Table of Contents

- What Is the Vanguard Target Retirement 2055 Fund VFFVX?

- Key Features of Vanguard Target Retirement 2055 Fund VFFVX

- Asset Allocation and Glide‑Path Details

- Performance Overview

- Fees and Expenses

- How VFFVX Fits Into a Broader Retirement Strategy

- Tips for Maximizing the Vanguard Target Retirement 2055 Fund VFFVX

- Potential Drawbacks to Keep in Mind

- Comparing VFFVX to Other Target‑Date Options

- How to Invest in Vanguard Target Retirement 2055 Fund VFFVX

Planning for retirement can feel like navigating a maze, especially when you’re juggling multiple accounts, market volatility, and the ever‑changing rules around withdrawals. One popular shortcut many investors take is to lean on a target‑date fund that automatically rebalances as you get closer to the retirement horizon. If you’re aiming to retire around 2055, Vanguard’s offering—vanguard target retirement 2055 fund vffvx—might just be the set‑and‑forget vehicle you’ve been looking for.

But before you click “buy,” it’s worth digging a little deeper. Understanding the underlying strategy, the fee structure, and how the fund aligns with your broader financial picture can make the difference between a smooth glide into retirement and a bumpy ride. In this article we’ll break down the key components of the vanguard target retirement 2055 fund vffvx, compare it with similar products, and give you some practical tips on how to incorporate it into a diversified retirement plan.

What Is the Vanguard Target Retirement 2055 Fund VFFVX?

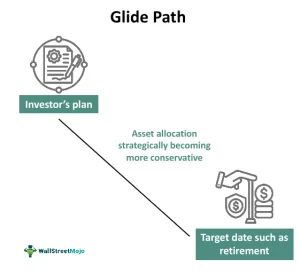

The vanguard target retirement 2055 fund vffvx is a target‑date mutual fund designed for investors who expect to retire roughly in the year 2055. Vanguard’s target‑date series follows a “glide‑path” that gradually shifts the asset allocation from a growth‑focused mix of stocks to a more conservative blend of bonds and cash as the target date approaches. The fund’s ticker symbol, VFFVX, is the shorthand you’ll see on brokerage platforms.

Key Features of Vanguard Target Retirement 2055 Fund VFFVX

- All‑in‑One Portfolio: Holds a mix of Vanguard index funds covering U.S. equities, international equities, and fixed income.

- Automatic Rebalancing: Adjusts the allocation each quarter to follow the glide‑path.

- Low Expense Ratio: Vanguard is known for low costs; VFFVX’s expense ratio is competitive within the industry.

- Tax‑Efficient Structure: The fund is structured as a mutual fund, which can be held in taxable accounts, IRAs, or 401(k)s.

Asset Allocation and Glide‑Path Details

When you first invest in the vanguard target retirement 2055 fund vffvx, the portfolio is heavily weighted toward equities—about 90% of the assets are stocks, split between U.S. large‑cap, U.S. small‑cap, and international equities. The remaining 10% sits in bonds and short‑term investments. This aggressive stance makes sense for someone with a 30‑plus‑year horizon, giving the portfolio ample time to ride out market swings.

As the years tick down, the glide‑path gradually reduces equity exposure. By 2045, the stock allocation typically drops to around 70%, and by the target year 2055, it’s roughly 50% stocks to 50% bonds. This shift aims to protect the accumulated nest egg from a market downturn right when you need the money most.

Performance Overview

Historical performance is never a guarantee of future results, but it does give a snapshot of how the fund has handled past market cycles. Over the past 10 years, the vanguard target retirement 2055 fund vffvx has delivered an average annual return in the mid‑high single digits, closely tracking the combined performance of its underlying index funds.

During bull markets, the fund tends to outperform more conservative portfolios because of its equity tilt. Conversely, in bear markets, the built‑in diversification and gradual shift toward bonds helps cushion losses, though investors will still see some volatility.

Fees and Expenses

One of Vanguard’s biggest selling points is its low-cost structure. The vanguard target retirement 2055 fund vffvx carries an expense ratio of just 0.12%, which is significantly lower than many actively managed target‑date funds that can charge 0.70% or more. Lower fees mean more of your money stays invested and compounds over time.

In addition to the expense ratio, investors should be aware of any potential transaction fees charged by their brokerage. However, many online brokers now offer commission‑free trades on Vanguard funds, making VFFVX an even more attractive option for cost‑conscious investors.

How VFFVX Fits Into a Broader Retirement Strategy

While the vanguard target retirement 2055 fund vffvx offers a convenient one‑stop solution, it’s rarely advisable to rely on a single fund for your entire retirement plan. Consider pairing VFFVX with other vehicles to address specific goals:

- Home Equity Line of Credit for Retirees – A Smart Way to Unlock Home Value: If you own a home, a HELOC can provide a flexible source of cash for large expenses without tapping your investment accounts. Read more here.

- Retirement Plan Options for Small Businesses – A Complete Guide: If you’re self‑employed or run a small business, you might supplement VFFVX with a SEP‑IRA or Solo 401(k). Details are available here.

- Vanguard Target Retirement 2035 Fund VTTHX – In‑Depth Review & Guide: For a diversified approach, you could hold a later‑date fund like VFFVX alongside an earlier‑date fund such as VTTHX to balance risk across different horizons. Learn more here.

Tips for Maximizing the Vanguard Target Retirement 2055 Fund VFFVX

- Start Early: The longer your money stays invested, the more you benefit from compounding and the equity bias of the early glide‑path.

- Stay Consistent: Set up automatic contributions to keep dollar‑cost averaging into the fund.

- Review Annually: Even though VFFVX rebalances automatically, an annual check ensures the fund still aligns with your overall financial situation.

- Consider Tax Implications: Holding the fund in a tax‑advantaged account (IRA or 401(k)) can defer taxes on dividends and capital gains.

Potential Drawbacks to Keep in Mind

Despite its many strengths, the vanguard target retirement 2055 fund vffvx isn’t a perfect fit for everyone. Here are a few considerations:

- Limited Customization: The fund’s allocation is preset; you can’t tweak the exact stock‑bond mix to reflect personal preferences.

- One‑Size‑Fits‑All Glide‑Path: Some investors may prefer a more aggressive or conservative glide‑path than Vanguard’s default.

- Market Risk Remains: Even with diversification, the fund is exposed to market downturns, especially in the early years when equity exposure is high.

Comparing VFFVX to Other Target‑Date Options

If you’re shopping around, you’ll notice other providers like Fidelity, T. Rowe Price, and American Funds also offer 2055 target‑date funds. Compared to the vanguard target retirement 2055 fund vffvx, many of these competitors charge higher expense ratios and may have slightly different glide‑paths. For example, the T. Rowe Price 2020 retirement fund has a more aggressive equity tilt and a higher fee structure.

When weighing options, consider three key metrics: expense ratio, historical risk‑adjusted returns (Sharpe ratio), and the exact asset allocation at each stage. Vanguard consistently scores well on the expense front, which can translate into higher net returns over a 30‑year horizon.

How to Invest in Vanguard Target Retirement 2055 Fund VFFVX

Getting started with VFFVX is straightforward:

- Open a brokerage account that offers Vanguard funds (most major brokers do).

- Search for the ticker symbol VFFVX.

- Decide on an initial lump‑sum investment or set up recurring contributions.

- Choose the account type—taxable, traditional IRA, Roth IRA, or employer‑sponsored plan.

- Monitor the account annually to ensure the fund still matches your retirement timeline and overall asset allocation strategy.

If you’re uncertain about the best account type for your situation, a financial advisor can help you evaluate the tax implications and align the fund with your broader retirement plan.

Overall, the vanguard target retirement 2055 fund vffvx offers a low‑cost, hands‑off approach that can serve as the backbone of a retirement portfolio for anyone targeting a mid‑2030s to early‑2050s retirement horizon. By understanding its glide‑path, fee structure, and how it interacts with other financial tools—like a home equity line of credit or a small‑business retirement plan—you can make a more informed decision and set yourself up for a smoother transition into retirement.

Remember, no single fund can replace a comprehensive financial plan. Pair VFFVX with solid budgeting, emergency savings, and perhaps a side of real‑estate exposure if it aligns with your risk tolerance. With disciplined investing and periodic reviews, you’ll be well on your way to reaching that 2055 retirement goal.