Table of Contents

- Understanding Florida Small Business Health Insurance Plans

- Key Features of Florida Small Business Health Insurance Plans

- Types of Coverage Available to Small Businesses in Florida

- Health Maintenance Organizations (HMOs)

- Preferred Provider Organizations (PPOs)

- High‑Deductible Health Plans (HDHPs) + Health Savings Accounts (HSAs)

- Catastrophic Plans

- How to Choose the Right Florida Small Business Health Insurance Plan

- Assess Your Workforce Demographics

- Evaluate Total Cost of Ownership

- Check Provider Networks

- Consider Employee Feedback

- Cost Factors Specific to Florida

- Utilize the Small Business Health Insurance Tax Credit

- Regulatory Landscape and Compliance

- ACA Reporting Requirements

- Florida’s Specific Mandates

- Open Enrollment Windows

- Tips for Managing Your Florida Small Business Health Insurance Plans

- Leverage Online Enrollment Platforms

- Offer Wellness Programs

- Stay Informed About Market Changes

- Review and Re‑Negotiate Annually

- Resources and Next Steps

Running a small business in the Sunshine State comes with its own set of challenges and perks. One of the biggest responsibilities you’ll face is making sure your team stays healthy—and that often means finding the right health insurance. In Florida, the market is a blend of national carriers, regional insurers, and a few state‑specific options that can feel overwhelming at first glance.

But don’t worry. This guide walks you through the essentials of florida small business health insurance plans, breaking down the jargon, highlighting cost‑saving strategies, and giving you practical steps to secure coverage that keeps both your employees and your bottom line happy.

Whether you’re a solo entrepreneur hiring your first employee or you already have a crew of ten, the principles covered here will help you navigate the maze of options, stay compliant with federal and state regulations, and ultimately choose a plan that fits your unique business needs.

Understanding Florida Small Business Health Insurance Plans

At its core, a florida small business health insurance plan is a group health policy that a company purchases to cover its employees. Unlike individual policies, group plans typically offer better rates, broader networks, and more predictable costs because the risk is spread across all participants.

Florida’s market is heavily influenced by the Affordable Care Act (ACA), which requires employers with 50 or more full‑time equivalents to offer “affordable” coverage or face penalties. While most small businesses fall below this threshold, many still opt into ACA‑compliant group plans to stay competitive and attract top talent.

Key Features of Florida Small Business Health Insurance Plans

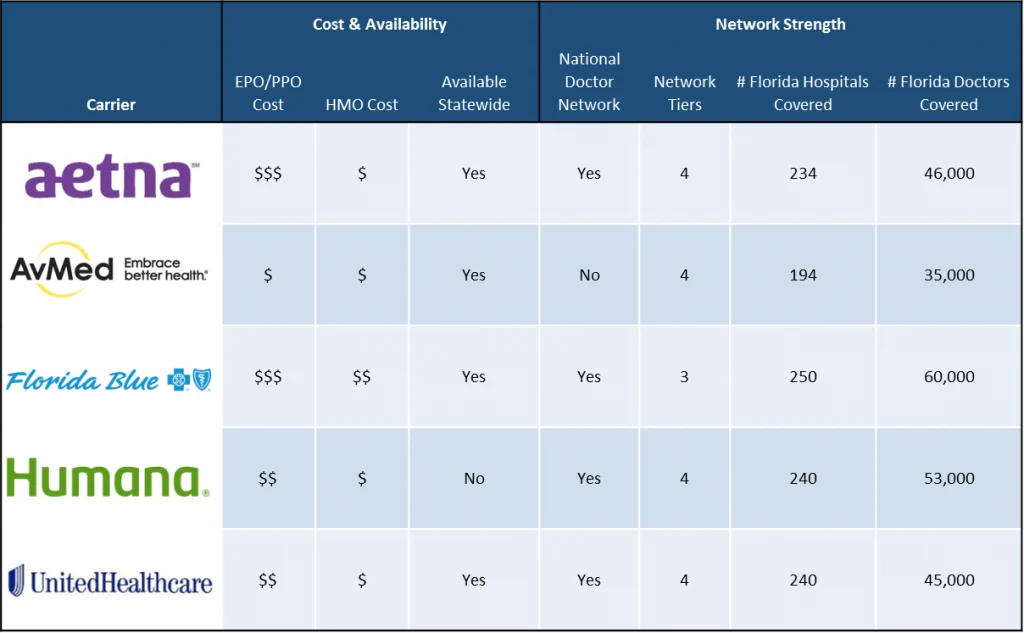

- Network Size: Larger insurers often provide extensive provider networks across the state, while regional carriers may focus on specific metro areas like Miami or Tampa.

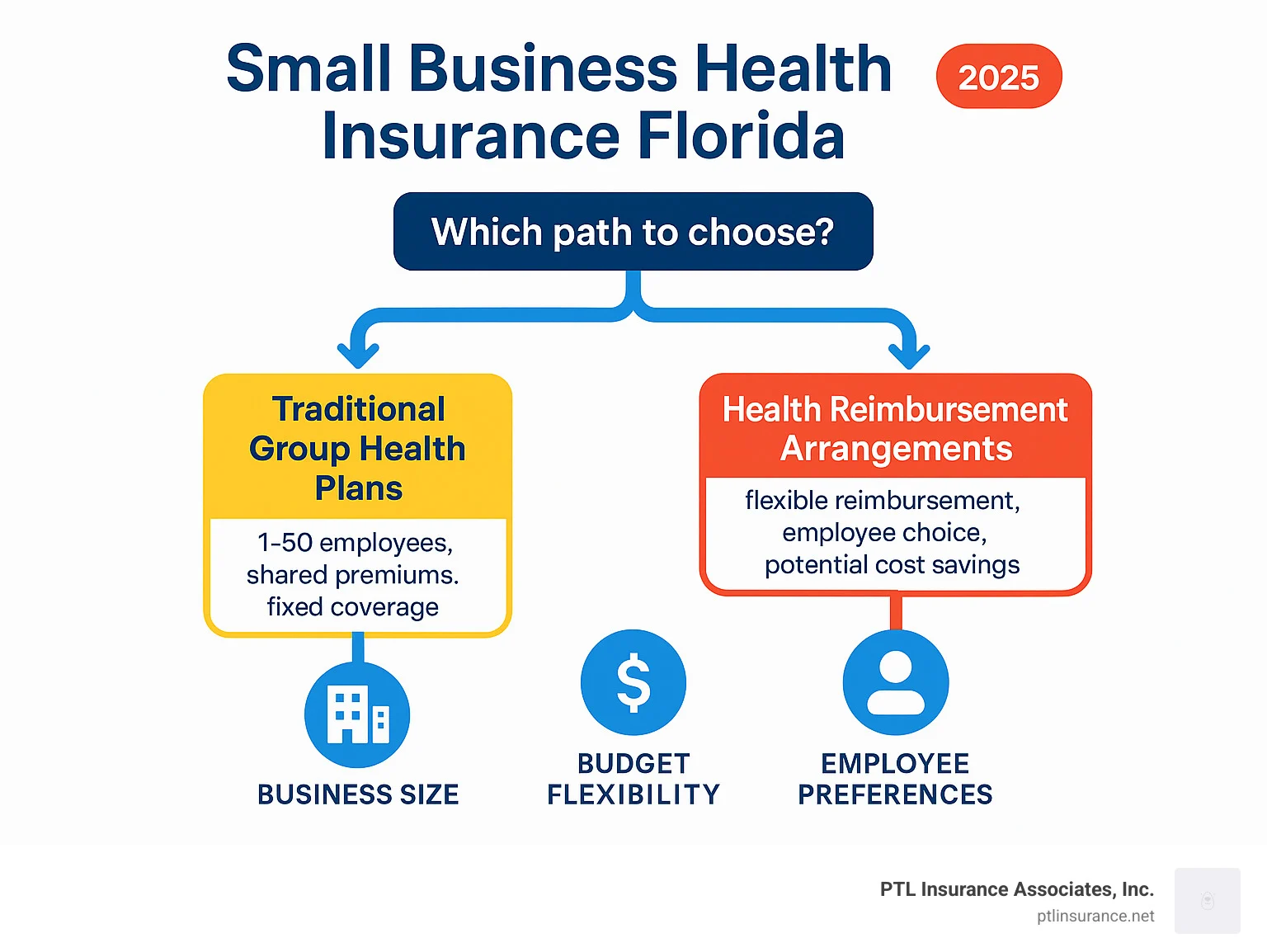

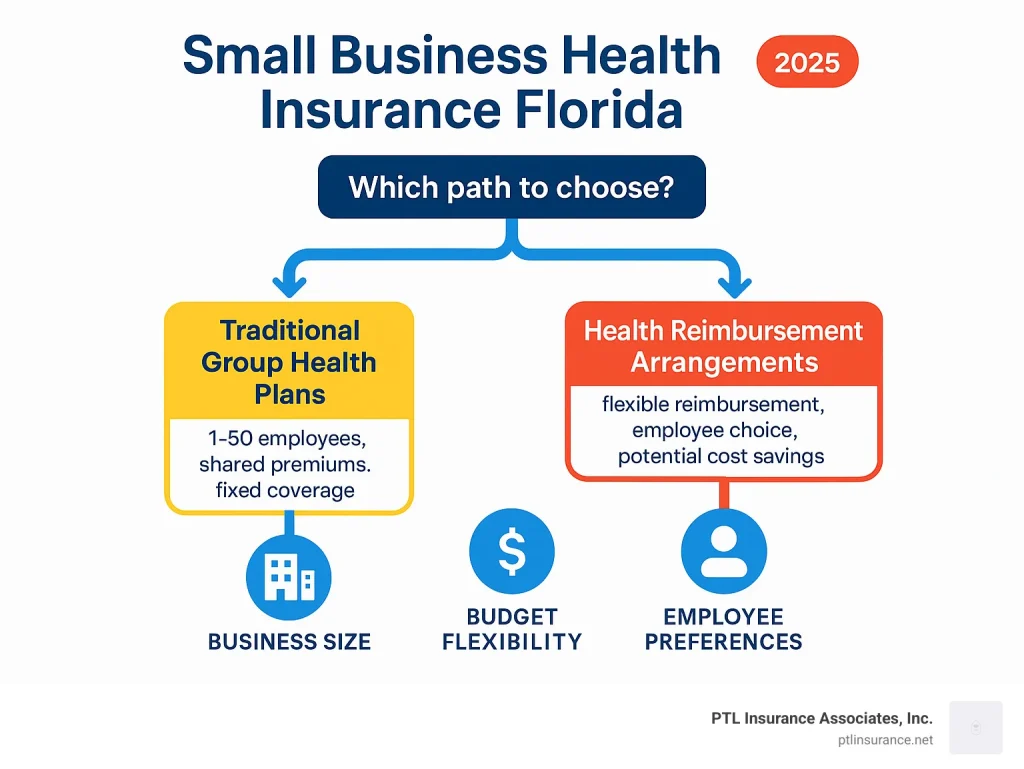

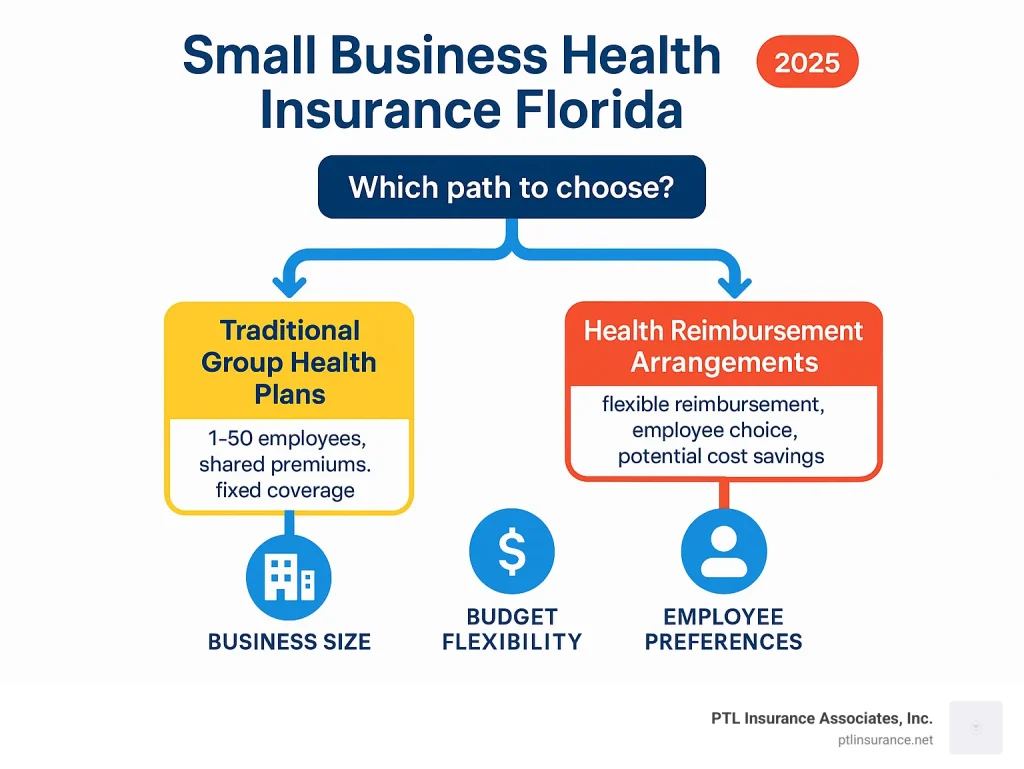

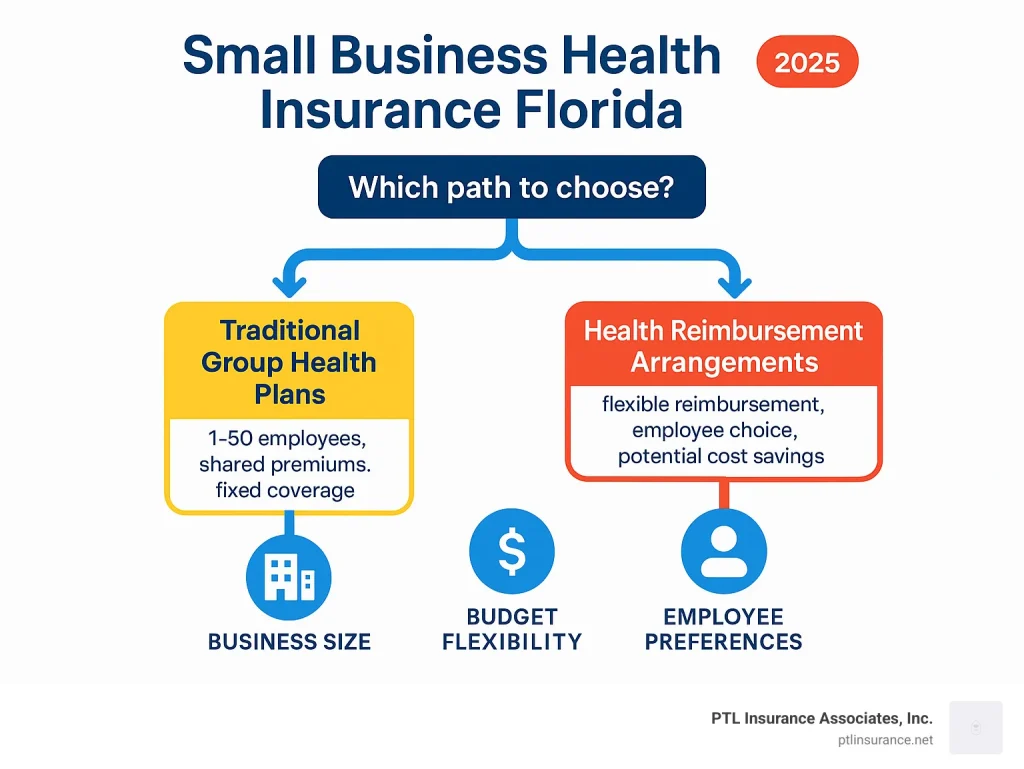

- Plan Types: From Health Maintenance Organizations (HMOs) to Preferred Provider Organizations (PPOs) and High‑Deductible Health Plans (HDHPs) paired with Health Savings Accounts (HSAs), options abound.

- Employer Contributions: Businesses can choose to cover a portion or the entirety of premiums, affecting both tax deductions and employee satisfaction.

- Compliance Tools: Many carriers offer online portals to track ACA reporting, eligibility, and enrollment periods.

Types of Coverage Available to Small Businesses in Florida

Not all health plans are created equal, and the best fit depends on your workforce size, budget, and the level of flexibility you want to provide. Below are the most common categories you’ll encounter when researching florida small business health insurance plans.

Health Maintenance Organizations (HMOs)

HMOs usually require employees to select a primary care physician (PCP) and get referrals for specialists. The trade‑off is lower premiums and out‑of‑pocket costs, making HMOs a solid choice for businesses looking to keep expenses predictable.

Preferred Provider Organizations (PPOs)

PPOs give employees the freedom to see any doctor, inside or outside the network, though staying in‑network saves money. This flexibility is attractive to a diverse workforce, especially those with existing relationships with certain specialists.

High‑Deductible Health Plans (HDHPs) + Health Savings Accounts (HSAs)

HDHPs pair a higher deductible with lower monthly premiums. When combined with an HSA, employees can save pre‑tax dollars for qualified medical expenses, which rolls over year to year. This model works well for younger, healthier teams who prefer lower upfront costs.

Catastrophic Plans

Designed primarily for individuals under 30 or those with a hardship exemption, catastrophic plans cover essential services after a high deductible is met. While not typically offered as a primary group option, some Florida employers include them as a supplemental tier.

How to Choose the Right Florida Small Business Health Insurance Plan

Selecting a plan isn’t just about comparing premiums. You’ll want to weigh multiple factors to ensure the coverage aligns with both your financial goals and employee expectations.

Assess Your Workforce Demographics

Look at age distribution, family status, and common health concerns. For example, a workforce with many young, single employees might appreciate an HDHP with an HSA, while a team of families may favor an HMO with lower co‑pays.

Evaluate Total Cost of Ownership

Beyond monthly premiums, consider:

- Employer contribution percentages

- Deductibles, co‑pays, and out‑of‑pocket maximums

- Administrative fees for enrollment platforms

- Potential tax credits such as the Small Business Health Care Tax Credit (available for businesses with ≤25 employees and average wages < $56,000)

Check Provider Networks

Florida’s geography means access can vary dramatically. Ensure the plan’s network covers providers in your employee’s hometowns—especially if you have staff spread across the state from the Panhandle to the Keys.

Consider Employee Feedback

Run a quick survey or hold a focus group. Employees often know what they value most—whether it’s lower premiums, broader specialist access, or telehealth options. Involving them early can boost enrollment rates and overall satisfaction.

Cost Factors Specific to Florida

Florida’s insurance market has some unique cost drivers:

- Climate‑Related Risks: Higher rates of certain illnesses (e.g., asthma from humidity) can affect underwriting.

- Population Diversity: A mix of retirees, seasonal workers, and young families creates varied health utilization patterns.

- State Regulations: Florida imposes its own consumer protections and mandates specific benefits, influencing plan pricing.

To offset these variables, many small businesses join “small group” pools through the Florida Office of Insurance Regulation, which can negotiate better rates by aggregating risk across multiple employers.

Utilize the Small Business Health Insurance Tax Credit

If you qualify, the federal tax credit can cover up to 50% of your premium contributions, dramatically reducing the cost of a florida small business health insurance plan. Keep detailed records of employee wages and contributions to claim this credit on your tax return.

Regulatory Landscape and Compliance

Staying compliant isn’t optional—non‑compliance can lead to hefty fines and reputational damage. Here’s what you need to keep in mind:

ACA Reporting Requirements

Even if you’re under the 50‑employee threshold, you must provide a summary of the health coverage offered to each employee (Form 1095‑C) if you’re offering an ACA‑compliant plan.

Florida’s Specific Mandates

The state requires certain essential health benefits (EHBs) to be included, such as emergency services, maternity care, and mental health treatment. Ensure your chosen plan lists these EHBs explicitly.

Open Enrollment Windows

Most group plans follow an annual open enrollment period, typically from November to January. However, “qualifying life events” (e.g., marriage, birth of a child) allow employees to enroll outside this window.

Tips for Managing Your Florida Small Business Health Insurance Plans

Having the right plan is just the beginning. Effective administration can save you time, money, and headaches.

Leverage Online Enrollment Platforms

Many carriers provide digital portals where employees can select coverage, view plan documents, and manage dependents. These tools streamline the process and reduce paperwork.

Offer Wellness Programs

Incentivize healthy habits through wellness challenges, gym membership discounts, or on‑site health screenings. Healthier employees generally generate lower claims, which can lead to lower premiums over time.

Stay Informed About Market Changes

The health insurance landscape evolves rapidly. Subscribe to newsletters from the Florida Office of Insurance Regulation and consider partnering with a broker who can alert you to new plan options or regulatory updates.

Review and Re‑Negotiate Annually

Don’t assume your first plan is the best forever. At the end of each plan year, evaluate claim data, employee satisfaction, and cost trends. Use this information to negotiate better terms or explore alternative carriers.

Resources and Next Steps

Ready to dive deeper? Start by gathering a list of potential carriers and requesting quotes. Our Medical Insurance Quotes for Small Businesses – A Complete Guide offers a step‑by‑step approach to obtaining and comparing quotes efficiently.

If you’re also looking to bundle other types of coverage—like property or liability—check out the Fort Collins Home and Auto Insurance Bundle: Save More, Stress Less article for ideas on how bundling can create additional savings.

Finally, remember that the health of your business is tightly linked to the health of your team. Investing time and resources into a well‑structured florida small business health insurance plan not only meets legal obligations but also builds a culture of care that can boost retention, morale, and productivity.

Take the first step today: assess your workforce, set a budget, and reach out to a trusted broker or carrier. With the right plan in place, you’ll have one less worry on your plate and more energy to focus on growing your business.