Table of Contents

- What Is General Liability Insurance for Construction Business?

- Why General Liability Insurance for Construction Business Is Non‑Negotiable

- Key Components of a Solid General Liability Policy

- How General Liability Insurance for Construction Business Interacts With Other Policies

- Factors That Influence Premiums for General Liability Insurance for Construction Business

- Tips to Lower Your General Liability Insurance Costs

- Choosing the Right Provider for General Liability Insurance for Construction Business

- Real‑World Example: When General Liability Insurance Saved a Contractor

- Common Misconceptions About General Liability Insurance for Construction Business

- Integrating General Liability with a Comprehensive Risk Management Plan

- Steps to Secure Your General Liability Insurance for Construction Business

- Related Resources You Might Find Useful

Running a construction business is no small feat. From juggling project timelines and budgets to managing crews on bustling job sites, there’s a lot on the plate. One critical piece that often gets overlooked—until it’s too late—is general liability insurance for construction business. This type of coverage acts like a safety net, protecting you from the financial fallout of accidents, property damage, and lawsuits that can arise in the field.

Imagine a subcontractor accidentally dropping a heavy beam, damaging a client’s brand-new storefront, or a passerby slipping on a wet concrete slab and filing a claim. Without the right protection, the costs can quickly spiral out of control, threatening the very survival of your company. In this article, we’ll walk through the fundamentals of general liability insurance for construction business, explore the key coverages you need, and share practical tips on selecting a policy that fits your unique risks.

What Is General Liability Insurance for Construction Business?

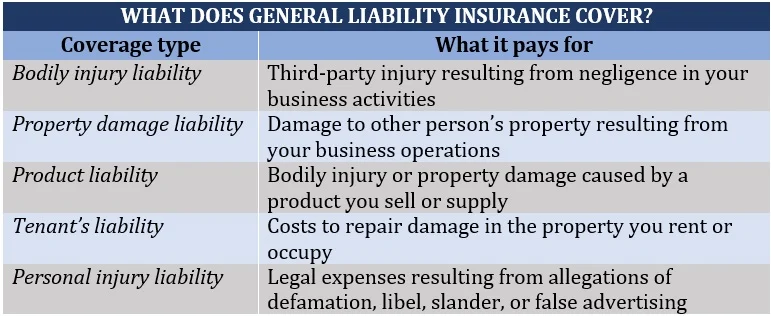

General liability insurance for construction business is a foundational policy that shields contractors from third‑party claims of bodily injury, property damage, and related legal expenses. Unlike workers’ compensation, which focuses on employee injuries, or professional liability, which covers errors in advice, general liability steps in when a third party—like a client, visitor, or neighbor—suffers loss because of your operations.

The policy typically includes:

- Bodily injury coverage: Pays for medical costs and legal fees if someone is hurt on your job site.

- Property damage coverage: Covers repair or replacement costs for damage you cause to someone else’s property.

- Personal and advertising injury: Handles claims such as libel, slander, or copyright infringement that arise from your marketing materials.

- Legal defense costs: Even if a lawsuit is unfounded, the insurance can cover attorney fees and court expenses.

Why General Liability Insurance for Construction Business Is Non‑Negotiable

Construction sites are high‑risk environments. Heavy machinery, hazardous materials, and a constant flow of workers and visitors create a perfect storm for accidents. A single incident can lead to a lawsuit that runs into hundreds of thousands of dollars—far beyond the reach of most small to midsize firms. Having general liability insurance for construction business isn’t just about compliance; it’s about safeguarding your financial future and maintaining a trustworthy reputation.

Key Components of a Solid General Liability Policy

Not all general liability policies are created equal. When you’re shopping for coverage, pay close attention to these components:

- Coverage limits: This is the maximum amount the insurer will pay per incident and in aggregate over the policy period. For many construction firms, a $1 million per occurrence limit with a $2 million aggregate is a common starting point.

- Deductibles: The amount you’ll pay out of pocket before the insurer steps in. Lower deductibles mean higher premiums, so balance affordability with risk tolerance.

- Exclusions: Every policy lists what’s not covered. Typical exclusions include damage to your own property, contractual liability, and pollution-related claims unless you purchase additional coverage.

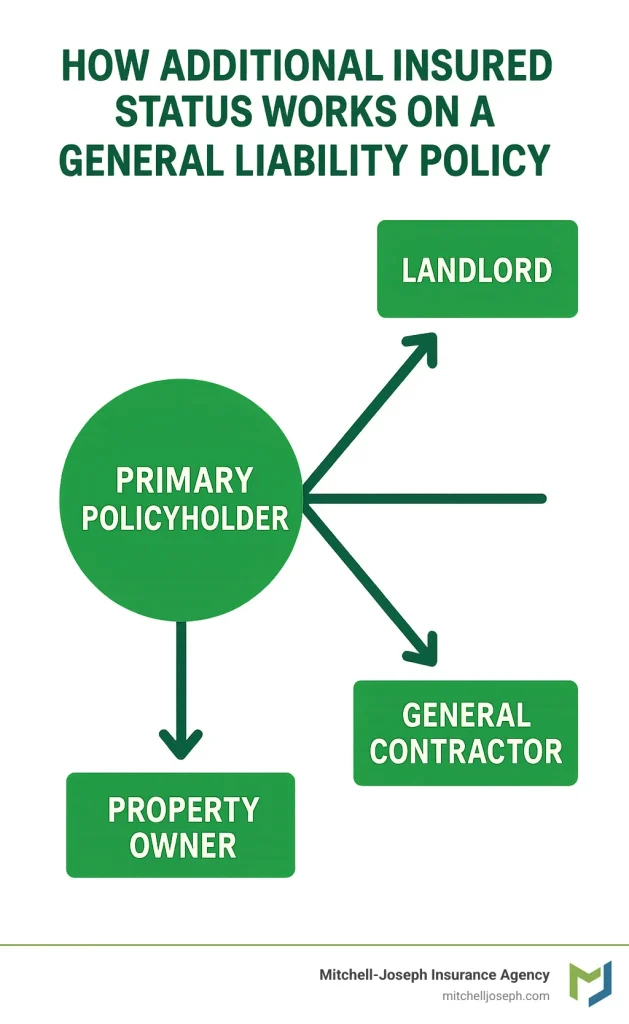

- Additional insureds: Clients often require you to add them to your policy as “additional insureds.” This can be a negotiation point; make sure you understand the implications.

- Broadened definition of “completed operations”: Covers incidents that occur after a project is finished, such as a structural defect that leads to injury.

How General Liability Insurance for Construction Business Interacts With Other Policies

While general liability is essential, it doesn’t operate in a vacuum. You’ll likely need a suite of policies to fully protect your business, including:

- Errors and Omissions Insurance for Consultants – What You Need to Know – especially if you provide design or consulting services.

- Workers’ compensation for employee injuries.

- Commercial auto insurance for your fleet of trucks and vans.

- Equipment insurance for high‑value tools and machinery.

Understanding how these policies overlap prevents gaps in coverage and can sometimes lower overall costs through bundled discounts.

Factors That Influence Premiums for General Liability Insurance for Construction Business

Insurance carriers assess risk based on a variety of factors. Knowing what drives your premium can help you take proactive steps to reduce costs:

- Business size and annual revenue: Larger firms with higher revenue usually face higher premiums.

- Type of work performed: Specialty trades like demolition or electrical work are seen as higher risk than general carpentry.

- Claims history: A clean record can earn you discounts, while frequent claims raise rates.

- Location: States with stricter construction regulations or higher litigation rates may see higher premiums.

- Safety programs: Documented safety training, OSHA compliance, and accident prevention initiatives can lower your risk profile.

Tips to Lower Your General Liability Insurance Costs

Here are some practical steps you can take to keep premiums manageable without sacrificing coverage:

- Implement a robust safety program and track incident reports.

- Maintain a clean claims history by promptly addressing minor incidents before they escalate.

- Bundle your general liability policy with other commercial coverages (like commercial auto or workers’ comp) to qualify for multi‑policy discounts.

- Consider higher deductibles if you have sufficient cash reserves to cover small losses.

- Shop around and request quotes from multiple carriers—pricing can vary widely.

Choosing the Right Provider for General Liability Insurance for Construction Business

Not every insurer understands the nuances of the construction industry. Look for carriers that specialize in commercial construction or have a dedicated team for contractors. When evaluating providers, ask the following:

- Do you have experience underwriting policies for businesses similar to mine?

- What endorsements or additional coverages are commonly recommended for my line of work?

- How quickly can you respond to a claim, and what is your claims handling reputation?

- Are there risk management resources or safety training programs offered as part of the policy?

Choosing a partner who not only offers coverage but also supports your risk mitigation efforts can be a game‑changer for long‑term success.

Real‑World Example: When General Liability Insurance Saved a Contractor

Consider a mid‑size remodeling firm that accidentally caused water damage to a client’s historic home during a bathroom renovation. The repair costs, including specialized restoration, ran up to $150,000. Because the contractor had a solid general liability insurance for construction business with a $1 million limit, the insurer covered the damages and legal fees, allowing the firm to keep its reputation intact and continue bidding on new projects.

Common Misconceptions About General Liability Insurance for Construction Business

Even seasoned contractors sometimes hold inaccurate beliefs about this essential coverage. Let’s debunk a few:

- “My workers’ comp covers everything.” Workers’ comp protects employees, not third parties. A client who slips on site is still a third‑party claim.

- “I don’t need it because I have a small crew.” Even a one‑person operation can cause property damage or bodily injury that leads to costly lawsuits.

- “My contract says the owner is liable.” Contractual clauses don’t eliminate legal responsibility; they merely shift financial responsibility, which insurance can cover.

Integrating General Liability with a Comprehensive Risk Management Plan

Insurance should be the final layer of a broader risk management strategy. Start with:

- Thorough site assessments and safety audits.

- Clear written contracts that outline responsibilities and indemnities.

- Regular training on equipment handling, fall protection, and emergency procedures.

- Documentation of all safety measures—this can be leveraged during underwriting to secure better rates.

When you combine proactive safety practices with robust general liability insurance for construction business, you build a resilient operation that can weather unexpected setbacks.

Steps to Secure Your General Liability Insurance for Construction Business

Ready to get covered? Follow these straightforward steps:

- Assess your risk profile. List the types of projects you handle, the size of your crew, and any past incidents.

- Gather quotes. Reach out to at least three reputable insurers that specialize in construction.

- Compare policy terms. Look beyond price—examine limits, exclusions, and endorsements.

- Check the carrier’s financial strength. Ratings from A.M. Best or Moody’s indicate the insurer’s ability to pay claims.

- Finalize and purchase. Work with an agent to customize the policy, add any required additional insureds, and sign the agreement.

After purchasing, keep your policy documents accessible, review them annually, and adjust coverage as your business grows or diversifies into new trade areas.

Related Resources You Might Find Useful

While you’re reviewing insurance options, you may also want to explore other protective measures for your business, such as Professional Liability Insurance for Small Businesses – What You Need to Know. This coverage complements general liability by addressing claims that arise from professional advice or design errors, which can be especially relevant if you also provide consulting services.

Additionally, if you’re a small firm looking to bundle employee benefits, checking out Health Insurance Quotes for Small Business – A Complete Guide can help you attract and retain skilled workers while potentially lowering overall insurance costs through combined underwriting.

In summary, general liability insurance for construction business is a non‑negotiable pillar of any contractor’s risk management arsenal. By understanding the coverage, assessing your unique risks, and partnering with a knowledgeable insurer, you can protect your bottom line, preserve client trust, and focus on what you do best—building great structures.