accelerate debt payoff. But not every offer is created equal, and understanding the nuances of a us bank balance transfer credit card is crucial before you hit “accept.”

This article unpacks the mechanics behind these cards, walks you through the hidden costs, and provides practical tips to ensure you actually save money—not just chase a promotional rate that disappears before you’re ready. Whether you’re a seasoned credit‑card user or new to the concept of balance transfers, you’ll walk away with a clearer roadmap for using a us bank balance transfer credit card to your advantage.

What Is a US Bank Balance Transfer Credit Card?

A us bank balance transfer credit card is a type of credit card that allows you to move existing credit‑card balances—or sometimes other types of debt—onto a new account that typically offers a 0% introductory APR for a set period, often ranging from 12 to 21 months. During this promotional window, you won’t pay interest on the transferred amount, which can dramatically reduce the total cost of your debt if you stay disciplined.

Most US banks, including big names like Chase, Citi, and Discover, market these cards as “debt‑relief tools.” The allure is simple: you transfer a high‑interest balance (say, 18% APR) to a card with a 0% introductory rate, pay down the principal faster, and avoid the compounding interest that would otherwise eat away at your payments.

Key Features of a US Bank Balance Transfer Credit Card

- Introductory APR: Usually 0% for a limited period (12‑21 months).

- Balance Transfer Fee: Typically 3%–5% of the transferred amount; some cards waive the fee for balances over a certain threshold.

- Credit Limit: Determined by your credit score and income; higher limits give you more flexibility.

- Post‑Promo APR: After the intro period, rates can jump to 15%–25% or higher.

- Rewards & Perks: Some cards still offer cash back or points on new purchases, even while you’re focusing on the transfer.

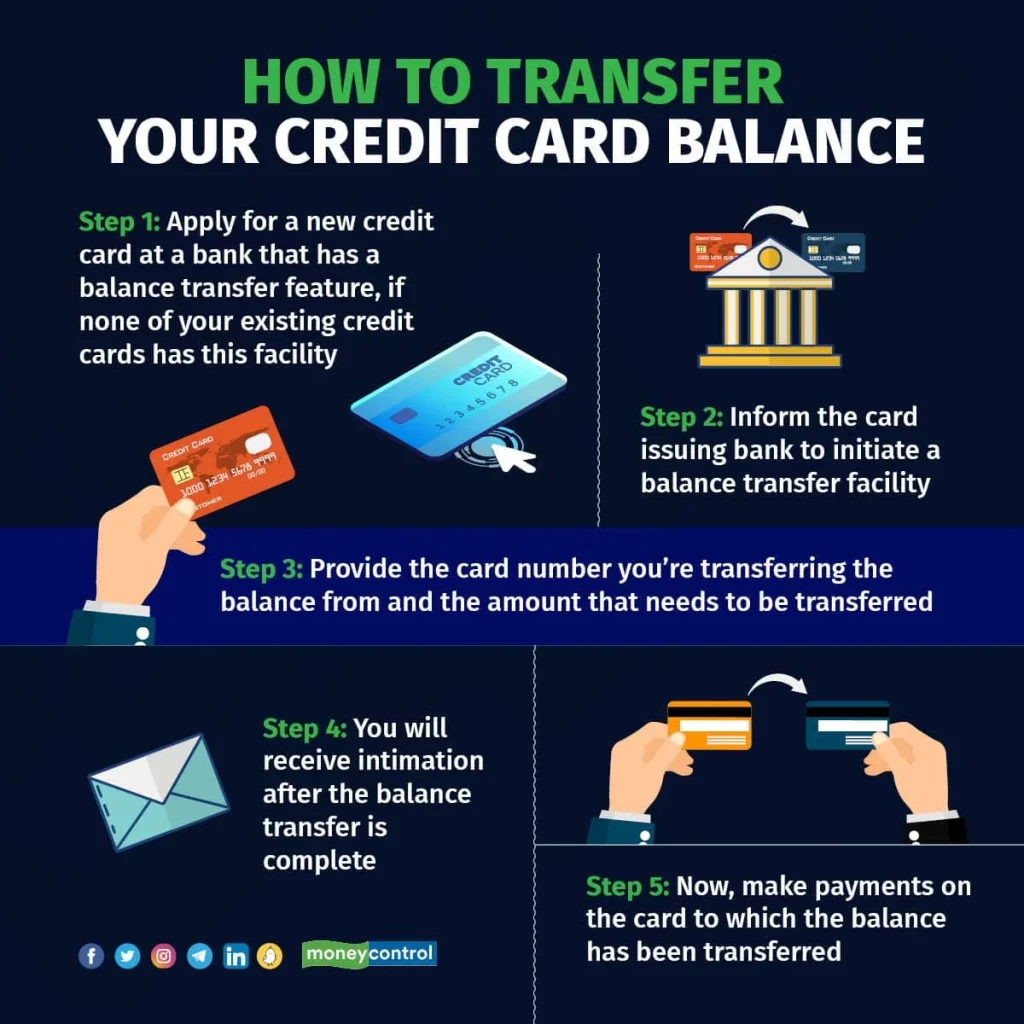

How the Balance Transfer Process Works

First, you apply for a us bank balance transfer credit card. Once approved, you’ll receive a balance‑transfer checklist that includes the account numbers of the debts you want to move. You can typically initiate the transfer online, by phone, or via a paper form. The bank then pays the existing creditor directly, and the balance appears on your new card.

It’s important to keep the original account open—at least until the transfer is confirmed—so you don’t risk a missed payment that could hurt your credit. After the transfer, you’ll receive a new statement showing the transferred balance, the fee, and the remaining days of the intro APR.

When a US Bank Balance Transfer Credit Card Makes Sense

Not every debt situation benefits from a balance transfer. Here are scenarios where a us bank balance transfer credit card shines:

- High‑Interest Debt: If you’re paying 18%+ on existing cards, a 0% intro rate can save you hundreds in interest.

- Predictable Payoff Timeline: You have a clear plan to pay off the transferred amount before the promo ends.

- Stable Credit Score: A strong score helps you qualify for a higher credit limit and better terms.

- Limited New Purchases: You can avoid adding new balances that could erode the benefits.

Hidden Costs and Pitfalls

While the promise of “no interest” sounds like a free ride, the reality includes several costs you need to watch out for. The most common trap is the balance‑transfer fee. For example, moving a $5,000 balance with a 3% fee costs $150—still worthwhile if you’d otherwise pay $400+ in interest over a year, but you need to calculate it.

Another pitfall is missing a payment. Most us bank balance transfer credit cards reset the intro APR if you’re 30 days late, turning your 0% rate into the standard, higher APR instantly. Also, after the introductory period, any remaining balance will be subject to the post‑promo rate, which can be steep.

Tips for Maximizing Your US Bank Balance Transfer Credit Card

- Do the math: Use a balance‑transfer calculator to compare interest saved versus fees.

- Set up automatic payments: Guarantees you never miss a due date, preserving the intro rate.

- Pay more than the minimum: Accelerates payoff and reduces the risk of carrying a balance into the higher APR phase.

- Avoid new purchases: If you must buy, use a separate card to keep the transferred balance untouched.

- Watch the deadline: Mark the exact day the promo ends and plan a final push to clear the balance.

Choosing the Right US Bank Balance Transfer Credit Card

Not all cards are equal, and the best fit depends on your financial situation. Here’s a quick checklist:

- Length of Intro Period: Longer is better if you need more time to pay down debt.

- Transfer Fee Structure: Some cards offer 0% fees for balances over $10,000—great for larger debts.

- Credit Score Requirement: Premium cards may demand 700+ scores.

- Additional Benefits: Look for travel insurance, purchase protection, or cash‑back rewards that complement your lifestyle.

For a deeper dive into opening the right kind of bank account to support your financial moves, check out our guide on the easiest bank to open a business account. While it focuses on business banking, many of the same principles—like evaluating fees and credit limits—apply to personal balance‑transfer cards.

Real‑World Example: Calculating Savings

Imagine you owe $8,000 on a credit card with a 20% APR. Your monthly payment is $200, but most of that goes toward interest. If you transfer the balance to a us bank balance transfer credit card with a 0% intro rate for 18 months and a 3% fee, here’s how the numbers break down:

- Transfer fee: 3% of $8,000 = $240.

- Total cost with transfer: $8,240 (principal + fee).

- Monthly payment needed to clear in 18 months: $8,240 ÷ 18 ≈ $458.

- Interest saved: At 20% APR, you’d pay roughly $1,200 in interest over 18 months on the original card. With the transfer, you pay $0 interest.

Even after the $240 fee, you save about $960 in interest—an impressive win if you can afford the higher monthly payment.

Common FAQs About US Bank Balance Transfer Credit Cards

Can I transfer more than one balance?

Yes. Most us bank balance transfer credit cards let you move multiple balances, as long as you stay within your credit limit.

What happens if I exceed my credit limit after the transfer?

Exceeding the limit can trigger over‑limit fees and may lead the issuer to raise your APR. It’s best to keep the transferred amount well below the limit.

Do balance transfers affect my credit score?

Initially, the hard inquiry can dip your score by a few points. However, if you keep utilization low and pay on time, the overall effect can be positive.

Is there a limit on how much I can transfer?

Each card sets its own limit, often 3‑5 times your existing credit line, but it’s ultimately capped by the credit limit you receive.

Strategic Uses Beyond Debt Consolidation

While the primary goal is debt relief, a us bank balance transfer credit card can also serve other strategic purposes. For instance, some borrowers use the 0% period to free up cash flow for investments or emergency savings. Others leverage the card’s rewards program for everyday purchases while keeping the transferred balance untouched.

If you’re a small business owner, consider how a personal balance‑transfer card might complement a business bank account. A lower personal debt load can improve your personal credit profile, which in turn may help you secure better financing terms for your business.

Final Thoughts on Using a US Bank Balance Transfer Credit Card

Choosing the right us bank balance transfer credit card is a balancing act—pun intended—between promotional benefits, fees, and your ability to commit to a disciplined repayment plan. By understanding the mechanics, calculating true savings, and avoiding common pitfalls, you can turn a high‑interest debt mountain into a manageable hill.

Remember, the power of a balance‑transfer card lies in the discipline to pay down the balance before the promotional period expires. Set up automatic payments, keep a close eye on your statement, and avoid the temptation to rack up new debt. With a clear strategy, a us bank balance transfer credit card can be a powerful tool in your financial toolkit, helping you regain control and move toward a debt‑free future.