Getrawbox Getrawbox

Getrawbox Getrawbox

Related Articles

Running a high‑risk business isn’t just about navigating volatile markets or tight regulations; it’s also about handling money the right way. When you sell products or services that regulators label as “high risk,” you’ll quickly discover that getting paid by credit card can feel like climbing a steep hill with a heavy backpack.

Why? Because banks and payment processors see these merchants as more likely to face chargebacks, fraud, or even sudden regulatory crackdowns. That perception translates into higher fees, stricter underwriting, and sometimes outright refusals. But don’t worry—there are clear paths forward, and understanding the landscape is the first step toward smoother transactions.

In this article we’ll unpack the ins and outs of credit card processing for high risk enterprises. From choosing the right processor to managing chargebacks, we’ll give you practical tips that keep your cash flow steady while staying compliant. Let’s get into the details.

Credit Card Processing for High Risk: Core Challenges and Opportunities

High‑risk merchants fall into categories like travel agencies, adult entertainment, online gambling, CBD products, and subscription services with recurring billing. Each of these niches carries a unique set of risks that processors must evaluate. Below are the most common hurdles you’ll encounter:

- Higher Interchange Fees: Processors often add a risk surcharge on top of standard interchange rates, which can push your total cost per transaction above 3%.

- Rolling Reserves: Instead of receiving the full transaction amount immediately, a portion (usually 5‑10%) is held for a set period to cover potential chargebacks.

- Stricter Underwriting: Expect to provide extensive documentation, including bank statements, business plans, and proof of compliance with industry regulations.

- Limited Processor Choice: Not every payment gateway works with high‑risk verticals, so you’ll need a specialist that understands your niche.

- Chargeback Vulnerability: High‑risk merchants often see higher dispute rates, which can lead to fines or even account termination if not managed properly.

Despite these obstacles, there’s a silver lining: specialized high‑risk processors have built tools and expertise specifically designed to mitigate these issues. By partnering with the right provider, you can turn a perceived disadvantage into a competitive advantage.

Key Factors in Credit Card Processing for High Risk Merchants

When you’re evaluating potential partners, keep these criteria front and center:

- Industry Expertise: Does the processor have a track record with businesses like yours? Look for case studies or client testimonials that speak to your niche.

- Transparent Pricing: High‑risk fees can be a maze of monthly fees, per‑transaction surcharges, and reserve holds. Choose a processor that offers a clear breakdown.

- Chargeback Management Tools: Advanced fraud detection, real‑time alerts, and a dedicated chargeback team can dramatically reduce disputes.

- Compliance Support: Regulations such as PCI‑DSS, AML, and industry‑specific licensing requirements should be handled by your processor, not left to you alone.

- Integration Flexibility: Whether you run an e‑commerce store, a mobile app, or a brick‑and‑mortar outlet, the gateway must slot seamlessly into your existing tech stack.

Choosing the Right High‑Risk Processor

Not all payment processors are created equal, especially when it comes to high‑risk verticals. Below is a step‑by‑step approach to narrowing down your options:

1. Identify Your Business Profile

Start by listing the exact nature of your products, average transaction size, monthly volume, and typical chargeback rate. This data will help processors assess your risk level accurately.

2. Research Specialized Providers

Search for processors that explicitly advertise “high‑risk merchant accounts.” Companies like HighRiskPay, Durango Payments, and Soar Payments often have dedicated account managers who understand the quirks of each niche.

3. Compare Pricing Structures

Ask for a detailed quote that includes:

- Interchange‑plus markup

- Monthly gateway fee

- Chargeback fees

- Rolling reserve percentage and duration

Remember that the lowest headline rate isn’t always the best deal if hidden fees pile up.

4. Test Their Support

Reach out to the sales or support team with a few “what‑if” scenarios. Fast, knowledgeable replies signal that you’ll have solid assistance when disputes arise.

5. Verify Compliance and Security

Ensure the processor is PCI‑DSS Level 1 compliant and offers tokenization or end‑to‑end encryption. This reduces your liability and builds consumer confidence.

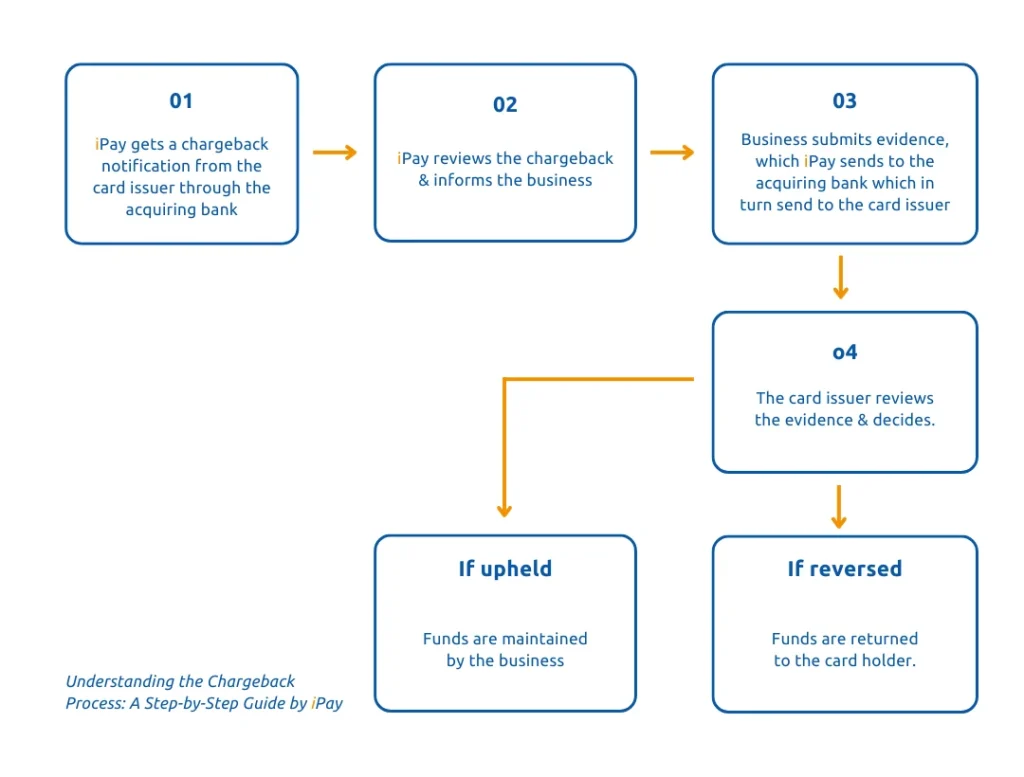

Managing Chargebacks Like a Pro

Chargebacks are the Achilles’ heel of high‑risk credit card processing. While you can’t eliminate them entirely, you can dramatically lower their frequency and impact.

Best Practices for Chargeback Prevention

- Clear Descriptions: Use recognizable business names and detailed product descriptors on customer statements.

- Transparent Refund Policies: Publish a straightforward return and cancellation policy; make it easy for customers to resolve issues before they file disputes.

- Robust Verification: Implement AVS (Address Verification Service), CVV checks, and 3‑D Secure where possible.

- Fraud Monitoring: Deploy real‑time fraud scoring tools that flag suspicious orders for manual review.

- Prompt Communication: Respond to chargeback notifications within the required timeframe (usually 7‑30 days) with solid evidence.

If a chargeback does slip through, a well‑documented rebuttal—complete with shipping confirmations, signed receipts, and communication logs—can sway the issuer in your favor. Some high‑risk processors even provide a “chargeback representment” service, handling the paperwork for you.

Balancing Fees and Cash Flow

High‑risk processing fees can eat into profit margins, but with strategic planning you can keep cash flow healthy.

Negotiating Rolling Reserves

While reserves protect processors, they also tie up capital. If you have a solid track record of low chargeback ratios, ask for a reduced reserve percentage or a shorter hold period. Demonstrating consistent sales volume and timely payouts can strengthen your negotiating position.

Leveraging Tiered Pricing

Some processors offer tiered rates based on transaction volume. As your business grows, you may qualify for a lower per‑transaction fee. Keep an eye on your monthly sales numbers and request a rate review when you cross a new threshold.

Bundling Services

Consider bundling your payment gateway with related services—like a business bank account with lowest fees—to negotiate a package discount. Many providers partner with banks to offer reduced merchant account fees for customers who open a compatible business checking account.

Regulatory and Compliance Considerations

High‑risk merchants operate under a microscope. Here’s what you need to stay compliant:

- PCI‑DSS: All merchants must meet the Payment Card Industry Data Security Standard, regardless of risk level.

- Industry‑Specific Licenses: For example, CBD sellers need a state‑approved hemp license; online gambling platforms require gambling authority permits.

- Anti‑Money Laundering (AML) Rules: Conduct Know‑Your‑Customer (KYC) checks for large or suspicious transactions.

- State & Federal Regulations: Keep abreast of evolving legislation, such as the 2024 “High‑Risk Merchant Act” that introduces new reporting requirements for certain verticals.

Partnering with a processor that offers compliance guidance can save you headaches and potential fines. Many providers assign a compliance officer to your account, ensuring you meet all necessary standards.

Future Trends: What’s Next for High‑Risk Processing?

The landscape is evolving fast. Here are a few trends that could reshape credit card processing for high‑risk businesses in the next few years:

1. Alternative Payments Gaining Traction

Cryptocurrency, ACH, and real‑time payment rails (like the U.S. FedNow service) are becoming viable options for high‑risk merchants who want to bypass traditional card networks.

2. AI‑Driven Fraud Prevention

Machine learning models can now analyze thousands of data points in milliseconds, flagging fraudulent activity with unprecedented accuracy. Expect more processors to bundle AI tools into their standard offering.

3. Greater Transparency Regulations

Regulators are pushing for clearer disclosure of fees and reserve policies. This shift will benefit merchants by making it easier to compare providers.

4. Consolidated Financial Solutions

Some fintech platforms are bundling merchant accounts, business banking, and corporate credit cards into a single dashboard. If you’re looking for a corporate credit card without personal guarantee, keep an eye out for integrated solutions that streamline cash management.

Practical Checklist for High‑Risk Credit Card Processing

Before you sign any agreement, walk through this quick checklist to ensure you’ve covered the essentials:

- Identify your industry risk level and gather supporting documentation.

- Compare at least three specialized high‑risk processors.

- Request a detailed fee breakdown, including any reserve requirements.

- Verify PCI‑DSS compliance and encryption methods.

- Assess chargeback mitigation tools and support response times.

- Confirm that the processor can integrate with your existing e‑commerce platform or POS system.

- Review the contract for termination clauses and notice periods.

- Plan a strategy for rolling reserves, ensuring you have enough working capital.

- Set up regular compliance reviews with your processor’s compliance officer.

- Stay updated on emerging payment trends that could diversify your revenue streams.

By ticking these boxes, you’ll be in a stronger position to negotiate favorable terms and protect your business from the typical pitfalls of high‑risk credit card processing.

Ultimately, high‑risk credit card processing for high risk merchants isn’t a death sentence for profitability. With the right partner, proactive fraud prevention, and a solid understanding of fees and compliance, you can keep your customers paying smoothly while safeguarding your bottom line. Remember, the key is to treat your payment ecosystem as a strategic asset—not just a cost center.