Getrawbox Getrawbox

Getrawbox Getrawbox

Related Articles

When you’re hunting for a credit card that offers a truly hassle‑free experience, the Citi Simplicity Card often tops the list. Its promise of no late fees, no annual fee, and an extended 0 % intro APR on purchases and balance transfers makes it especially attractive to both newcomers and seasoned cardholders. But before you dive in, you’ll want to know whether your credit profile meets the bar. In other words, what is the credit score required for Citi Simplicity Card and how can you position yourself for a smooth approval?

This article breaks down the score expectations, the other factors Citi looks at, and practical steps you can take to improve your odds. Whether you’re planning to apply this month or simply curious about the card’s standards, the information here will give you a clear roadmap. Let’s unpack the details so you can decide if the Citi Simplicity Card is within your reach.

Credit Score Required for Citi Simplicity Card: The Baseline You Should Target

While Citi doesn’t publicly publish a hard cutoff, industry data and anecdotal evidence point to a typical range of 720‑740 for the credit score required for Citi Simplicity Card. Applicants sitting comfortably in the “good” to “excellent” bracket (700‑749) usually see a higher acceptance rate, whereas those below 700 may encounter more scrutiny or outright denial.

Why this range? Citi’s underwriting algorithm balances risk and reward. A score of 720‑740 signals a reliable payment history, low credit utilization, and a mix of credit types—attributes that align with the card’s low‑risk, low‑fee structure. Keep in mind that the credit score is just one piece of the puzzle; income, debt‑to‑income ratio, and recent credit inquiries also play significant roles.

How the Credit Score Required for Citi Simplicity Card Interacts With Other Eligibility Factors

- Income Verification: Even with a strong score, Citi wants to see sufficient income to cover potential balances.

- Debt‑to‑Income (DTI) Ratio: A lower DTI (< 35 %) strengthens your application, showing you have room to manage additional credit.

- Recent Credit Activity: Multiple hard inquiries in a short period can signal risk, potentially offsetting a solid score.

- Credit History Length: Longer histories (5+ years) give Citi confidence in your repayment habits.

In short, meeting the credit score required for Citi Simplicity Card is necessary but not sufficient. A holistic view of your financial picture determines the final decision.

Understanding the Citi Simplicity Card’s Core Benefits

Before you chase the score, it helps to know why the card is worth the effort. The Citi Simplicity Card offers:

- 0 % introductory APR for 21 months on purchases and balance transfers.

- No annual fee—ideal for budget‑conscious consumers.

- No late fees, over‑limit fees, or penalty APRs, which truly lives up to the “simplicity” promise.

- Access to Citi’s ThankYou® Points program (though not as generous as premium cards, it still provides redemption flexibility).

If these perks align with your financial goals, working toward the required score becomes a strategic move rather than a mere hurdle.

Strategies to Reach the Credit Score Required for Citi Simplicity Card

Boosting your credit score isn’t an overnight miracle, but steady, disciplined actions can get you into the 720‑740 range within a few months. Below are proven tactics:

- Pay Down Balances: Aim for a utilization below 30 %, ideally under 10 %. This single change can add 20‑30 points.

- Automate Payments: On‑time payments are the single biggest driver of credit scores. Set up automatic transfers to avoid missed due dates.

- Keep Old Accounts Open: The length of credit history matters; closing old cards can shave points off.

- Limit Hard Inquiries: Space out applications for new credit. Each hard pull can temporarily dip your score by 5‑10 points.

- Dispute Inaccuracies: Review your credit report for errors. Correcting a mistaken late payment can result in a noticeable boost.

Combine these steps with a consistent check on your score (many banks offer free monthly updates) and you’ll be steadily moving toward the credit score required for Citi Simplicity Card.

What to Do If Your Score Falls Short

Not everyone hits the 720‑740 sweet spot on the first try. If your current score is below the typical range, consider these alternatives:

- Apply for a Secured Card First: Building a solid payment history on a secured card can lift your score over time.

- Become an Authorized User: Adding yourself to a family member’s well‑managed credit card can boost your score quickly.

- Target a Different Citi Card: Some Citi products have slightly lower score thresholds, such as the Citi® Double Cash Card, which still offers strong rewards.

While you work on improving your credit, you might also explore other beginner‑friendly options. For instance, the article Is Discover a Good First Credit Card? An In‑Depth Look offers a great comparison of entry‑level cards that can serve as stepping stones.

Application Process: How to Submit Your Request Smoothly

When you feel ready, the application itself is straightforward:

- Visit Citi’s official website and navigate to the Simplicity Card page.

- Fill out personal information, including Social Security Number, income, and housing costs.

- Review the terms, submit the form, and wait for an instant decision (often within minutes).

Having all your documents handy—pay stubs, tax returns, and a recent credit report—can speed up the process. If you’re pre‑approved, the likelihood of acceptance is even higher, much like the benefits you’ll read about in Chase Business Credit Card Pre Approval – How to Get It & Why It Matters.

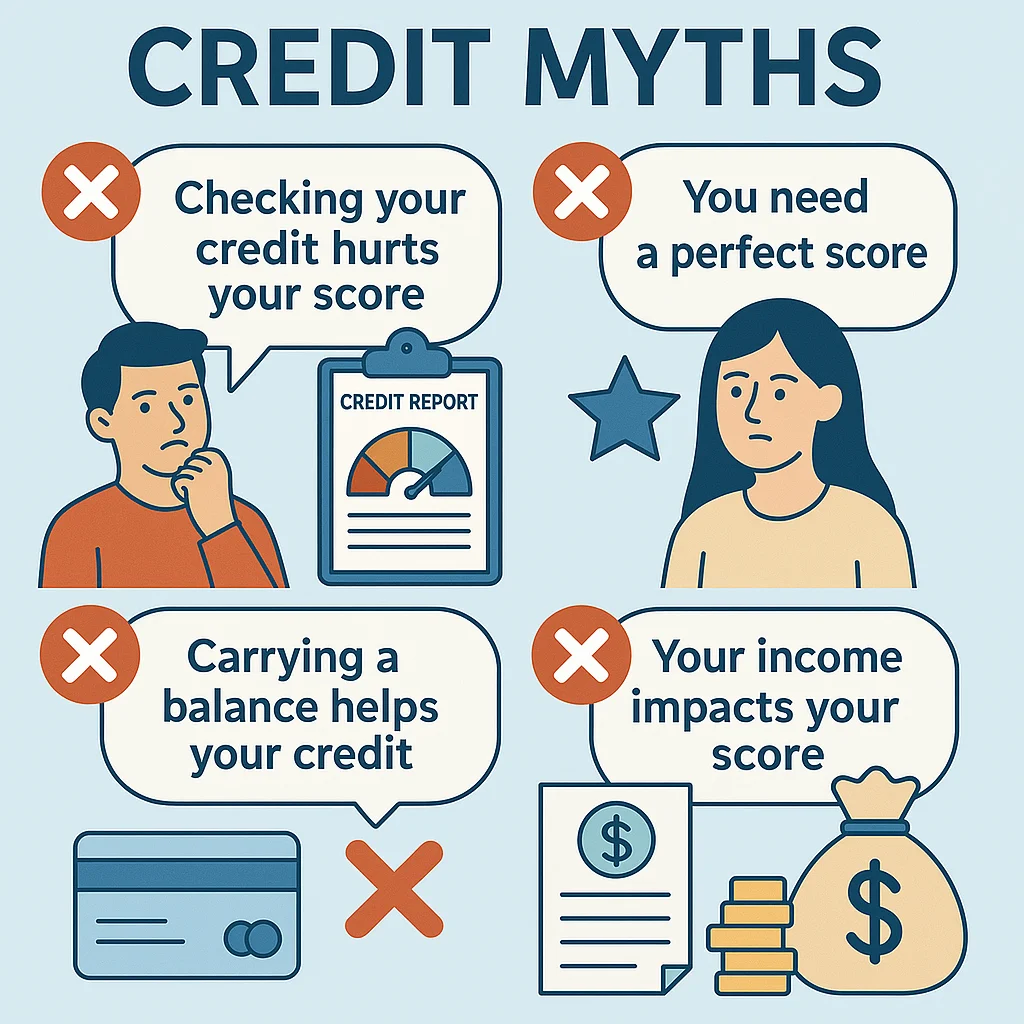

Common Myths About the Credit Score Required for Citi Simplicity Card

Myth #1: “You need a perfect 850 score.”

Reality: While a perfect score certainly helps, Citi’s range sits comfortably in the good‑to‑excellent band. Scores in the low 700s can still qualify if other factors are strong.

Myth #2: “Only high earners get approved.”

Reality: Income matters, but Citi also weighs debt‑to‑income ratio and existing credit limits. A modest income paired with low utilization can beat a high income with high debt.

Myth #3: “Once you’re denied, you can’t reapply.”

Reality: You can reapply after 30‑90 days, especially if you’ve taken steps to improve your credit profile in the interim.

Final Thoughts on Securing the Citi Simplicity Card

Understanding the credit score required for Citi Simplicity Card is the first step toward enjoying its fee‑free, penalty‑free benefits. Aim for the 720‑740 range, but remember that a solid income, low DTI, and clean payment history are equally vital. By following the practical strategies outlined above—paying down balances, automating payments, and keeping old accounts open—you’ll not only improve your chances of approval but also set a stronger foundation for overall financial health.

Whether you’re a seasoned cardholder looking for a low‑cost backup or a first‑time applicant seeking a forgiving credit environment, the Simplicity Card can be a perfect fit once you meet the score criteria. Keep monitoring your credit, stay disciplined with payments, and when the time feels right, submit that application. The simplicity promised by Citi isn’t just in the card’s terms; it’s also in the straightforward path you’ll follow to get it.

Good luck, and may your credit journey be as smooth as the card’s interest‑free period.