Getrawbox Getrawbox

Getrawbox Getrawbox

Related Articles

Running a business means juggling cash flow, expenses, and the ever‑present need for flexible financing. One tool that can streamline spending while keeping personal assets safe is a corporate credit card that doesn’t require a personal guarantee. Unlike traditional business cards, these cards let the company stand on its own creditworthiness, sparing owners from risking their personal credit scores.

But how realistic is it to find a corporate credit card without personal guarantee? What are the hidden costs, eligibility criteria, and real‑world benefits? In this article we’ll break down the landscape, compare the major players, and give you a practical roadmap to secure the right card for your organization—no personal guarantee needed.

Whether you’re a startup founder, a seasoned CFO, or an entrepreneur looking to separate personal and business finances, understanding the nuances of a no‑guarantee corporate card can be a game‑changer. Let’s dive into the why, what, and how, and finish with a few actionable tips you can put into practice right away.

What Is a Corporate Credit Card Without Personal Guarantee?

A corporate credit card without personal guarantee is a revolving credit line issued directly to a business entity. The issuing bank or financial institution evaluates the company’s credit profile—revenue history, cash flow, industry risk, and existing debt—rather than the personal credit of its owners or executives. In essence, the company alone is liable for the balances and any defaults.

Why does this matter? Because it protects the personal credit scores of founders, limits personal liability in lawsuits, and often simplifies bookkeeping: all expenses flow through a single, business‑only account.

Key Features of a Corporate Credit Card Without Personal Guarantee

- Company‑Only Liability: The legal responsibility rests with the corporation or LLC, not the individual.

- Higher Credit Limits: Limits are based on business cash flow and revenue, potentially far exceeding personal cards.

- Expense Management Tools: Integrated software for receipt capture, spend categorization, and real‑time reporting.

- Rewards Tailored to Business Needs: Travel points, cash back on office supplies, or industry‑specific perks.

- Enhanced Controls: Ability to set per‑employee limits, restrict merchant categories, and enforce policy compliance.

Who Can Qualify for a Corporate Credit Card Without Personal Guarantee?

The biggest hurdle is proving that the business itself is creditworthy. While the exact criteria vary by issuer, most banks look for:

- Annual Revenue: Typically $500,000 or more, though some issuers accept lower figures if cash flow is strong.

- Operating History: At least 12‑24 months of consistent financial statements.

- Profitability or Positive Cash Flow: Demonstrated ability to meet recurring obligations.

- Business Credit Score: A Dun & Bradstreet PAYDEX score of 70+ or an Experian Business Credit Rating of “B” or higher.

- Industry Risk Profile: Low‑risk sectors (professional services, SaaS, manufacturing) are favored over high‑risk ones (construction, hospitality).

If your company checks most of these boxes, you’re in a good position to apply. For newer startups that don’t yet meet the thresholds, consider building business credit through vendor lines, a secured business credit card, or a traditional corporate card that does require a personal guarantee as a stepping stone.

Top Issuers Offering Corporate Credit Cards Without Personal Guarantee

Not every bank offers a no‑guarantee corporate card, but a few major players have entered the market to attract high‑growth businesses.

American Express Business Platinum Card

While technically a personal guarantee is still part of the application, large corporations can negotiate a “corporate guarantee” model where the company’s credit replaces the personal guarantee. The card shines with travel perks, 5X points on airfare, and a suite of expense‑management tools.

Capital One Spark Cash for Business

Capital One offers a corporate version that can be structured without a personal guarantee for firms with solid business credit. The flat‑rate 2% cash back on all purchases is attractive for companies that spend heavily on supplies and advertising.

Bank of America Business Advantage Travel Rewards Card

For companies that travel frequently, this card provides 1.5 points per dollar on all purchases, plus a suite of travel‑related benefits. The bank will consider a corporate guarantee instead of a personal one for eligible businesses.

Wells Fargo Business Elite Signature Card

Wells Fargo’s “Corporate Credit Card without Personal Guarantee” program is tailored for midsize firms with annual revenues above $1 million. It includes robust reporting, employee card controls, and the ability to earn points redeemable for travel or statement credits.

How to Apply for a Corporate Credit Card Without Personal Guarantee

The application process mirrors that of a standard business loan: you’ll need to submit financial statements, tax returns, and a detailed business plan. Below is a step‑by‑step roadmap to keep you on track.

Step 1: Gather Your Financial Documentation

- Last two years of audited or reviewed financial statements.

- Quarterly profit & loss statements for the most recent year.

- Bank statements showing cash flow trends.

- Business credit reports from Dun & Bradstreet or Experian.

Step 2: Choose the Right Issuer

Match your spending patterns with the card’s rewards structure. If you’re unsure, read related guides like Business Bank Account with Lowest Fees: Complete Guide to understand how banking costs affect your overall financial health.

Step 3: Submit the Application

Most banks now offer an online portal where you can upload documents and track status. Be prepared to answer questions about revenue projections, major contracts, and your company’s credit policies.

Step 4: Negotiate Terms (If Possible)

Some issuers are flexible on interest rates, annual fees, and the exact nature of the guarantee. If your business has a strong credit profile, ask for a lower APR or a waived annual fee.

Step 5: Activate and Set Up Controls

Once approved, configure employee spending limits, merchant category blocks, and integrate the card with your accounting software (e.g., QuickBooks, Xero). This ensures real‑time visibility and reduces the risk of unauthorized expenses.

Benefits of Going Card‑Only (No Personal Guarantee)

Choosing a corporate credit card without personal guarantee isn’t just about protecting personal credit—it also brings tangible operational advantages.

- Risk Mitigation: Your personal credit score stays untouched, preserving borrowing power for future personal needs.

- Clear Financial Separation: Audits become straightforward when all expenses run through a single corporate account.

- Improved Cash Management: Many cards offer extended payment terms (up to 60 days), giving you breathing room to manage cash flow.

- Enhanced Employee Accountability: Detailed transaction logs make it easy to enforce expense policies.

- Potential Tax Advantages: Business‑only interest and fees may be deductible as ordinary business expenses.

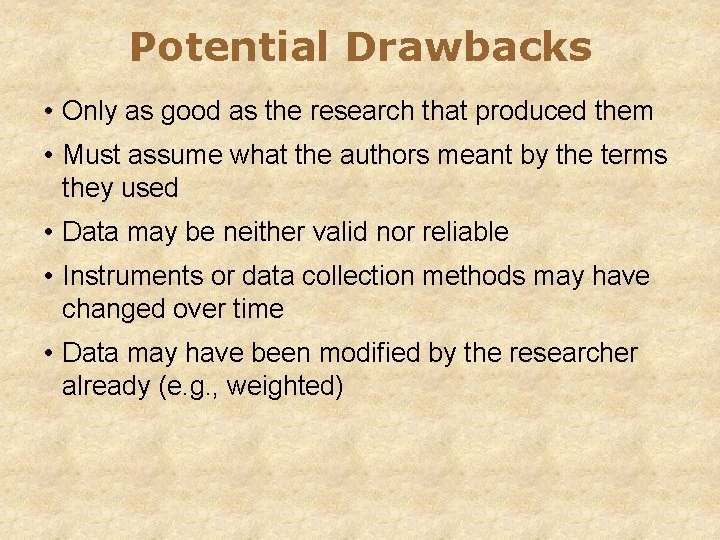

Potential Drawbacks and How to Address Them

No product is perfect. While a no‑guarantee corporate card reduces personal exposure, it can come with higher interest rates or stricter approval standards. Here’s how to navigate common challenges:

Higher APRs

If the issuer perceives higher risk, the APR may be above the average personal card rate. Mitigate this by paying the balance in full each month, or by negotiating a lower rate if you can demonstrate strong cash flow.

Limited Issuer Options

Only a handful of banks currently offer true no‑guarantee corporate cards. If you don’t qualify, consider a secured business credit card as a bridge. The Business Bank Accounts with No Credit Check – A Complete Guide can also help you establish a credit line without a personal guarantee.

Stringent Reporting Requirements

Many issuers require monthly spend reports and compliance checks. Use integrated expense‑management platforms to automate reporting and stay on the safe side of policy.

Comparing No‑Guarantee Corporate Cards to Traditional Alternatives

To put things into perspective, let’s compare a no‑guarantee corporate card with two common alternatives: a personal guarantee corporate card and a small business loan.

| Feature | No‑Guarantee Corporate Card | Corporate Card with Personal Guarantee | Small Business Loan |

|---|---|---|---|

| Liability | Company only | Owner(s) personally liable | Company (sometimes personal guarantee) |

| Credit Limit | Based on business cash flow | Often higher due to personal guarantee | Fixed amount, amortized |

| Interest | Variable, often higher | Variable, lower if strong personal credit | Fixed or variable, usually lower than credit cards |

| Rewards | Business‑focused (travel, office spend) | Similar, but may be limited | None |

| Application Time | Weeks (due to credit review) | Days to weeks | Weeks to months |

As the table shows, the no‑guarantee option excels in protecting personal assets and providing business‑centric rewards, but it may carry a higher cost of capital.

Tips for Maximizing the Value of Your Corporate Credit Card Without Personal Guarantee

Getting the card is just the first step. To truly reap the benefits, adopt these best practices.

Integrate with Your Accounting System

Sync the card feed with tools like QuickBooks, Xero, or NetSuite. This reduces manual entry, catches duplicate charges, and makes expense reconciliation a breeze.

Leverage Reward Categories

Identify the top spend categories for your business—travel, advertising, supplies—and align them with the card’s highest‑earning rewards. For example, use a card that offers 5X points on airfare if you have a sales team that travels frequently.

Set Employee Spending Policies

Use the card’s control features to set per‑employee limits, restrict high‑risk merchants, and require receipt uploads. This not only prevents fraud but also simplifies audit trails.

Pay the Balance in Full When Possible

Avoid interest charges by paying the statement balance each month. If cash flow is tight, prioritize high‑interest balances and aim to keep utilization below 30% to protect the company’s credit score.

Review Statements Monthly

Schedule a recurring meeting with your finance team to go over the card statements. Look for unusual spikes, duplicate charges, or opportunities to consolidate suppliers for better pricing.

Real‑World Examples: Companies That Benefited from No‑Guarantee Corporate Cards

Seeing the concept in action helps solidify its value. Here are two brief case studies.

Tech Startup “ByteWave”

ByteWave, a SaaS company with $2 million in annual revenue, secured a corporate credit card without personal guarantee from Capital One. By funneling all software subscriptions and travel expenses through the card, they earned $12,000 in cash‑back annually, reduced manual expense processing time by 40%, and kept the founders’ personal credit untouched during a rapid growth phase.

Manufacturing Firm “ForgeCo”

ForgeCo, an established mid‑size manufacturer, negotiated a corporate guarantee card with Wells Fargo. The card’s 60‑day payment term allowed them to align vendor payments with their production cycle, improving cash flow by $150,000 per year. Moreover, the detailed spend reports helped the CFO tighten budgeting and cut unnecessary travel spend by 15%.

Frequently Asked Questions (FAQ)

Do I need to have a personal credit score to apply?

Most issuers will still ask for personal information for identity verification, but they will not use your personal credit score to determine eligibility if you qualify for a true corporate credit card without personal guarantee.

Can a startup with less than $500k revenue qualify?

It’s challenging but not impossible. Some niche fintechs and alternative lenders are beginning to offer no‑guarantee cards to high‑growth startups that can demonstrate strong cash flow or have a solid personal credit profile for the founders.

What happens if the company defaults?

The corporation bears the loss. Creditors may place liens on company assets or pursue legal action against the business entity, but owners’ personal assets remain protected unless a personal guarantee was signed.

Are there annual fees?

Yes, many corporate cards charge annual fees ranging from $95 to $550. However, the rewards and expense‑management tools often offset this cost, especially for businesses with high spend volumes.

How does this differ from a secured business credit card?

A secured card requires a cash deposit that serves as collateral, while a no‑guarantee corporate card relies on the company’s creditworthiness. Secured cards are usually easier to obtain but offer lower limits and fewer rewards.

Getting a corporate credit card without personal guarantee can be a pivotal move for businesses that want to protect personal assets while gaining the flexibility of revolving credit. By understanding eligibility, choosing the right issuer, and implementing disciplined expense controls, you can unlock cash‑flow benefits, earn valuable rewards, and keep your financials clean and transparent.

Ready to explore your options? Start by reviewing your business credit reports, gather the necessary financial statements, and reach out to an issuer that offers a corporate guarantee model. The right card could be the missing piece that powers your next phase of growth.