Getrawbox Getrawbox

Getrawbox Getrawbox

Related Articles

Starting a new business is an exhilarating mix of vision, hustle, and endless to‑do lists. Amid product development, marketing plans, and hiring, one foundational task often gets pushed to the back burner: setting up a business bank account for new business. It may sound simple, but the right account can be a silent engine that fuels credibility, streamlines cash flow, and keeps you compliant with tax regulations.

Think of your business bank account as the financial front door of your venture. It separates personal and professional money, safeguards your personal assets, and presents a professional image to vendors, clients, and lenders. Moreover, many banks bundle tools—like invoicing, payroll integration, and expense tracking—that can save you hours of manual work.

In this guide we’ll walk through everything a founder needs to know: why a dedicated account matters, what features to hunt for, how to compare providers, and practical steps to get yours up and running without a hitch.

Business Bank Account for New Business: Why It’s a Must‑Have

When you open a business bank account for new business, you’re doing more than just getting a place to deposit cash. You’re establishing a clear financial boundary that protects you and builds trust.

- Legal protection: Keeping personal and business funds separate helps maintain the corporate veil, especially for LLCs and corporations, reducing personal liability.

- Professional credibility: Paying suppliers with a business check or ACH transfer looks far more trustworthy than using a personal account.

- Accurate bookkeeping: A dedicated account simplifies expense tracking, tax preparation, and financial reporting.

- Access to financing: Lenders often require several months of business banking statements before approving a loan. A solid account history can be the key to unlocking capital.

If you’re still on the fence, take a look at the free business bank account guide. It explains how a well‑structured account can set the tone for your financial discipline from day one.

Choosing a Business Bank Account for New Business: Core Features to Evaluate

Not all banks are created equal, and the features that matter most will vary depending on your industry, cash flow patterns, and growth plans. Below are the key criteria you should weigh when evaluating options.

- Fees and minimum balances: Some banks charge monthly maintenance fees unless you meet a minimum balance or transaction threshold. Others offer fee‑free accounts for the first year—great for cash‑strapped startups.

- Online and mobile banking experience: A robust digital platform lets you deposit checks, transfer funds, and reconcile accounts on the go. Check out the online banking for small business owners article for a deep dive into top platforms.

- Integration capabilities: Does the bank sync with accounting software like QuickBooks, Xero, or Wave? Seamless integration cuts down on manual entry and errors.

- Payment processing tools: Look for built-in merchant services, ACH capabilities, and the ability to issue virtual or physical debit cards to employees.

- Customer support: Small business owners often need quick answers. A dedicated small‑business support line or relationship manager can be a lifesaver.

- Branch access vs. digital‑only: If you handle a lot of cash or need in‑person assistance, a bank with physical branches may be essential. Conversely, digital‑only banks often provide faster onboarding.

Business Bank Account for New Business: Step‑by‑Step Setup Checklist

Getting your account live is usually quicker than you think—especially if you prepare the paperwork in advance. Follow this checklist to avoid surprises.

- Choose the right legal structure: Your business type (sole proprietorship, LLC, corporation) determines which documents you’ll need.

- Gather required documents: Typically you’ll need:

- Employer Identification Number (EIN) from the IRS

- Articles of Incorporation or Organization

- Operating Agreement or Bylaws

- Personal identification (driver’s license or passport)

- Compare banks: Use the criteria above to shortlist 3‑5 institutions. Request a fee schedule and ask about any hidden costs.

- Open the account: Many banks let you start the process online. You’ll usually submit the documents digitally and verify your identity via video call or a mailed code.

- Set up online banking: Link your accounting software, order debit cards, and enable two‑factor authentication for security.

- Transfer initial capital: Deposit your seed money, record the transaction, and ensure your bookkeeping system reflects the new balance.

- Update payment information: Switch any recurring vendor payments, payroll services, and invoicing tools to the new account number.

Need a free option? The opening an online business bank account: your complete guide walks through zero‑fee accounts that still offer essential features.

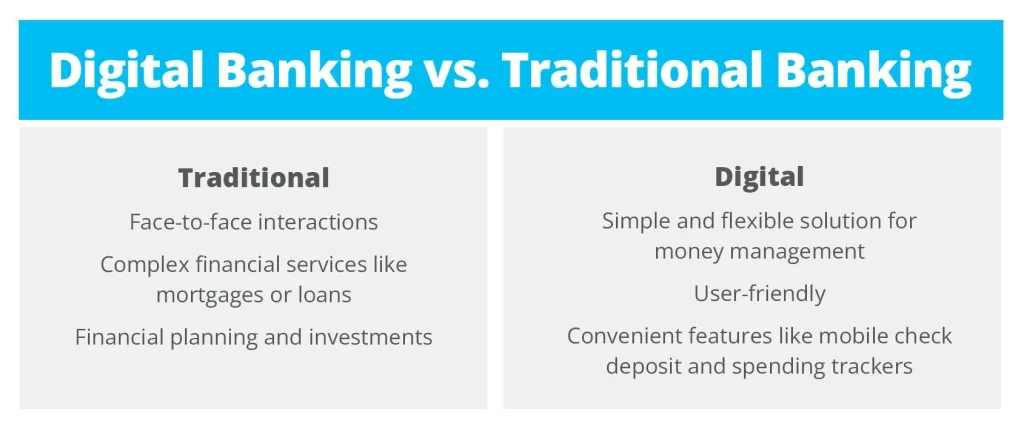

Banking Options: Traditional vs. Digital‑Only for Your New Business

When you search for a business bank account for new business, you’ll encounter two main camps: brick‑and‑mortar banks (like Chase, Wells Fargo, Bank of America) and digital‑only banks (such as Mercury, Novo, or BlueVine). Each has pros and cons.

Traditional Banks

Traditional banks often boast a large network of branches, which can be handy if you handle cash deposits or need in‑person assistance. They also tend to have more robust lending products—useful when you transition from startup to growth phase. However, they may impose higher fees and longer onboarding times.

Digital‑Only Banks

Digital banks focus on speed and simplicity. You can usually open an account within minutes, often with no minimum balance. They excel at integrating with modern accounting tools and offering real‑time transaction alerts. The trade‑off is limited cash‑handling services and, occasionally, less access to traditional loans.

Whichever route you choose, the most important thing is that the account aligns with your business workflow. If you anticipate heavy cash transactions, a traditional bank may be safer. If you’re a SaaS startup that lives online, a digital‑only solution could save you time and money.

Common Pitfalls and How to Avoid Them

Even seasoned entrepreneurs stumble over a few avoidable mistakes when setting up their business bank account for new business. Recognizing these pitfalls early can keep your finances on track.

Mixing Personal and Business Funds

It’s tempting to use a personal account for early-stage expenses, but doing so erodes the legal protection an LLC or corporation offers. Keep every receipt, invoice, and transfer within the business account to maintain a clean audit trail.

Ignoring Transaction Limits

Some free accounts impose a cap on the number of free transactions per month. If your startup processes dozens of invoices daily, those limits can quickly turn into hidden fees. Review the transaction policy before you commit.

Overlooking International Capabilities

If you plan to sell abroad or receive payments in foreign currencies, ensure your bank supports multi‑currency accounts or low‑cost foreign exchange. Otherwise you might end up paying hefty conversion fees.

Neglecting Security Features

Business accounts are prime targets for fraud. Choose a bank that offers multi‑factor authentication, real‑time alerts, and the ability to set user permissions for employees.

Leveraging Your Business Account for Growth

Once your business bank account for new business is live, it becomes a platform for strategic financial moves.

- Cash‑flow forecasting: Use the bank’s reporting tools to project inflows and outflows, helping you anticipate shortfalls before they happen.

- Accessing credit lines: A healthy banking relationship can unlock revolving lines of credit, which are crucial for inventory purchases or bridging seasonal gaps.

- Automating payments: Set up recurring ACH transfers for payroll and vendor bills. Automation reduces manual errors and saves time.

- Building a credit profile: Consistently maintaining a positive balance and paying any bank fees on time contributes to your business credit score, making future financing easier.

When you’re ready to explore financing options, remember that lenders often request three months of business bank statements. Our business loans 3 month bank statements guide explains how to present those statements in the best light.

Maximizing Benefits of a High‑Yield Savings Component

Some banks bundle a high‑yield savings account with their business checking package. While interest rates may not rival dedicated investment accounts, the extra earnings on idle cash can add up. The Lending Club Bank high yield savings article provides a quick overview of how such accounts work and whether they’re worth the effort for startups.

Final Thoughts

Choosing the right business bank account for new business is one of the first strategic decisions you’ll make as an entrepreneur. By separating finances, leveraging digital tools, and staying vigilant about fees and security, you set a solid foundation for growth. Remember to prepare your paperwork, compare both traditional and digital providers, and align the account’s features with your operational needs.

Take the time now to research, ask questions, and even test a few platforms with trial accounts if possible. The effort you invest today will pay dividends in smoother cash flow, easier tax filing, and stronger credibility with partners and investors. Happy banking, and here’s to the success of your new venture!